Medicare in South Carolina

Original Medicare, Medicare Advantage, Part D prescription drug, and Medigap coverage in South Carolina

In this article

Medicare enrollment in South Carolina

As of January 2026, there were 1,273,035 people enrolled in Medicare in South Carolina.1

People become eligible for Medicare either due to their age (turning 65) or due to a disability. In South Carolina, about 10% of Medicare beneficiaries were eligible due to a disability as of early 2026,1 while the rest were eligible due to their age. Nationwide, almost 91% of all Medicare beneficiaries are eligible due to their age.2

- Read about Medicare’s open enrollment period and other important enrollment deadlines.

- Learn how South Carolina’s Medicaid program can provide assistance to Medicare beneficiaries with limited income and assets.

Medicare Advantage plan availability and enrollment in South Carolina

In most areas of the country, Medicare beneficiaries have the option to get their coverage through Original Medicare (directly from the federal government) or from a private Medicare Advantage plan. There are pros and cons to either option.

Enrollment in Medicare Advantage plans has been steadily increasing nationwide3 and also in South Carolina. As of January 2026, about 46% of South Carolina Medicare beneficiaries had Medicare Advantage coverage.1

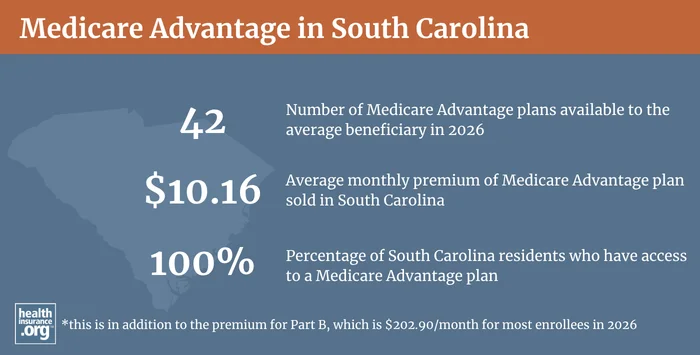

Medicare Advantage plans are marketed in all 46 counties in South Carolina in 2026. The average Medicare beneficiary in South Carolina can choose from among 42 Medicare Advantage plans in 2026.4

Learn more about Medicare Advantage, Medicare’s annual open enrollment period, and the Medicare Advantage open enrollment period.

Sources: Medicare Advantage 2026 Spotlight: A First Look at Plan Offerings, KFF.org, Dec. 9, 2025; Fact Sheet: Medicare Open Enrollment for 2026, Centers for Medicare & Medicaid Services. Sep. 26, 2025

Learn about Medicare plan options in South Carolina by contacting a licensed agent.

Medicare supplement (Medigap) plan availability in South Carolina

There were 275,034 people enrolled in Medigap plans in South Carolina in 2023, according to an AHIP report.5

There are 26 insurers offering Medigap plans in South Carolina in 2026.6

Federal rules do not guarantee access to Medigap plans for people who are under 65 and enrolled in Medicare due to a disability. The majority of the states have rules ensuring at least some access to Medigap plans for enrollees who are under the age of 65. South Carolina is among them, although the options are very limited and very expensive.

Instead of requiring insurers to offer Medigap plans to people under 65, South Carolina has maintained its pre-ACA high-risk pool and offers three guaranteed-issue Medigap plans through the high-risk pool, for Medicare beneficiaries who are under age 65. These beneficiaries can choose from among Medigap Plan A, Plan C, and Plan D via the high-risk pool.7 (Under federal rules, Medigap Plan C is only available to people who became eligible for Medicare prior to 2020.)8

The South Carolina Health Insurance Pool (SCHIP) allows these enrollees to purchase Medigap coverage when they would otherwise be unable to do so, but at a much higher cost: In 2026, Medigap Plan A is $1,191.09 per month,9 Medigap Plan C (only available to beneficiaries who became eligible for Medicare prior to 2020) is $1,510.33 per month,10 and Medigap Plan D is $1,406.01 per month.11

For perspective, premiums for Medigap Plan A for a 65-year-old non-smoking female ranges from $96/month to $423/month in 2026, according to Medicare’s plan finder tool.12 In states that have enacted laws requiring Medigap insurers to offer plans to people under the age of 65, the prices are typically higher, if the state allows it. But the high-risk pool Medigap premiums in South Carolina are several times more expensive than the average Medigap plan sold in the state.

People enrolled in SCHIP Medigap plans prior to turning 65 are granted the normal six-month guaranteed-issue Medigap Open Enrollment Period when they turn 65, and can switch to any available plan at that point, with the same pricing as any other 65-year-old.

Learn what Medigap covers, who’s eligible for Medigap and when you can enroll.

Medicare Part D plan availability and enrollment in South Carolina

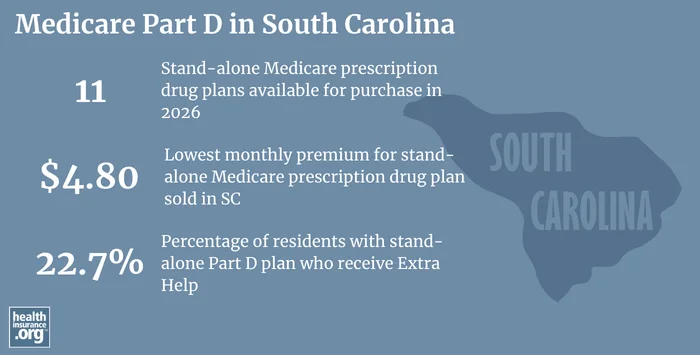

For 2026, there are 11 stand-alone Medicare Part D prescription drug plan options in South Carolina, with premiums that start as low as $4.80/month.13

Medicare Part D coverage in South Carolina is roughly equally split between stand-alone Medicare Part D prescription drug plans and Medicare Advantage Prescription Drug Plans (MA-PD): 488,991 Medicare beneficiaries in South Carolina were covered under stand-alone Medicare Part D prescription drug plans as of January 2026, and an additional 528,524 had Medicare Part D prescription drug plan coverage as part of their Medicare Advantage plans.1

Learn how Medicare Part D prescription drug coverage works, what it pays for, how and when to enroll.

Source: Fact Sheet: Medicare Open Enrollment for 2026, Centers for Medicare & Medicaid Services. Sep. 26, 2025

Resources for Medicare beneficiaries in South Carolina

If you need help with Medicare eligibility in South Carolina or Medicare enrollment in South Carolina, you can contact South Carolina’s Insurance Counseling Assistance and Referral for Elders, the state’s State Health Insurance Assistance Program (SHIP), with questions related to Medicare coverage in South Carolina.

The South Carolina Department of Insurance provides customer service and assistance with a wide range of insurance-related issues. The Department is responsible for regulating and overseeing Medigap insurers, and also licenses the insurers that sell Medicare Advantage and Medicare Part D prescription drug plans in the state (but most regulatory oversight of Medicare Advantage and Medicare Part D prescription drug plans is conducted at the federal level, by Centers for Medicare and Medicaid Services). The South Carolina Department of Insurance has a resource called “Making sense of health insurance after retirement,” which provides useful information to people with Medicare and people who aren’t yet eligible for Medicare.

The Medicare Rights Center is a nationwide service that can provide a wide range of information and assistance related to Medicare enrollment, eligibility, and benefits.

This page provides information about how South Carolina Medicaid can help Medicare beneficiaries who have limited financial means.

Looking for more information about other options in your state?

Need help navigating health insurance options in South Carolina?

Explore more resources for options in SC including ACA coverage, short-term health insurance, dental and Medicaid.

Speak to a sales agent at a licensed insurance agency.

Footnotes

- “Medicare Monthly Enrollment – South Carolina” Centers for Medicare & Medicaid Services Data. Accessed May 2026. ⤶ ⤶ ⤶ ⤶

- “Medicare Monthly Enrollment – US” Centers for Medicare & Medicaid Services Data. Accessed May 2026. ⤶

- “Medicare Advantage Enrollment Grew by About 1 Million People, Mainly Due to Special Needs Plans” KFF.org. Feb. 23, 2026 ⤶

- “Medicare Advantage 2026 Spotlight: First Look” KFF.org. Dec. 9, 2025 ⤶

- “The State of Medicare Supplement Coverage” AHIP. May 2025 ⤶

- “Explore your Medicare coverage options” Medicare.gov. Accessed May 15, 2026 ⤶

- “South Carolina Health Insurance Pool” South Carolina Department of Insurance. Accessed May 15, 2026 ⤶

- “South Carolina Health Insurance Pool (SCHIP), Plan C” doi.sc.gov, Accessed May 15, 2026 ⤶

- “South Carolina Health Insurance Pool (SCHIP), Plan A” doi.sc.gov. Accessed May 15, 2026 ⤶

- “South Carolina Health Insurance Pool (SCHIP), Plan C” doi.sc.gov. Accessed May 15, 2026 ⤶

- “South Carolina Health Insurance Pool (SCHIP), Plan D” doi.sc.gov. Accessed May 15, 2026 ⤶

- “Supplement Insurance (Medigap) Plans in South Carolina” Medicare.gov, Accessed May 15, 2026 ⤶

- “Fact Sheet: Medicare Open Enrollment for 2026” Centers for Medicare & Medicaid Services. Sep. 26, 2025 ⤶