Find Massachusetts Health Insurance Marketplace Coverage for 2026

Compare ACA plans and check subsidy savings from a licensed third-party health insurance agency.

Massachusetts Health Insurance Marketplace Guide

This guide, including the FAQs below, was created to help you better understand the health coverage options available to you and your family in Massachusetts. The options found in Massachusetts’s ACA Marketplace may be a good choice for many consumers.

Massachusetts residents use a fully state-based health insurance marketplace known as Massachusetts Health Connector to obtain ACA Marketplace plans offered by several private health insurance companies. Eight insurers are offering individual/family plans via MA Health Connector for 2026,1 all of which plan to continue to offer coverage in 20272 (See below for premium change details.)

Massachusetts also

- provides state-funded subsidies, in addition to the federal subsidies that are available nationwide. State-funded subsidies in Massachusetts became available to more people as of 2024, as described below. And for 2026, Massachusetts allocated more funding to the state-subsidy program to offset much of the reduction in federal subsidies caused by the expiration of the federal subsidy enhancements.3

- has stricter medical loss ratio requirement than most states (88%,4 as opposed to the 80% federal minimum),

- caps premiums for older enrollees at no more than double the rate for a 21-year-old (as opposed to a 3:1 ratio in most states),5

- requires residents to maintain health insurance or face a tax penalty, under a rule that predates the ACA.

- Has a merged individual and small group market, which means rates and rate changes are the same in both markets6 (subsidies offset a significant portion of premiums in the individual market, but not the small group market).

Massachusetts ACA Marketplace quick facts

Frequently asked questions about health insurance in Massachusetts

Who can buy Marketplace health insurance in Massachusetts?

To purchase health coverage through the Massachusetts Marketplace, you must:9

- Live in Massachusetts

- Be lawfully present in the United States

- Not be incarcerated

- Not be enrolled in Medicare

Eligibility for premium subsidies and cost-sharing reductions through the Marketplace depends on your income and how it compares with the cost of the second-lowest-cost Silver plan in your area. In addition, to qualify for financial assistance with your Marketplace plan you must:

- Not have access to affordable health coverage through your employer. If your employer offers coverage but you feel it’s too expensive, you can use our Employer Health Plan Affordability Calculator to see if you might qualify for premium subsidies in the Marketplace.

- Not be eligible for Medicaid (MassHealth).10

- If married, file taxes jointly with your spouse.11 (with very limited exceptions)12

- Not be able to be claimed by someone else as a tax dependent.11

It’s important to note that Massachusetts is one of the states that has its own individual mandate, and residents who don’t have health insurance are subject to a penalty when they file their state tax returns.13 The individual mandate in Massachusetts pre-dates the ACA. It was paused from 2014 through 2018, when there was a federal penalty for not having health insurance. Massachusetts revived the state-based penalty in 2019.

When can I enroll in an ACA-compliant plan in Massachusetts?

The open enrollment period for 2027 individual/family health coverage in Massachusetts runs from November 1, 2026 to December 23, 2026.14

This is shorter than the enrollment window has been in previous years, due to a federal rule change that prohibits states from extending open enrollment into January.

Outside of open enrollment, a qualifying life event is generally necessary to enroll in a plan or make coverage changes. But residents who are eligible for ConnectorCare can enroll anytime if they are newly eligible or haven’t previously enrolled.15

Massachusetts also has a “Simple Sign Up Program” that allows people to use their state tax return to gain access to health coverage.16 Several other states have similar programs (easy enrollment programs).

How do I enroll in a Massachusetts Marketplace plan?

To enroll in an ACA Marketplace plan in Massachusetts, you can:

- Visit the Health Connector to access Massachusetts’s state-based health insurance marketplace. Here you will find an online platform to shop, compare, and choose the best health plans.

- Purchase individual and family health coverage with the help of an insurance agent or broker, or a Navigator or certified application counselor.

How can I find affordable health insurance in Massachusetts?

Residents in Massachusetts use the Health Connector to enroll in Marketplace health coverage as well as to determine subsidy eligibility. Both non-standardized and standardized health plans are available through the Health Connector.17

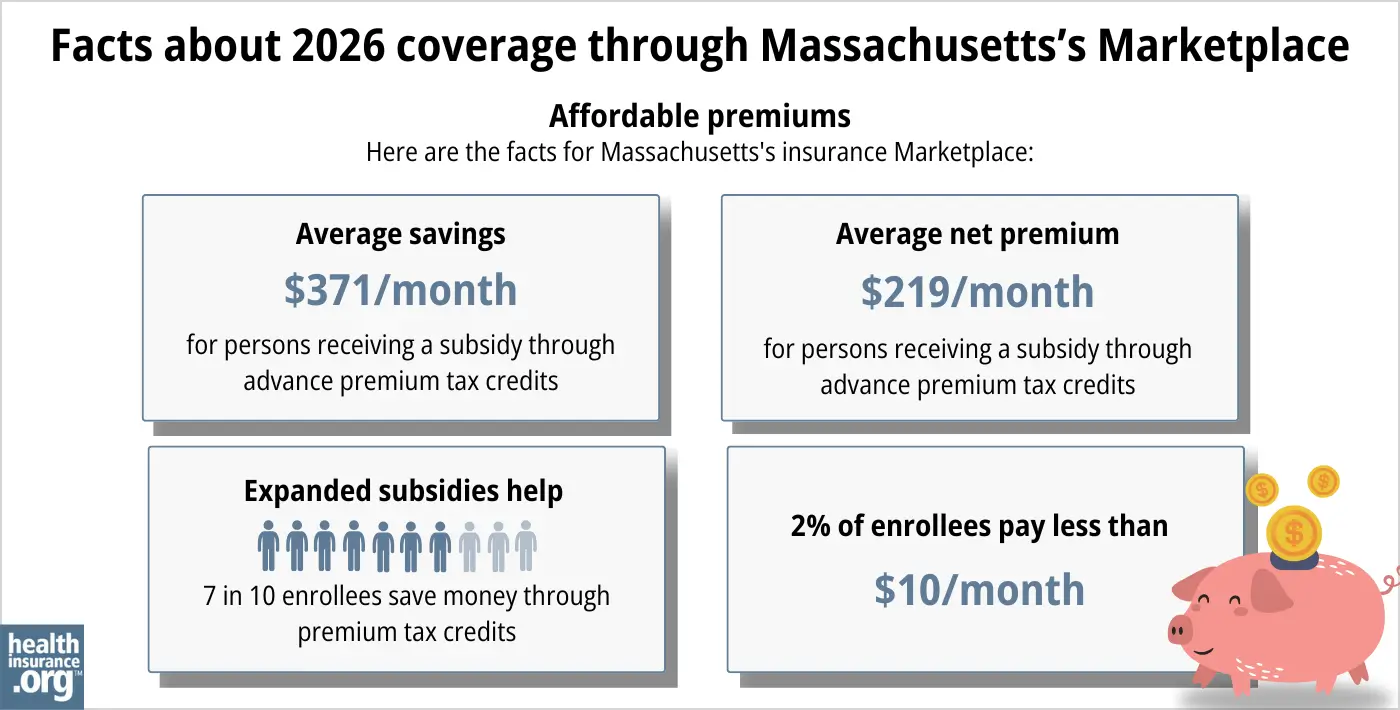

The Affordable Care Act provides income-based advance premium tax credits (subsidies) that offset premium payments to help keep your expenses down. More than 72% of Massachusetts Health Connector enrollees saved money on 2026 premiums. The average subsidy for these enrollees was $371/month, resulting in an average after-subsidy premium of $219/month (not counting state subsidies, discussed below).18

Source: CMS.gov18

In addition to federal subsidies, Massachusetts residents may also qualify for additional subsidies via the ConnectorCare program. ConnectorCare plans qualify for the federally funded ACA premium tax credits, but are also subsidized by the state, resulting in even lower premium and out-of-pocket costs for eligible residents.19

ConnectorCare was historically available to applicants with income up to 300% of the poverty level. But starting in 2024, ConnectorCare eligibility was expanded to 500% of the poverty level.20 The expansion was a two-year pilot program, initially slated to sunset at the end of 2025. The state’s 2026 Fiscal Year budget extended the pilot program for another year, allowing eligibility for ConnectorCare to continue to extend to 500% FPL in 2026.21

However, ConnectorCare subsidies are only available to enrollees who also get federal premium subsidies. Since those are no longer available as of 2026 due to the return of the “subsidy cliff,”ConnectorCare subsidies are also not available above 400% of FPL.22

In early 2026, Massachusetts officials announced that the state had allocated significant additional funding to the ConnectorCare program. This was done in an effort to mitigate much of the impact of the expiration of federal subsidy enhancements at the end of 2025. As a result, most enrollees with income up to 400% of the federal poverty level will see little or no impact from the expiration of the federal subsidy enhancements.3

ConnectorCare enrollment has been steadily increasing since mid-2023, due to the post-pandemic return to normal eligibility redeterminations and disenrollments for MassHealth (Medicaid). Many people who are no longer eligible for MassHealth are now eligible for ConnectorCare instead.23

The expansion of eligibility to 500% of the poverty level also helped to drive ConnectorCare enrollment to record-high levels.24 and 202525 A large majority of all 2025 Massachusetts Health Connector enrollees were in ConnectorCare.25

ConnectorCare plans are offered by the same insurers that offer other QHPs via MA Health Connector. There are seven plan variations available; access to each plan depends on the applicant’s income. The 2026 premiums range from $0/month (for those with income up to 150% FPL) to $235/month (for those with income between 300% and 400% FPL).26

How many insurers offer Marketplace coverage in Massachusetts?

Eight insurers are offering exchange plans in Massachusetts for 2026,27 all of which have filed plans for 2027 as well.2 Coverage areas vary from one insurer to another, so plan availability depends on where you live.

- Mass General Brigham Health Plan

- Boston Medical Center Health Plan/WellSense

- Fallon Community Health Plan

- Health New England (HNE)

- Tufts Health Public Plans, Inc.

- Blue Cross Blue Shield of Massachusetts

- Harvard Pilgrim Health Care, Inc.

- UnitedHealthcare

Are Marketplace health insurance premiums increasing in Massachusetts?

The following average rate changes have been proposed for 2027 for the merged individual and small group markets in Massachusetts, amounting to an overall average proposed rate increase of 12.9%, before subsidies are applied.2

Massachusetts’ ACA Marketplace Plan 2027 PROPOSED Rate Increases by Insurance Company |

|

|---|---|

| Issuer | Percent Increase |

| Mass General Brigham Health Plan | 13.5% |

| Boston Medical Center Health Plan /WellSense Health Plan | 11.9% |

| Fallon Community Health Plan | 25.7% |

| Health New England (HNE) | 11.1% |

| Tufts Health Public Plans, Inc. | 11.8% |

| Blue Cross Blue Shield of Massachusetts (BCBSMA/ HMO Blue) | 15.3% |

| Harvard Pilgrim Health Care, Inc. | 6.7% |

| UnitedHealthcare | 14.2% |

Source: Massachusetts Division of Insurance; Office of Consumer Affairs and Business Regulation2

Because Massachusetts has a merged individual and small-group market, each carrier’s rate changes apply to both individual and small-group plans.

For perspective, here’s a summary of how average premiums have changed in Massachusetts over time:

How many people are insured through Massachusetts’s Marketplace?

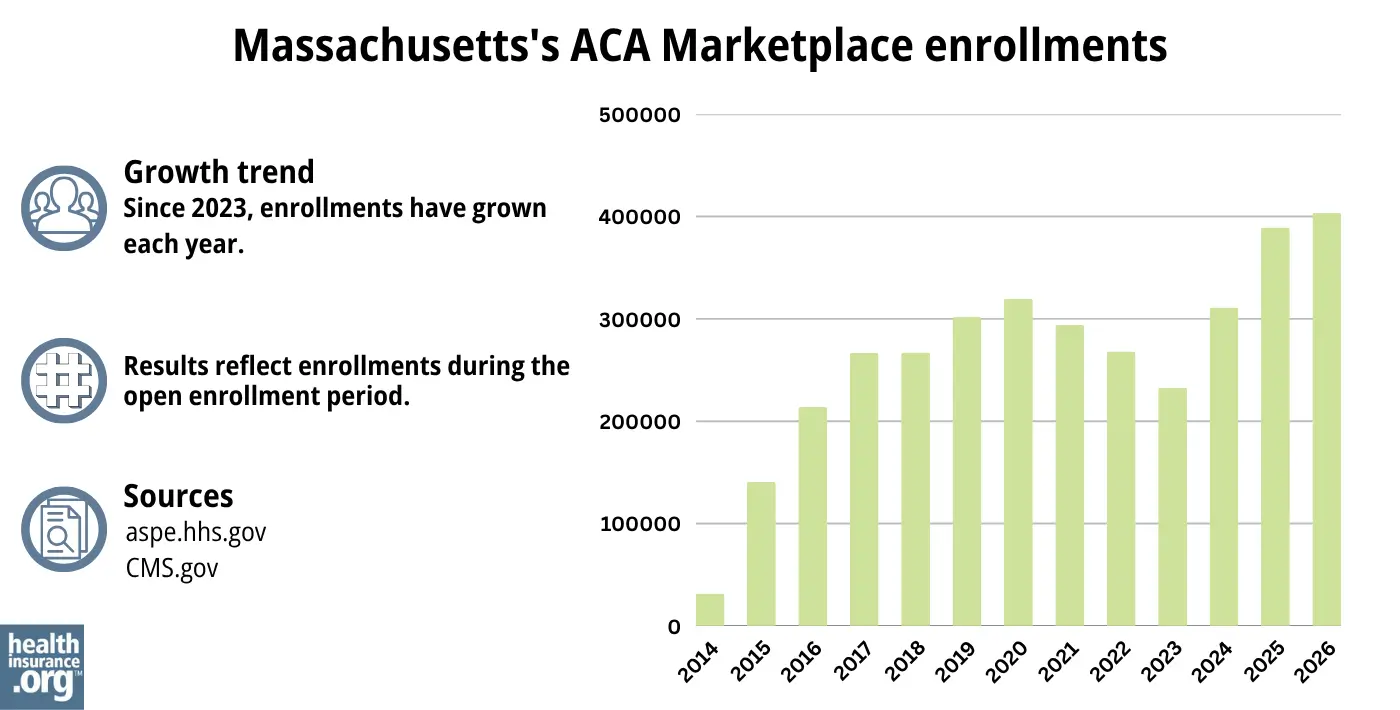

During the open enrollment period for 2026 coverage, 403,624 people enrolled in a health plan through the Massachusetts exchange.18

This was a record-high enrollment number (see chart below). The enrollment increase came even as most states saw a decline in Marketplace enrollment for 2026 due to the expiration of federal subsidy enhancements at the end of 2025. But Massachusetts is among the states where additional state-funded subsidies helped to offset some of the impact of the expiration of the federal subsidy enhancements.

Enrollment growth in 2024 and 2025 was also partly due to the “unwinding” of the pandemic-era continuous coverage rule for Medicaid. According to a CMS report, almost 98,000 Massachusetts residents transitioned from MassHealth to a Marketplace plan through Massachusetts Health Connector between April 2023 and September 2024, due to the “unwinding.”40

Source: 2014,41 2015,42 2016,43 2017,44 2018,45 2019,46 2020,47 2021,48 2022,49 2023,50 2024,51 202552 202618

What health insurance resources are available to Massachusetts residents?

Massachusetts Health Connector

877-MA-ENROLL (877-623-6765)

State Exchange Profile: Massachusetts

The Henry J. Kaiser Family Foundation overview of Massachusetts’s progress toward creating a state health insurance exchange.

Health Care for All – Massachusetts Consumer Assistance Program

Assists people insured by private health plans, Medicaid, or other plans in resolving problems pertaining to their health coverage; assists uninsured residents with access to care.(800) 272-4232

Office of Patient Protection, Department of Public Health

800-436-7757 (toll-free nationwide)

Serves residents and other consumers who receive health coverage from a Massachusetts carrier, insurer, or HMO.

Looking for more information about other options in your state?

Need help navigating health insurance options in Massachusetts?

Explore more resources for options in MA including short-term health insurance, dental, Medicaid and Medicare.

Speak to a sales agent at a licensed insurance agency.

Footnotes

- ”2026 Health Insurance Rates” Massachusetts Division of Insurance. Accessed Oct. 27, 2025 ⤶

- ”2027 Health Insurance Rates” Massachusetts Division of Insurance. Accessed June 9, 2026 ⤶ ⤶ ⤶ ⤶

- ”Governor Healey Details Strongest Plan in the Country to Protect Against President Trump’s ACA Cost Hikes” Massachusetts Health Connector. Jan. 8, 2026 ⤶ ⤶

- “Chapter 288; An Act to Promote Cost Containment, Transparency, and Efficiency in the Provision of Quality Health Insurance for Individuals and Small Businesses” Massachusetts Legislature ⤶

- “Market Rating Reforms State Specific Rating Variations” Centers for Medicare and Medicaid Services. ⤶

- ”Report of the Merged Market Advisory Council” Massachusetts Commissioner of Insurance. Accessed June 25, 2024 ⤶

- ”2026 OEP State-Level Public Use File (ZIP)” Centers for Medicare & Medicaid Services, Accessed July 9, 2026 ⤶ ⤶

- ”2026 Health Insurance Rates” Massachusetts Division of Insurance. Accessed July 11, 2025 *The above is based on the most current data available. ⤶

- ”Health Connector Policy: Eligibility to Purchase Individual and Family Plans” Massachusetts Health Connector. Apr. 7, 2025 ⤶

- ”Who is eligible for Marketplace premium tax credits?” KFF.org. Sep. 29, 2025 ⤶

- Premium Tax Credit — The Basics. Internal Revenue Service. Accessed Jan. 8, 2026 ⤶ ⤶

- Updates to frequently asked questions about the Premium Tax Credit. Internal Revenue Service. February 2024. ⤶

- “Health Care Reform for Individuals” Mass.gov. Apr. 8, 2025 ⤶

- ”When is Open Enrollment and when do Health Connector plans start?” Massachusetts Health Connector. Accessed Apr. 22, 2026 ⤶

- “ConnectorCare Health Plans” Massachusetts Health Connector. Accessed Oct. 27, 2025 ⤶

- Simple Sign Up Program. Massachusetts Health Connector. Accessed Oct. 27, 2025 ⤶

- “2026 Seal of Approval Submission Summary” Massachusetts Health Connector Board of Directors. July 9, 2025 ⤶

- ”2026 Marketplace Open Enrollment Period Public Use Files” CMS.gov. April 2026 ⤶ ⤶ ⤶ ⤶

- “ConnectorCare Plans: Affordable, high-quality coverage from the Health Connector” Massachusetts Health Connector. Accessed Oct. 27, 2025 ⤶

- ”Massachusetts expands access to affordable health care” Massachusetts Health Connector. Aug. 15, 2023. ⤶

- ”Governor Healey Signs $60.9 Billion Fiscal Year 2026 Budget” Mass.gov. July 4, 2025 ⤶

- ”Preliminary Eligibility: What does it mean and what do you need to do?” Massachusetts Health Connector. Sep. 2025 ⤶

- Massachusetts Health Connector Membership During MassHealth Redeterminations. Massachusetts Health Connector. December 2023. ⤶

- ”ConnectorCare Expansion Pilot Annual Report to the Legislature” Massachusetts Health Connector. July 2025 ⤶

- ”Health Connector Board Report Metrics” Massachusetts Health Connector. Mar. 2, 2025 ⤶ ⤶

- ”ConnectorCare Health Plans: Affordable, high-quality coverage from the Health Connector” Massachusetts Health Connector. Accessed Jan. 8, 2026 ⤶

- ”2026 Health Insurance Rates” Massachusetts Division of Insurance. Accessed July 11, 2025 ⤶

- “Final Award of 2015 Seal of Approval” Massachusetts Health Connector. ⤶

- ”Massachusetts health insurance costs set to rise by 6.3 percent in 2016” Mass Live. August 30, 2015. ⤶

- ”Board of the Commonwealth Health Insurance Connector Authority Minutes” September 8, 2016 ⤶

- ”2018 Rate Hikes” ACA Signups ⤶

- ”Health Connector Rates Going Up 4.7%” The Sun. September 13, 2018. ⤶

- ”Massachusetts: *Final* Avg. Unsubsidized 2020 Premiums: 5.2% Increase” ACA Signups. October 30, 2019. ⤶

- ”Do You Live In Massachusetts? You’ll Probably Pay More For Health Insurance Next Year” WGBH. September 17, 2020. ⤶

- ”Board of the Commonwealth Health Insurance Connector Authority Minutes” September 9, 2021 ⤶

- ”Final Award of the 2023 Seal of Approval (VOTE)” Massachusetts Health Connector Board of Directors Meeting, September 2022 ⤶

- 2024 Health Insurance Rates. Office of Consumer Affairs and Business Regulation, Mass.gov, Accessed August 2023 ⤶

- ”2025 Health Insurance Rates” Massachusetts Division of Insurance. Accessed Sep. 12, 2024 ⤶

- ”2026 Health Insurance Rates” Massachusetts Division of Insurance. And “2026 Rate Changes – Massachusetts: +11.7% avg. (updated)” ACA Signups. Oct. 20, 2025 ⤶

- ”State-based Marketplace (SBM) Medicaid Unwinding Report” Centers for Medicare & Medicaid Services. Data through Sep. 2024; Accessed Oct. 27, 2025 ⤶

- “ASPE Issue Brief (2014)” ASPE, 2015 ⤶

- “Health Insurance Marketplaces 2015 Open Enrollment Period: March Enrollment Report”, HHS.gov, 2015 ⤶

- “HEALTH INSURANCE MARKETPLACES 2016 OPEN ENROLLMENT PERIOD: FINAL ENROLLMENT REPORT” HHS.gov, 2016 ⤶

- “2017 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2017 ⤶

- “2018 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2018 ⤶

- “2019 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2019 ⤶

- “2020 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2020 ⤶

- “2021 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2021 ⤶

- “2022 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2022 ⤶

- “Health Insurance Marketplaces 2023 Open Enrollment Report”CMS.gov, Accessed August 2023 ⤶

- ”HEALTH INSURANCE MARKETPLACES 2024 OPEN ENROLLMENT REPORT” CMS.gov, 2024 ⤶

- “2025 Marketplace Open Enrollment Period Public Use Files” CMS.gov, May 2025 ⤶