direct primary care

What is direct primary care?

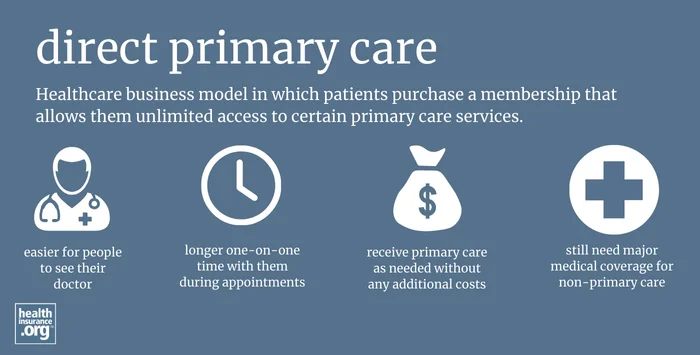

Direct primary care (DPC) is a healthcare business model in which a physician practice offers an arrangement in which patients purchase a membership that allows them unlimited access to certain primary care services. The patient pays a monthly fee to the medical office, and can then access care as needed, without paying an additional fee at the time of service.

How does direct primary care work?

Direct primary care practices enroll patients in a membership program, and provide certain primary care services without the patient having to pay anything other than the monthly membership fee. Members may be able to access additional services – such as prescription drugs, imaging, and lab services – by paying a fee at the time of service (but often at wholesale pricing). Direct primary care practices generally do not bill third-party payers (commercial health insurance, Medicaid, Medicare, etc.), which means that the patient is fully responsible for the cost of any care that isn't included in the membership fee.

How common is direct primary care?

According to one resource, as of early 2026, there were more than 2,800 direct primary care practices, including locations in every state in the U.S.1 On average, direct primary care practices have about 413 patients.2 So the vast majority of individuals in the U.S. are not utilizing DPC memberships. But the number of direct primary care practices has been steadily growing,3 and the idea has become more popular with patients over the last decade.

How much does a direct primary care membership cost?

The fees for direct primary care will vary from one office to another. Pricing generally varies by age, with the lowest rates for children ($20 to $75 per month is common) and the highest rates for older adults, who will sometimes pay up to $150 per month for a direct primary care membership. But in most cases, the monthly fee is in the range of $50 to $100 per member.2

Discounted rates may be available for couples or families, or for paying on a quarterly or annual basis instead of monthly. And the rate for children might also vary depending on whether an adult is also enrolling along with the child. Direct primary care practices often require a one-time enrollment fee in addition to the membership fee.

What services are covered with a direct primary care membership?

The specific services that you can receive via a direct primary care membership will depend on the direct primary care office you choose, and the scope of the practice. Many direct primary care memberships include in-person and virtual office visits (and sometimes home/mobile visits), text/phone consultations with the medical provider, wellness visits, nutritional/weight management counseling, sutures, biopsy/excisions, cryotherapy, chronic disease management, sports physicals, etc.4

Some direct primary care practices have on-staff professionals who can provide services such as mental health care, acupuncture, chiropractic care, etc. And it's common for direct primary care practices to offer some basic laboratory, imaging, and/or immunization/pharmacy services, albeit with a cost that the patient has to pay in addition to their membership fee. But the DPC clinic may offer wholesale pricing for these services, resulting in lower out-of-pocket for the patient.5

However, direct primary care practices generally do not offer a full suite of outpatient services, as their focus is on primary care. So services such as colonoscopies, obstetrical care, outpatient surgery, vasectomies, imaging (MRI, CT, ultrasound, x-ray, etc.), and specialty medicine do not tend to be covered with a DPC membership.6 And DPC memberships do not cover care provided to members in other locations, such as the hospital, an outpatient surgery center, or an urgent care clinic.

Is a direct primary care membership a type of health insurance?

No. Direct primary care is not considered minimum essential coverage under the Affordable Care Act and more than half the states have enacted laws that explicitly exempt DPC from state insurance laws and insurance commissioner oversight.7

Do I still need health insurance if I have a direct primary care membership?

Yes. Relying on a DPC membership by itself is not recommended. Direct primary care memberships give patients access to a variety of primary care. But people still need health insurance in case they end up needing medical care that goes beyond the basic primary care services available through a DPC membership.

Combining a direct primary care membership with an ACA-compliant health plan (purchased on-exchange or off-exchange) might be an option for some people. The DPC membership will allow unlimited access to a primary care provider who can take care of the patient's basic needs. And the health insurance plan will be there in case more significant or specialty care is needed. (Mending, formerly Taro Health, which offers Marketplace/exchange health plans in Oklahoma and Maine, includes a DPC membership with all of its plans,8 and notes that many local DPC practices partner with Mending despite not accepting any other insurance.9

When you're shopping for a DPC paired with major medical health insurance, consider these tips for choosing a health plan. But the DPC membership may give you a bit of extra leeway, as you won't need to worry about using the health insurance plan for your routine primary care.

You'll still want to make sure that the health plan has in-network specialists and hospitals that are conveniently located. And you can check with the DPC practice to see if there is a particular hospital/provider system that they recommend and use for referrals. If so, it may make life easier if you pick a health insurance plan that has that provider system in its network.

But keep in mind that the fees you spend on your DPC membership won't count toward your health plan's out-of-pocket costs. So meeting your deductible and out-of-pocket limit will only happen if and when you need care that's outside the scope of the DPC practice.

It's also important to note that while you may see recommendations to combine a DPC membership with a health care sharing ministry plan, you still won't have any actual health insurance with that approach. Health care sharing ministry plans are also not considered health insurance, are not subject to insurance laws and regulations, and do not guarantee coverage for serious health conditions like a major medical plan. So if you're considering a DPC membership, it's still essential to have health insurance as well.

What are the pros and cons of direct primary care?

The direct primary care model generally makes it easier for people to see their doctor and have longer one-on-one time with them during appointments. On average, DPC members can get an appointment within one day2 and visits with the medical provider last an average of 30 to 60 minutes.10 DPC members appreciate being able to receive primary care as needed without any additional costs, and being able to get more one-on-one attention from their medical provider. And providers who have adopted the DPC model report improved job satisfaction, better relationships with patients, and improved quality of the medical care they can provide.2

But there are potential drawbacks to the DPC model. Direct primary care practices aren't available in all areas, and tend to be clustered in higher-income areas, which exacerbates physician shortages and economic/racial disparities in health care access. DPC enrollees must carefully read the fine print, understand what is and isn't included in their membership, and maintain health insurance coverage for other medical care they may end up needing.11 DPCs could also drive the trend toward less-robust employer-sponsored health coverage, with employers opting for higher deductible health plans combined with DPC memberships. And since DPCs are often exempt from insurance regulations and oversight, consumers generally cannot get help from the state department of insurance if they run into difficulties with their DPC membership.12

How does a DPC membership affect an HSA?

As of 2026, a DPC membership no longer makes a person ineligible to contribute to a health savings account (HSA), as long as certain conditions are met.13 Before 2026, longstanding rules prohibited HSA contributions if the person had a DPC membership in addition to their HSA-qualified high-deductible health plan (HDHP). But H.R. 1 – the “One Big Beautiful Bill Act” – which was enacted in July 2025, allows a person with an HDHP to contribute to an HSA even if they have a DPC membership, as long as the DPC meets the following requirements:14

- The monthly DPC fee cannot exceed $150/month for a single person, or $300/month for a family.

- The DPC membership can’t include prescription drugs (with the exception of vaccines), lab services “not typically administered in an ambulatory primary care setting” or “procedures that require the use of general anesthesia”

In addition, DPC membership fees are considered medical expenses starting in 2026, which means that the members can pay the membership fee with pre-tax HSA funds.15

(Note that the legislation was HSA-specific, and doesn't extend to flexible spending accounts (FSAs). Without additional IRS guidance, DPC membership fees are not necessarily an expense that can be reimbursed with an FSA.16 People with FSAs need to check with their FSA administrator to determine whether DPC membership fees are eligible for reimbursement in 2026.)

Can employers offer direct primary care memberships to their employees?

Yes. Employers can purchase direct primary care memberships for their employees, and this concept is growing in popularity.17 The employer can simultaneously switch to a health plan with a higher deductible and fewer services that are covered pre-deductible. The general idea is that the employer's total costs (for the health plan premium and DPC memberships) will decline, while employees will be more satisfied with their overall benefits package, thanks to the convenience that the DPC membership offers.

Is direct primary care the same thing as concierge medicine?

No. Direct primary care practices generally do not bill health insurance or other third-party payers, and instead rely on members' fees for their revenue. Concierge medical practices collect monthly fees from their members but also bill the members' health plans or collect additional fees at the time of service. And the monthly or annual fees to be part of a concierge medical practice tend to be much higher than direct primary care fees.18

Footnotes

- “DPC Frontier Mapper” Accessed Jan. 5, 2026 ⤶

- “Direct Primary Care” AAFP. Accessed Jan. 5, 2026 ⤶ ⤶ ⤶ ⤶

- “Q+A: Is the Growth of Direct Primary Care Expanding Health Care Access Where It’s Needed Most?” Drexel University. Nov. 26, 2024 ⤶

- ”2024 Direct Primary Care” American Academy of Family Physicians. May 7, 2024 ⤶

- ”Benefits of Direct Primary Care from a Patient’s Perspective” Ark Family Health. Accessed July 29, 2025 ⤶

- ”What’s The Difference Between Direct Primary Care And Traditional Healthcare?” Assurance Healthcare & Counseling Center. Dec. 16, 2021 ⤶

- “Direct Primary Care Arrangement, 50-State Survey” McDermott Will & Emery. Accessed Jan. 5, 2026 ⤶

- “What is direct primary care, or DPC?” Mending. Accessed Jan. 5, 2026 ⤶

- “New Name, New Look, Same Mission: Taro Health is now Mending” Mending/PR Newswire. June 27, 2025 ⤶

- “Direct Primary Care (DPC): A Consumer’s Guide to This Payment Model” GoodRx. Nov. 24, 2025 ⤶

- “The pros and cons of direct primary care (DPC)” Wolters Kluwer. Apr. 15, 2020 ⤶

- “5 Legal Considerations for Direct Care Providers” Hint Health. Apr. 2025 ⤶

- "Notice 2026-5, Expanded Availability of Health Savings Accounts under the One, Big, Beautiful Bill Act (OBBBA)" Internal Revenue Service. Accessed Mar. 17, 2026 ⤶

- “H.R.1 - One Big Beautiful Bill Act” (Section 71308(a)) Congress.gov. Enacted July 4, 2025 ⤶

- “H.R.1 - One Big Beautiful Bill Act” (Section 71308(b)) Congress.gov. Enacted July 4, 2025 ⤶

- "One Big Beautiful Bill Act (OBBBA) Refresher for 2026 Benefits Enrollment" Risk Strategies. Oct. 3, 2025 ⤶

- “Employer Trends in Direct Primary Care 2023” Hint Health. Accessed July 16, 2025 ⤶

- “The difference between direct primary care and concierge medicine” PeopleKeep. Nov. 7, 2024 ⤶