Medicare in Alaska

Original Medicare, Medicare Advantage, Part D prescription drug, and Medigap coverage in Alaska

Medicare enrollment in Alaska

Medicare enrollment in Alaska stood at more than 122,000 people as of December 2025.1

Nationwide, almost 90% of Medicare beneficiaries are eligible due to their age, and the remaining 10% are eligible due to a disability.1 In Alaska, about 8% of Medicare beneficiaries are eligible as a result of a disability, while the rest are eligible due to being at least 65 years old.1

- Understand the difference between Medigap, Medicare Advantage, and Medicare Part D (including tips for picking the best coverage combination to meet your needs).

- Learn how Medicaid can provide assistance to Alaska Medicare beneficiaries who have limited financial resources.

Medicare Advantage plan availability and enrollment in Alaska

The vast majority of beneficiaries enrolled in Medicare in Alaska have coverage under Original Medicare.1 There are no individual Medicare Advantage plans for sale in Alaska as of the 2026 plan year.2

There were two Medicare Advantage plans available in Alaska in 2022 and 2023, both of which were Medicare Savings Account plans. (Here’s how those work. Note that this is not the same thing as a Medicare Savings Program, which is an assistance program available based on income and run by each state’s Medicaid office.)3

But as of the 2024 plan year, there were no individual Medicare Advantage plans available for purchase in Alaska,4 and that continued to be the case in 2025 and 2026. There are, however, some employer-sponsored Medicare Advantage plans (EGWPs) that cover some retirees in Alaska, including retired state employees.5

As of December 2025, just under 3% of Alaska’s Medicare beneficiaries had Medicare Advantage plans, including EGWPs. That amounted to 3,463 people out of more than 122,000 total Medicare beneficiaries in the state.1

Learn more about Medicare Advantage, Medicare’s annual open enrollment period, and the Medicare Advantage open enrollment period.

Learn about Medicare plan options in Alaska by contacting a licensed agent.

Medicare supplement (Medigap) enrollment and regulations in Alaska

Medigap plans are used to supplement Original Medicare, covering some or all of the out-of-pocket costs (for coinsurance and deductibles) that people would otherwise incur if they only had Original Medicare on its own.

Learn more about how Medigap plans are standardized and what they cover.

Under federal rules, Medicare beneficiaries have a six-month guaranteed-issue enrollment window for Medigap plans that starts when they turn 65 and enroll in Medicare Part B. But federal rules don’t guarantee access to Medigap plans if a person is under 65 years old and enrolled in Medigap as a result of a disability.

The majority of the states have adopted rules to ensure at least some access to Medigap plans for enrollees under the age of 65, but Alaska is not one of them.

As of 2026, there were no private Medigap insurers in Alaska that offered Medigap plans to enrollees under the age of 65.6

However, Alaska has kept its high-risk pool (the Alaska Comprehensive Health Insurance Association, also known as ACHIA) operational, and the pool serves as a backstop for people who are under 65 and in need of coverage to supplement Medicare. ACHIA offers four Medicare supplement options in 2026, with premiums that vary by age. (The highest premiums are for people under age 65.)7

Prior to the Affordable Care Act (ACA), many states relied on high-risk pools for people who needed to purchase their own health insurance and couldn’t qualify for coverage due to medical underwriting. Some states, including Alaska, still have an operational high-risk pool – and Medigap access is part of the reason ACHIA and similar programs in other states are still offering coverage. (Other states that have maintained their high-risk pools and use them to offer supplemental coverage to Medicare beneficiaries include Iowa, New Mexico, South Carolina, Washington, and Wyoming.)

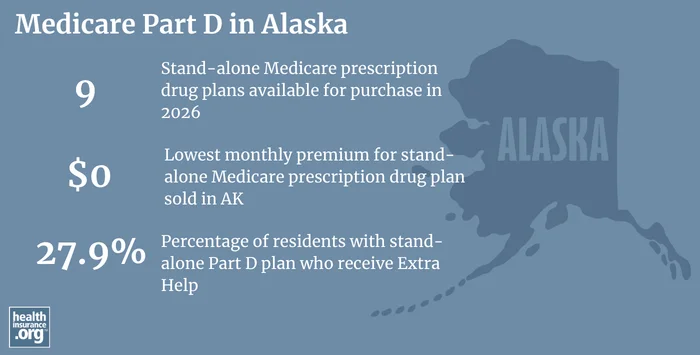

Medicare Part D plan availability and enrollment in Alaska

For 2026 coverage, insurers are offering nine stand-alone Part D plans to people who reside in Alaska, with premiums that start as low as $0/month.8

As of December 2025, there were more than 80,000 Alaska Medicare beneficiaries covered by stand-alone Medicare Part D prescription drug plans.1

Learn how Medicare Part D prescription drug coverage works, what it pays for, how and when to enroll.

Source: Fact Sheet: Medicare Open Enrollment for 2026, Centers for Medicare & Medicaid Services. Sep. 26, 2025

Resources for Medicare beneficiaries in Alaska

- If you have questions about Medicare enrollment in Alaska or Medicare eligibility in Alaska, you can contact the Alaska State Health Insurance Assistance Program.

- The Alaska Department of Health and Social Services, Senior and Disability Services can also provide a variety of helpful information and assistance for Medicare beneficiaries in Alaska. Here is the Medicare Information Office page on their website.

- The Alaska Division of Insurance oversees and regulates insurance companies that offer plans in the state (including Medigap insurers) as well as the agents and brokers who sell the policies. Their office can provide assistance and information to consumers and address complaints and inquiries about the entities they regulate.

Looking for more information about other options in your state?

Need help navigating health insurance options in Alaska?

Explore more resources for options in AK including ACA coverage, short-term health insurance, dental and Medicaid.

Speak to a sales agent at a licensed insurance agency.

Footnotes

- “Medicare Monthly Enrollment” Centers for Medicare & Medicaid Services. Accessed April 2026. ⤶ ⤶ ⤶ ⤶ ⤶ ⤶

- “Medicare Advantage 2026 Spotlight: A First Look at Plan Offerings” KFF.org. Dec. 9, 2025 ⤶

- “Help with Medicare Costs” State of Alaska. Accessed October, 2024. ⤶

- “Medicare Advantage 2026 Spotlight: A First Look at Plan Offerings” KFF.org Dec. 9, 2025 ⤶

- “Employer Group Waiver Plan” Alaska Department of Administration. Accessed November 2023. ⤶

- “Find a Medicare Plan” Medicare.gov. Accessed Apr. 22, 2026 ⤶

- “ACTION REQUIRED: 2026 Premium Rates & Coverage Renewal” Alaska Comprehensive Health Insurance Association. Nov. 2025 ⤶

- “Fact Sheet: Medicare Open Enrollment, 2026” Centers for Medicare & Medicaid Services. Sep. 26, 2025 ⤶