Medicare in Iowa

Original Medicare, Medicare Advantage, Part D prescription drug, and Medigap coverage in Iowa

Medicare enrollment in Iowa

As of February 2026, there were 704,561 residents with Medicare coverage in Iowa.1

In most cases, Medicare eligibility is triggered when a person turns 65. But younger people gain Medicare eligibility if they have end-stage renal disease (ESRD) or amyotrophic lateral sclerosis (ALS), or after they’ve been receiving disability benefits for 24 months. Nationwide, about 9% of Medicare beneficiaries are disabled and under age 65;2 in Iowa similarly, 9% of the Medicare population is under 65 and eligible for Medicare coverage enrollment due to a disability.1

- Read about Medicare’s open enrollment period and other important enrollment deadlines.

- Learn how Iowa’s Medicaid program can provide assistance to Medicare beneficiaries with limited income and assets.

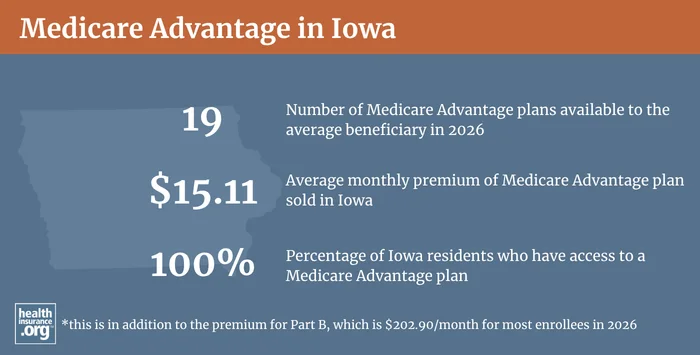

Medicare Advantage plan availability and enrollment in Iowa

Medicare Advantage plans are available in all areas of Iowa, and the average Medicare beneficiary in Iowa can choose from among 19 Medicare Advantage plans in 2026.3 The Iowa Medicare Advantage buyer’s guide shows premiums and benefit summaries for each of the insurers that offer Medicare Advantage plans in the state.

Nationwide, more than half of all Medicare beneficiaries had Medicare Advantage plans as of February 2026.4 However, in Iowa, it was 38%.1 Some Iowa Medicare beneficiaries are enrolled in Medicare Cost plans, which are another form of private Medicare coverage. The other 438,419 Iowa Medicare beneficiaries had coverage under Original Medicare.1

Learn more about Medicare Advantage, Medicare’s annual open enrollment period, and the Medicare Advantage open enrollment period.

Sources: Medicare Advantage 2026 Spotlight: A First Look at Plan Offerings, KFF.org, Dec. 9, 2025; Fact Sheet: Medicare Open Enrollment for 2026, Centers for Medicare & Medicaid Services. Sep. 26, 2025

Learn about Medicare plan options in Iowa by contacting a licensed agent.

Medicare supplement (Medigap) plan availability in Iowa

As of 2024, there were 298,527 Iowa Medicare beneficiaries enrolled in Medigap plans, according to an AHIP analysis.5 Learn how Medigap plans are standardized and what they cover.

There were 31 insurers offering Medigap plans in Iowa for 2026.6

Medigap plans in the state are governed by Chapter 37 of Iowa insurance statute.

Medigap insurers in Iowa can use issue-age rating (premiums are based on the age you were when you bought the policy), attained-age rating (premiums go up as you get older), or community rating (premiums don’t vary based on age). Almost all of the insurers in the state – all but AARP/UnitedHealthcare and Everence Association – use attained-age rating.6

Iowa considers legislation to create a limited annual window for Medigap plan changes

Unlike other private Medicare coverage (Medicare Advantage and Medicare Part D plans), there is no annual open enrollment window for Medigap plans. Instead, federal rules provide a one-time six-month window when Medigap coverage is guaranteed-issue. This window starts when a person is at least 65 and enrolled in Medicare Part B. (You must be enrolled in both Part A and Part B to buy a Medigap plan.)

Over the last few years, several pieces of legislation have been introduced in Iowa that would have created an annual open enrollment period for Medigap policies, but none of the bills have been successful.7 8 9 10 11 12 13

People who aren’t yet 65 can enroll in Medicare if they’re disabled and have been receiving disability benefits for at least two years, or if they have ALS or kidney failure. About 9% of Iowa’s Medicare beneficiaries are under age 65.14 But federal rules do not guarantee access to Medigap plans for people who are under 65.

The majority of the states have implemented rules to ensure that disabled Medicare beneficiaries have at least some access to Medigap plans, but Iowa is not among them. Medigap insurers in Iowa have the option to offer coverage to disabled enrollees who aren’t yet 65, but most do not. As of 2026, according to Iowa’s Medigap guide, only two insurers (United American and Wellmark) offer Medigap plans to people under 65, but the premiums are quite a bit more expensive than the rates for a 65-year-old.6

Disabled Medicare beneficiaries under age 65 in Iowa also have the option to enroll in HIPIOWA, the state’s high-risk health insurance pool. HIPIOWA has a plan that provides coverage to supplement Medicare, with premiums that vary based on age. Iowa is one of several states where state-run high-risk pools are still operational, with supplemental coverage available to Medicare beneficiaries who are unable to obtain private Medigap plans.

Disabled Medicare beneficiaries have access to the normal Medigap open enrollment period when they turn 65. At that point, they can select from among any of the available Medigap plans, with standard premiums that apply to non-disabled people who are enrolling when they turn 65.

Learn what Medigap covers, who’s eligible for Medigap and when you can enroll.

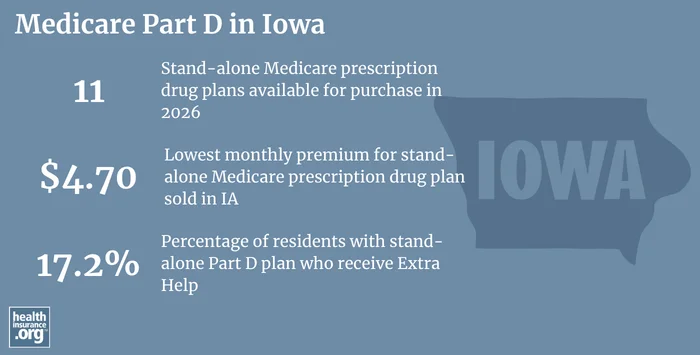

Medicare Part D plan availability and enrollment in Iowa

There are 11 stand-alone Medicare Part D plans for sale in Iowa for 2026, with premiums that start at $4.70/month.15

More than 370,095 Iowa residents had stand-alone Medicare Part D plans as of February 2026. Another 225,853 Iowa Medicare beneficiaries had Part D prescription coverage as part of their Medicare Advantage plans.1

Learn how Medicare Part D prescription drug coverage works, what it pays for, how and when to enroll.

Source: Fact Sheet: Medicare Open Enrollment for 2026, Centers for Medicare & Medicaid Services. Sep. 26, 2025

Resources for Medicare beneficiaries in Iowa

Need help with Medicare enrollment in Iowa, or have questions about Medicare eligibility or benefits? These resources provide free assistance and information.

- SHIIP, Iowa’s Senior Health Insurance Information Program, answers questions related to Medicare enrollment and coverage in Iowa. SHIIP has a Medigap shopping guide for Iowa, showing all of the available plans and prices.

- The Iowa Insurance Division answers questions and handles consumer complaints about health insurance companies that offer Medicare plans, as well as the agents and brokers who sell those plans. The Division also has a Medicare Resource Page.

- The Medicare Rights Center is a nationwide service, with a website and call center, that provides information and assistance related to Medicare enrollment, eligibility, and benefits.

- This resource about how Iowa Medicaid assists Medicare beneficiaries with limited financial means is a useful guide for beneficiaries and their caregivers.

Looking for more information about other options in your state?

Need help navigating health insurance options in Iowa?

Explore more resources for options in IA including ACA coverage, short-term health insurance, dental and Medicaid.

Speak to a sales agent at a licensed insurance agency.

Footnotes

- “Medicare Monthly Enrollment – Iowa” Centers for Medicare & Medicaid Services Data. Accessed June 2026. ⤶ ⤶ ⤶ ⤶ ⤶

- “Medicare Monthly Enrollment – US” Centers for Medicare & Medicaid Services Data, February 2026. ⤶

- “Medicare Advantage 2026 Spotlight: First Look” KFF.org. Dec. 9, 2025 ⤶

- “Medicare Monthly Enrollment – US” Centers for Medicare & Medicaid Services Data. Accessed June 2026. ⤶

- “The State of Medicare Supplement Coverage” AHIP. April 2026 ⤶

- “Iowa Medicare Supplement & Premium Comparison Guide” Iowa SHIIP. June 1, 2026 ⤶ ⤶ ⤶

- “Iowa SF2081” BillTrack50. Accessed June 7, 2026 ⤶

- “Iowa H.F.228” BillTrack50. Accessed June 7, 2026 ⤶

- “Iowa HF462” BillTrack50. Accessed June 7, 2026 ⤶

- “Iowa HF308” BillTrack50. Accessed June 7, 2026 ⤶

- “Iowa HF70” BillTrack50. Accessed June 7, 2026 ⤶

- “Iowa SF71” BillTrack50. Accessed June 7, 2026 ⤶

- “Iowa HF446” BillTrack50. Accessed June 7, 2026 ⤶

- “Medicare Monthly Enrollment – Iowa” Centers for Medicare & Medicaid Services Data. Accessed June 7, 2026 ⤶

- “Fact Sheet: Medicare Open Enrollment for 2026” Centers for Medicare & Medicaid Services. Sep. 26, 2025 ⤶