Find New Jersey Health Insurance Marketplace Coverage for 2026

Compare ACA plans and check subsidy savings from a licensed third-party health insurance agency.

New Jersey Health Insurance Marketplace Guide

This New Jersey health insurance guide, including the FAQs below, is designed to help you understand the coverage options and potential financial assistance that may be available to you and your family.

Starting in the fall of 2020, New Jersey began using its own state-based health insurance exchange (Marketplace) – Get Covered New Jersey. Before that, the state used the federally-facilitated HealthCare.gov Marketplace platform. Get Covered New Jersey is a platform where New Jersey residents can shop for individual and family health plans offered by various private health insurance carriers. These plans are used by people who aren’t eligible for Medicare, Medicaid, or an affordable employer-sponsored health plan.

For 2026 coverage, New Jersey’s Marketplace offers plans from five insurers (plan availability varies by area),1 down from six in 2025.2 (See details below about insurer participation and premium changes for 2026.)

In addition to federal premium subsidies and cost-sharing reductions, New Jersey also offers state-funded premium subsidies. The program, called New Jersey Health Plan Savings, is available to Get Covered New Jersey enrollees with household incomes up to 600% of the poverty level.3 This program continues to be available in 2026 with the same benefits and eligibility rules that were used in prior years.

But state officials clarified that they didn’t have enough funding to make up for the federal subsidy reductions due to the expiration of federal subsidy enhancements at the end of 2025.4 So while state subsidies continue to make coverage more affordable in 2026, it is less affordable overall than it was in 2025.5 (See below for details about enrollment totals and plan affordability for 2026.)

New Jersey is one of the few states that has its own individual mandate, which means residents who don’t have health insurance can be subject to a penalty on the state tax return.6

New Jersey ACA Marketplace quick facts

Frequently asked questions about health insurance in New Jersey

Who can buy Marketplace health insurance in New Jersey?

To be eligible to enroll in private health coverage through Get Covered New Jersey, you must:9

- Live in New Jersey and be lawfully present in the United States

- Not be incarcerated

- Not be enrolled in Medicare

So most New Jersey residents are eligible to enroll in a health plan through the exchange. But a bigger question for most people is eligibility for financial assistance, and there are some additional parameters must be met in order to qualify for state and federal subsidies through GetCoveredNJ.

To qualify for income-based Advance Premium Tax Credits (APTC), federal cost-sharing reductions (CSR), or New Jersey’s Health Plan Savings subsidies,10 you must:

- Not be eligible to enroll in an affordable plan offered by an employer. If you have access to an employer’s plan and aren’t sure whether it’s considered affordable, you can use our Employer Health Plan Affordability Calculator to see if you might qualify for premium subsidies via GetCoveredNJ.

- Not be eligible for New Jersey Family Care (Medicaid or CHIP), or premium-free Medicare Part A.11

- If married, file a joint tax return12 (with very limited exceptions)13

- Not be able to be claimed by someone else as a tax dependent.12

In addition to those basic parameters, qualifying for subsidies through Get Covered New Jersey depends on your household’s income and how that compares with the cost of the second-lowest-cost Silver plan in your area – which depends on your age and location.

When can I enroll in an ACA-compliant plan in New Jersey?

In New Jersey, the open enrollment period for 2026 coverage ended on January 31, 2026.14 This was a couple of weeks longer than the enrollment window used in most other states.

The open enrollment period will be shorter, however, starting in the fall of 2026. At that point, due to a federal rule finalized in 2025, state-run Marketplaces will be required to end open enrollment by December 31.

Outside of the annual open enrollment period, you may be eligible to enroll or make a plan change if you experience a qualifying life event, such as giving birth or losing other health coverage.

New Jersey is one of several states where pregnancy is considered a qualifying life event, allowing a pregnant woman to enroll in health coverage during the pregnancy (in most states, the birth of a baby is a qualifying event, but pregnancy is not).15

New Jersey enacted legislation to create an “easy enrollment” program that became available in early 2024, helping uninsured people get connected with health coverage via their state tax returns. 16

Native Americans can enroll year-round, without a specific qualifying life event.

Enrollment in New Jersey Family Care (Medicaid and CHIP) is available year-round.

How do I enroll in a Marketplace plan in New Jersey?

To enroll in an ACA Marketplace/exchange plan in New Jersey, you can:

- Visit Get Covered New Jersey, New Jersey’s health insurance exchange, to compare available health plans, determine whether you’re eligible for financial assistance (including federal and state subsidies), and enroll in coverage, either during open enrollment or during a special enrollment period.

- Enroll in a Get Covered New Jersey plan the help of licensed agents, navigators, or certified application counselors.17

You can reach GetCoveredNJ’s call center at 1-833-677-1010 TTY 711

How can I find affordable health insurance in New Jersey?

As a result of the Affordable Care Act (ACA), federal income-based subsidies (APTC) are available to lower the amount you pay for your health coverage each month. These subsidies are available to enrollees who meet the eligibility requirements and select a metal-level health plan through GetCoveredNJ.

In addition to the federal APTC, New Jersey is among the states that also offer state-funded subsidies. These subsidies (New Jersey Health Plan Savings) are available to households earning up to 600% of the federal poverty level (as opposed to the reinstated cap of 400% of FPL for federal premium subsidies).18 For 2026, that’s $93,900 for a single individual, and $192,900 for a family of four.)19

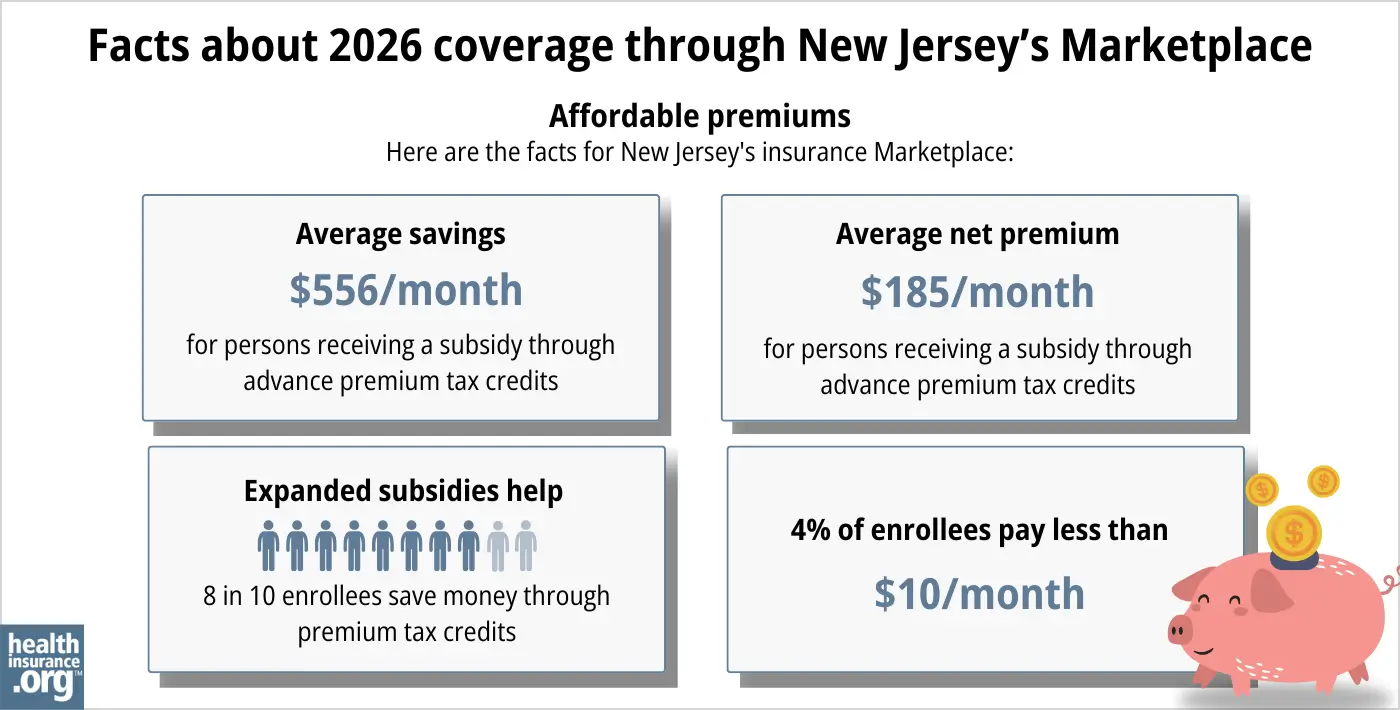

During the open enrollment period for 2026 coverage, about 80% of Get Covered New Jersey enrollees qualified for federal and/or state subsidies that averaged $556 per person per month.20

The year before, 90% of Get Covered New Jersey enrollees qualified for subsidies21 (see chart below), but federal subsidies are no longer available above 400% of FPL, and NJ state subsidies aren’t available above 600% of FPL.

Source: CMS.gov20

Applicants with household income up to 250% of the federal poverty level are also eligible for federal cost-sharing reductions (CSR), which reduce the deductible and other out-of-pocket expenses for Silver-level plans. Fifty-six percent of the people who enrolled via Get Covered New Jersey for 2025 were receiving CSR benefits.21

If you’re eligible for premium subsidies (including APTC and NJ Health Plan Savings subsidies) as well as CSR, you can use them both if you select a Silver-level plan through GetCoveredNJ. (APTC and NJ Health Plan Savings subsidies can be used with plans at any metal level, but CSR benefits are only available on Silver plans.)

For 2026 coverage, Get Covered New Jersey noted that Silver plan selections dropped while Bronze plan selections increased. This was due to the higher net premiums caused by the expiration of the federal subsidy enhancements, as people opted for plans with lower premiums.5

But even with the plan changes, net premiums rose. In 2025, nearly half of Get Covered New Jersey enrollees were paying no more than $10/month for their coverage, and that dropped to only 11% of enrollees in 2026.5

Although most Get Covered New Jersey enrollees do qualify for premium subsidies, New Jersey is also among the states that have created reinsurance programs. This helps to keep unsubsidized premiums lower than they would otherwise be.22 As of 2026, enrollees earning more than 600% of FPL in NJ are entirely unsubsidized, and anyone earning more than 400% of FPL is not eligible for federal premium subsidies.

Depending on your income and circumstances, you may be able to enroll in free or low-cost health coverage through New Jersey Family Care. Learn more about whether you might be eligible for Medicaid in New Jersey.

How many insurers offer Marketplace coverage in New Jersey?

Five insurers offer plans through New Jersey’s exchange for 2026:1

- AmeriHealth Ins. Co. of NJ

- Horizon Healthcare Services (BCBS)

- Oscar Health

- WellCare/Ambetter

- UnitedHealthcare

This is down from six in 2025.2 Aetna Health exited the market in New Jersey at the end of 2025, as was the case in all states where Aetna offered individual market coverage. New Jersey Marketplace enrollees with Aetna Health coverage had to select a new plan for 2026.

Are Marketplace health insurance premiums increasing in New Jersey?

For 2026, the following average rate changes were approved for New Jersey’s Marketplace insurers, amounting to an overall average rate increase of 16.6%,23 before subsidies are applied. But most enrollees get subsidies, and as described below, the increase in after-subsidy premiums was much larger due to the expiration of federal subsidy enhancements.

New Jersey’s ACA Marketplace Plan 2026 APPROVED Rate Increases by Insurance Company |

|

|---|---|

| Issuer | Percent Increase |

| AmeriHealth Ins. Co. of NJ | 15.5% |

| Horizon Healthcare Services (BCBS) | 18.1% |

| Oscar Health | 4.6% |

| WellCare/Ambetter | 17.1% |

| UnitedHealthcare | 18.4% |

Source: New Jersey Department of Banking and Insurance23

Average rate changes apply to full-price premiums. But most enrollees qualify for advance premium tax credits (subsidies) and thus do not pay full price. However, Marketplace coverage is much less affordable in 2026, due to the expiration of federal subsidy enhancements at the end of 2025.

Here are some examples of the sort of net premium increases that people experienced for 2026 in Cherry Hill, New Jersey:24

- 40-year-old earning $40,000:

- Lowest-cost plan in 2025 was $0/month

- Lowest-cost plan in 2026 is $93/month

- 60-year-old earning $63,000:

- Lowest-cost plan in 2025 was $191/month

- Lowest-cost plan in 2026 is $908/month (due to the subsidy cliff, no federal subsidy is available; this premium includes only NJ’s state subsidy)

For perspective, here’s an overview of how average unsubsidized premiums in the individual market in New Jersey have changed over the years:

- 2015: Average increase of 2%25

- 2016: Average increase of 10.2%26

- 2017: Average increase of 8.8%27

- 2018: Average increase of 22%28

- 2019: Average decrease of 9.3%29 (Reinsurance program took effect)

- 2020: Average increase of 8.7%30

- 2021: Average increase of 3.3%31

- 2022: Average increase of 7.9%32

- 2023: Average increase of 8.8%33

- 2024: Average increase of 4.4%34

- 2025: Average increase of 6.2%,2

How many people are insured through New Jersey’s Marketplace?

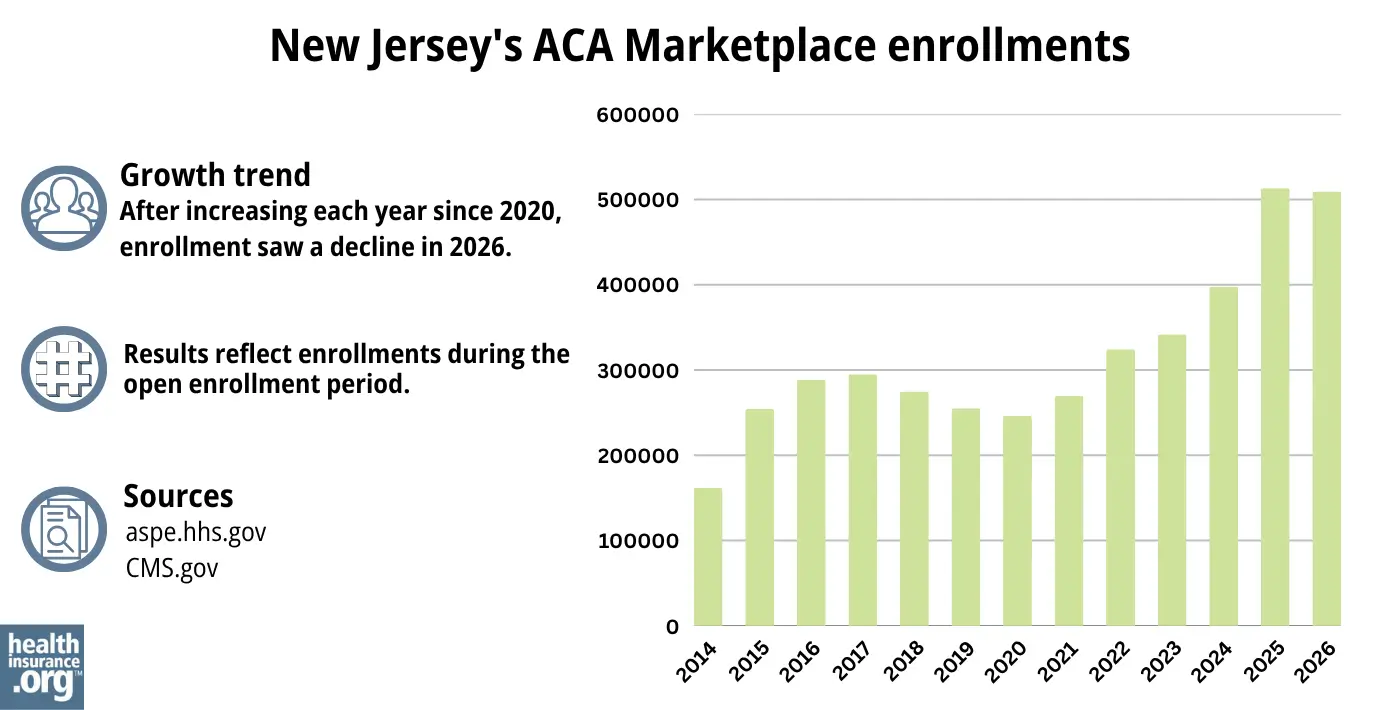

509,192 people enrolled in coverage through Get Covered NJ during the open enrollment period for 2026 coverage.20

That was down less than 1% from the year before, when 513,217 people selected plans during the open enrollment period for 2025 coverage.35 The 2025 enrollment was a new record high for the state, for the third year in a row.

Source: 2014,36 2015,37 2016,38 2017,39 2018,40 2019,41 2020,42 2021,43 2022,44 2023,45 2024,46 202535 202620

The enrollment growth in recent years was due partly to the enhancement of premium subsidies under the American Rescue Plan and Inflation Reduction Act, New Jersey’s additional state subsidy program, and the “unwinding” of the pandemic-era Medicaid continuous coverage rule. Medicaid disenrollments resumed in 2023 after a three-year pause. During the unwinding period, more than 48,000 New Jersey residents transitioned from Medicaid to a Marketplace plan.47

But the ARP/IRA subsidy enhancements expired at the end of 2025, resulting in higher net premiums for 2026. As a result, fewer people enrolled in coverage during the open enrollment period that ended on January 31, 2026.

What health insurance resources are available to New Jersey residents?

Get Covered New Jersey

New Jersey’s Marketplace/exchange. Residents who need to buy their own health insurance can use GetCoveredNJ to enroll in coverage and receive income-based subsidies. You can contact GetCoveredNJ at r 1-833-677-1010 TTY 711.

New Jersey Division of Insurance

Regulates New Jersey’s insurance industry, and assists consumers and businesses with insurance-related questions and concerns.

New Jersey Family Care

Includes Medicaid and the Children’s Health Insurance Program (CHIP).

New Jersey State Health Insurance Assistance Program

A resource for people with questions about Medicare in New Jersey.

Looking for more information about other options in your state?

Need help navigating health insurance options in New jersey?

Explore more resources for options in NJ including short-term health insurance, dental, Medicaid and Medicare.

Speak to a sales agent at a licensed insurance agency.

Footnotes

- ”NJ Department of Banking and Insurance Releases Initial Health Insurance Rates for the Individual Market for Plan Year 2026” New Jersey Department of Banking and Insurance. Aug. 21, 2025 ⤶ ⤶

- ”Get Covered New Jersey Open Enrollment Kicks Off November 1 With Historic Levels of Financial Assistance Available” New Jersey Department of Banking and Insurance. Oct. 31, 2024 ⤶ ⤶ ⤶

- “Lower Your Monthly Premiums with the NJ Health Plan Savings” GetCoveredNJ. ⤶

- ”Responses to Assembly Budget Committee questions” New Jersey Department of Banking and Insurance. June 11, 2025 ⤶

- ”2026 Open Enrollment Update Final Snapshot: November 1, 2025 – January 31, 2026” Get Covered NJ. Accessed Feb. 27, 2026 ⤶ ⤶ ⤶

- New Jersey’s Health Coverage Requirement. New Jersey Department of the Treasury. Accessed November 2023. ⤶

- ”2026 OEP State-Level Public Use File (ZIP)” Centers for Medicare & Medicaid Services, Accessed July 9, 2026 ⤶ ⤶

- ”NJ Department of Banking and Insurance Releases Initial Health Insurance Rates for the Individual Market for Plan Year 2026” New Jersey Department of Banking and Insurance. Aug. 21, 2025 *The above is based on the most current data available. ⤶

- ”Frequently Asked Questions: Who can shop on Get Covered NJ?“ Get Covered NJ. Accessed Feb. 27, 2026 ⤶

- ”Lower Your Monthly Premiums with the NJ Health Plan Savings” Get Covered NJ. Accessed Feb. 27, 2026 ⤶

- Medicare and the Marketplace, Master FAQ. Centers for Medicare and Medicaid Services. Accessed Feb. 27, 2026 ⤶

- Premium Tax Credit — The Basics. Internal Revenue Service. Accessed Feb. 27, 2026 ⤶ ⤶

- Updates to frequently asked questions about the Premium Tax Credit. Internal Revenue Service. February 2024. ⤶

- “What is an open enrollment period?” Get Covered New Jersey Frequently Asked Questions. Accessed Oct. 31, 2025 ⤶

- Special Enrollment Period (SEP) Overview. Get Covered New Jersey. Accessed Feb. 27, 2026 ⤶

- New Law Establishing the New Jersey Easy Enrollment Health Insurance Program Aims to Improve Access to Affordable Health Coverage for Residents. New Jersey Department of Banking and Insurance. July 2022 ⤶

- Find Local Assistance. GetCoveredNJ. Accessed Feb. 27, 2026 ⤶

- “Lower Your Monthly Premiums with the NJ Health Plan Savings” GetCoveredNJ. Accessed Sep. 21, 2025 ⤶

- ”2025 Poverty Guidelines” U.S. Department of Health & Human Services. Accessed Oct. 31, 2025 ⤶

- ”2026 Marketplace Open Enrollment Period Public Use Files” CMS.gov. April 2026 ⤶ ⤶ ⤶ ⤶

- “2025 Marketplace Open Enrollment Period Public Use Files” CMS.gov, May 2025 ⤶ ⤶

- New Jersey’s ACA Section 1332 State Innovation Waiver. New Jersey Department of Banking and Insurance. Accessed November 2023. ⤶

- ”NJ Department of Banking and Insurance Releases Final Health Insurance Rates for the Individual Market for Plan Year 2026” New Jersey Department of Banking and Insurance. Oct. 27, 2025 ⤶ ⤶

- ”Find out how much insurance may cost” (zip 08002) Get Covered NJ. Accessed Oct. 31, 2025 ⤶

- Analysis Finds No Nationwide Increase in Health Insurance Marketplace Premiums. The Commonwealth Fund. December 2014. ⤶

- FINAL PROJECTION: 2016 Weighted Avg. Rate Increases: 12-13% Nationally* ACA Signups. October 2015. ⤶

- Avg. UNSUBSIDIZED Indy Mkt Rate Hikes: 25% (49 States + DC). ACA Signups. October 2016. ⤶

- New Jersey: Approved 2018 Rate Hikes: 22% On Average, Over Half Due Specifically To CSR/Mandate Sabotage. ACA Signups. October 2017. ⤶

- 2019 Rate Hikes. ACA Signups. October 2018. ⤶

- NJ Department of Banking and Insurance Releases Health Plan Rates. New Jersey Department of Banking and Insurance. October 2019. ⤶

- NJ Department of Banking and Insurance Announces 2021 Health Insurance Rate Changes, Lower Premiums Available for Most Marketplace Enrollees Due to New State Subsidies. New Jersey Department of Banking and Insurance. September 2020. ⤶

- NJ Department of Banking and Insurance Announces More Health Insurance Offerings in 2022, Record Levels of Financial Help Available for Another Year at Get Covered New Jersey. New Jersey Department of Banking and Insurance. September 2021. ⤶

- “NJ Department of Banking and Insurance Announces Expanded Health Insurance Options in 2023, Historic Levels of Financial Help Remain Available at Get Covered New Jersey” New Jersey Department of Banking and Insurance, Sept. 30, 2022. ⤶

- ”2024 IHC/SEH Average Rate Changes” New Jersey Department of Banking and Insurance. Accessed November 2023 ⤶

- “2025 Marketplace Open Enrollment Period Public Use Files” CMS.gov, May 2025 ⤶ ⤶

- “ASPE Issue Brief (2014)” ASPE, 2015 ⤶

- “Health Insurance Marketplaces 2015 Open Enrollment Period: March Enrollment Report”, HHS.gov, 2015 ⤶

- “HEALTH INSURANCE MARKETPLACES 2016 OPEN ENROLLMENT PERIOD: FINAL ENROLLMENT REPORT” HHS.gov, 2016 ⤶

- “2017 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2017 ⤶

- “2018 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2018 ⤶

- “2019 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2019 ⤶

- “2020 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2020 ⤶

- “2021 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2021 ⤶

- “2022 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2022 ⤶

- “Health Insurance Marketplaces 2023 Open Enrollment Report”CMS.gov, Accessed August 2023 ⤶

- ”HEALTH INSURANCE MARKETPLACES 2024 OPEN ENROLLMENT REPORT” CMS.gov, 2024 ⤶

- ”State-based Marketplace (SBM) Medicaid Unwinding Report” Centers for Medicare & Medicaid Services. Data through April 2024; Accessed Aug. 15, 2024 ⤶