Medicare in Maine

Original Medicare, Medicare Advantage, Part D prescription drug, and Medigap coverage in Maine

Medicare enrollment in Maine

As of February 2026, there were 388,058 residents enrolled in Medicare in Maine.1

Most Medicare beneficiaries are eligible for coverage because they’re at least 65 years old. But younger people gain Medicare eligibility if they have end-stage renal disease (ESRD) or amyotrophic lateral sclerosis (ALS), or after they’ve been receiving disability benefits for 24 months.

Nationwide, about 9% of Medicare beneficiaries are under the age of 65,2 but this is slightly higher in Maine, where 11% of Medicare beneficiaries were under 65 as of early-2026.1

- Read about Medicare’s open enrollment period and other important enrollment deadlines.

- Learn how Maine’s Medicaid program can provide assistance to Medicare beneficiaries with limited income and assets.

Medicare Advantage plan availability and enrollment in Maine

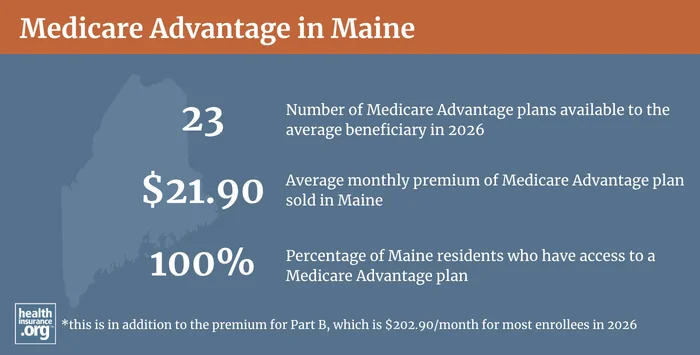

Nearly 59% of Maine’s Medicare beneficiaries were enrolled in Medicare Advantage plans as of February 2026.1 The remaining 41% of Maine’s Medicare beneficiaries had opted instead for coverage under Original Medicare.1 Nationwide, about 51% of all Medicare beneficiaries were enrolled in private Medicare Advantage plans as of February 2026.3

All counties in Maine have Medicare Advantage plans available, and the average Medicare beneficiary in Maine can choose from among 23 Medicare Advantage plans in 2026.4

Learn more about Medicare Advantage, Medicare’s annual open enrollment period, and the Medicare Advantage open enrollment period.

Sources: Medicare Advantage 2026 Spotlight: A First Look at Plan Offerings, KFF.org, Dec. 9, 2025; Fact Sheet: Medicare Open Enrollment for 2026, Centers for Medicare & Medicaid Services. Sep. 26, 2025

Learn about Medicare plan options in Maine by contacting a licensed agent.

Medicare supplement (Medigap) plan availability in Maine

For 2026, 15 insurers in Maine offer Medigap plans.5 And as of 2024, there were 55,561 Maine residents with Medigap coverage.6

People are granted a six-month window, when they turn 65 and enroll in Original Medicare, during which coverage is guaranteed issue for Medigap plans. Federal rules do not, however, guarantee access to a Medigap plan if you’re under 65 and eligible for Medicare as a result of a disability. And after the initial six-month open enrollment period ends, federal rules do not allow enrollees guaranteed-issue access to Medigap plans (including switching from one plan to another) unless they experience one of the limited situations that trigger a guaranteed-issue right.

But Maine has much more extensive Medigap regulations, designed to protect consumers and ensure greater access to Medigap. Maine’s rules are explained in the state’s Consumer Guide to Medicare Supplement Plans, and include several provisions:

- All Medigap insurers in Maine must designate at least one month per year when all applicants will be accepted for enrollment in Medigap Plan A, regardless of their medical history (Plan A offers the least amount of benefits). Insurers can be more lenient than this basic requirement and two insurers (Anthem Blue Cross Blue Shield and Washington National) offer year-round access to Medigap Plan A. The rest of the insurers have varying one-month windows when Plan A is available on a guaranteed-issue basis.7

- People under age 65 in Maine are granted the same six-month open enrollment period for guaranteed-issue Medigap plans (starting when they’re enrolled in Medicare Part B) as people who are 65 and enrolling in Medicare due to their age. These enrollees also have access to another six-month open enrollment period – during which they can switch to any Medigap plan on a guaranteed-issue basis – when they turn 65. Maine Rule 275, Section 11 clarifies that insurers cannot condition eligibility or premiums on a person’s medical history as long as they enroll during their six-month open enrollment window, or in the 60 days preceding it (to ensure that people can have a seamless transition to Medicare, with Medigap coverage effective the same day Medicare begins).8

- After the initial six-month window ends, Medigap enrollees in Maine are allowed to switch to a different plan from their current insurer or a different insurer, as long as they pick a plan with equal or lesser benefits (this chart on page 5 shows which plans are available, depending on the plan the person already has) and as long as they haven’t had a break of more than 90 days in their Medigap coverage since their initial open enrollment period.

- Medigap insurers in Maine must allow a Medicare beneficiary to enroll in a Medigap plan if they apply within 90 days of losing coverage under an individual market plan (not counting a short-term health plan or fixed indemnity plan), an employer-sponsored plan, or MaineCare (Medicaid).

- Maine is one of nine states where Medigap premiums cannot vary based on age,9 and that provision also includes people under age 65. (Some of the states that ban age-based Medigap premiums only apply that requirement to plans sold to people who are at least 65 years old). Medigap premiums in Maine only vary based on tobacco use.10

- Federal law gives people a “trial right” to try Medicare Advantage and then switch to Original Medicare instead, with guaranteed-issue access to Medigap as long as the person makes the switch to Original Medicare within a year. But Maine law extends that trial right period to three years. If a person in Maine signs up for Medicare Advantage when they’re first eligible for Medicare and then switches to Original Medicare within three years, they have a guaranteed-issue right to buy any Medigap plan available in their area, as long as they purchase it within 90 days of their Medicare Advantage plan ending.11

- Maine residents who have Medigap coverage and terminate it to switch to Medicare Advantage also have a three-year trial period, although it’s a little more restrictive. As long as they switch back to Original Medicare within three years and apply for a Medigap plan within 90 days of the Medicare Advantage plan ending, they have a guaranteed issue right to buy a Medigap plan with benefits that are equal to or less than their original Medigap plan’s benefits. (Again, this chart on page 5 shows which plans have equal or lesser benefits.)11

Learn what Medigap covers, who’s eligible for Medigap and when you can enroll.

Medicare Part D plan availability and enrollment in Maine

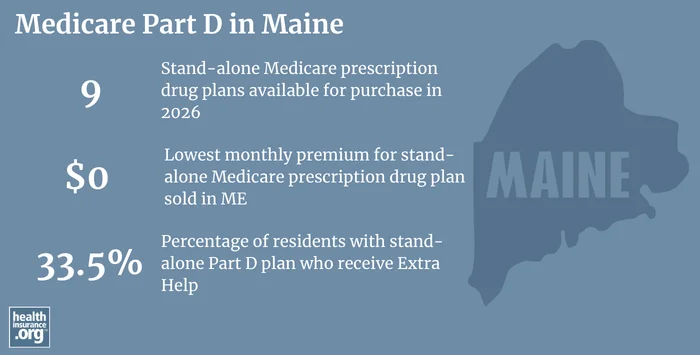

As of February 2026, there were 321,809 Medicare beneficiaries in Maine enrolled in Part D coverage.1 The majority of them – more than 213,000 – had Part D coverage integrated with Medicare Advantage plans.1 And there were also more than 108,000 who had stand-alone Part D plans.1

For 2026 coverage, there are 9 stand-alone Medicare Part D plans available in Maine, with premiums starting at $0 per month.12

Learn how Medicare Part D prescription drug coverage works, what it pays for, how and when to enroll.

Source: Fact Sheet: Medicare Open Enrollment for 2026, Centers for Medicare & Medicaid Services. Sep. 26, 2025

Resources for Medicare beneficiaries in Maine

Need help with your Medicare application in Maine, or have questions about Medicare eligibility in Maine? These resources provide free assistance and information.

- The Maine State Health Insurance Assistance Program can provide assistance with a wide range of topics related to Medicare in Maine

- The Maine Bureau of Insurance web site includes a page of frequently asked Medicare questions, as well as a page about Medigap.

- The Medicare Rights Center provides helpful information geared to Medicare beneficiaries, caregivers, and professionals.

Looking for more information about other options in your state?

Need help navigating health insurance options in Maine?

Explore more resources for options in ME including ACA coverage, short-term health insurance, dental and Medicaid.

Speak to a sales agent at a licensed insurance agency.

Footnotes

- “Medicare Monthly Enrollment – Maine” Centers for Medicare & Medicaid Services Data. Accessed June 2026. ⤶ ⤶ ⤶ ⤶ ⤶ ⤶ ⤶

- “Medicare Monthly Enrollment – US” Centers for Medicare & Medicaid Services Data, February 2026. ⤶

- “Medicare Monthly Enrollment – US” Centers for Medicare & Medicaid Services Data. Accessed June 2026. ⤶

- “Medicare Advantage 2026 Spotlight: First Look” KFF.org. Dec. 9, 2025 ⤶

- “A Consumer’s Guide to Medicare Supplement Insurance” Maine Bureau of Insurance. Nov. 2025. ⤶

- “The State of Medicare Supplement Coverage” AHIP. April 2026 ⤶

- “A Consumer’s Guide to Medicare Supplement Insurance” Maine Bureau of Insurance. November 2025. ⤶

- “Medicare FAQs” (First question includes a link that will allow a download of Rule 275.) Maine Bureau of Insurance. Accessed June 4, 2026 ⤶

- “Key Facts About Medigap Enrollment and Premiums for Medicare Beneficiaries” KFF.org. Oct. 18, 2024 ⤶

- “Medicare Supplement Annual Rates” Maine Bureau of Insurance. Accessed June 4, 2026 ⤶

- “Buy/Switch Outside Open Enrollment” Maine Bureau of Insurance. Accessed June 4, 2026 ⤶ ⤶

- “Fact Sheet: Medicare Open Enrollment for 2026” Centers for Medicare & Medicaid Services. Sep. 26, 2025. ⤶