Medicare in Vermont

Original Medicare, Medicare Advantage, Part D prescription drug, and Medigap coverage in Vermont

Medicare enrollment in Vermont

Nationwide, nearly 70 million people were enrolled in Medicare as of late 2025.1 As of December 2025, there were 169,197 Vermont residents covered by Medicare in Vermont.2

Most people attain Medicare eligibility in Vermont when they turn 65, but Medicare also provides coverage for more than 7 million disabled individuals under the age of 65. Nationwide, about 10% of Medicare beneficiaries are under age 65;1 in Vermont, about 11% of Medicare beneficiaries – 18,278 people – are under the age of 65 and eligible due to a disability.2

- Read about Medicare’s open enrollment period and other important enrollment deadlines.

- Learn how Vermont’s Medicaid program can provide assistance to Medicare beneficiaries with limited income and assets.

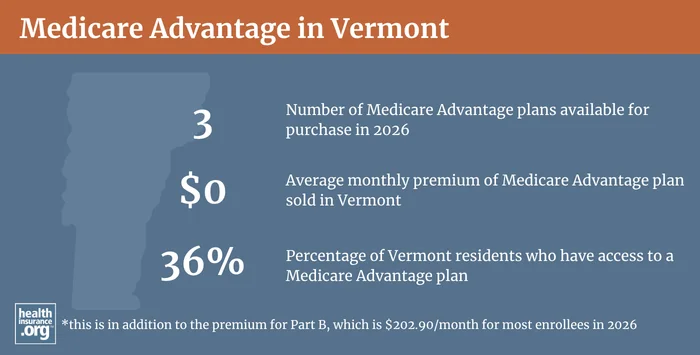

Medicare Advantage plan availability and enrollment in Vermont

Nationwide, a little more than half of all Medicare beneficiaries had Medicare Advantage plans as of late 20251 But in Vermont, just 31% of the state’s Medicare beneficiaries were enrolled in Medicare Advantage plans at that point.2

Medicare Advantage plans are provided by private insurers, so plan availability varies by area. Vermont has 14 counties, and the number of available Medicare Advantage plan options for 2026 varies from 0 to 3, depending on the county. In eight of Vermont’s counties, there are no Medicare Advantage plans available in 20263 Although there were Medicare Advantage plans available state-wide in 2025, only about 36% of Vermont Medicare beneficiaries have access to Medicare Advantage plans in 2026.4

Medicare Advantage plans provide all of the benefits of Medicare Part A (hospital coverage) and Part B (outpatient/medical coverage), and most plans also incorporate Part D coverage (prescription drugs) as well as extra benefits like dental and vision coverage, gym memberships, and a nurse hotline. But out-of-pocket costs (deductible, coinsurance, copays) vary under Advantage plans and are not the same as a person would have under Medicare Part A and B plus a Medigap plan. There are pros and cons to each option, and no single solution that works for everyone.

Medicare beneficiaries can switch from Original Medicare to Medicare Advantage enrollment, and vice versa, during the annual election period each fall (October 15 through December 7), with coverage effective January 1.

Read our guide to Medicare open enrollment.

There is also a Medicare Advantage open enrollment period (January 1 to March 31) during which people who are already enrolled in Medicare Advantage plans can switch to a different Medicare Advantage plan or drop their Medicare Advantage plan and enroll in Original Medicare instead.

Learn more about Medicare Advantage benefits, premium costs, plan eligibility and enrollment.

Sources: Medicare Advantage 2026 Spotlight: A First Look at Plan Offerings, KFF.org, Dec. 9, 2025; Fact Sheet: Medicare Open Enrollment for 2026, Centers for Medicare & Medicaid Services. Sep. 26, 2025

Learn about Medicare plan options in Vermont by contacting a licensed agent.

Medicare supplement (Medigap) plan availability in Vermont

There are 16 insurers that offer Medigap plans in Vermont in 2026.5 On the Vermont Department of Financial Regulation’s website, you’ll find an extensive guide that provides information about Medigap plans in the state.

According to an AHIP analysis, there were 50,277 Vermont Medicare beneficiaries with Medigap plans as of 2023.6

In most states, Medigap carriers can price plans using attained-age rating (rates increase as the enrollee gets older), issue-age rating (rates are based on the age the person was when they enrolled), or community rating (rates do not vary based on age). Vermont does not allow Medigap insurers to use attained-age rating7 and instead requires community rating as long as the enrollee is at least 65 years old. (Very few states require this.8 Vermont’s consumer protection is strong in terms of rating rules.) So in Vermont, rates for a given plan only vary based on whether the enrollee is under 65 or 65+.9 (Vermont is also one of only two states where insurers offering non-Medicare individual market coverage are also required to charge the same price regardless of how old an enrollee is.)10

Under federal rules, people are granted a six-month window during which they can enroll in a Medigap plan regardless of their medical history. This window starts when they’re at least 65 and enrolled in Medicare Part B. Federal rules do not, however, guarantee access to a Medigap plan if you’re under 65 and eligible for Medicare as a result of a disability.

To address this, the majority of the states have implemented rules ensuring at least some access to Medigap plans for people who are under age 65, and Vermont is among them. Vermont requires Medigap insurers to make all of their plans available to Medicare beneficiaries, regardless of age, during the first six months after the person is enrolled in Medicare Part B.11

It’s important to note, however, that Vermont’s guaranteed-issue provision does not apply to people under 65 who are eligible for Medicare due to end-stage renal disease.12

Learn more about Medicare supplement insurance (Medigap) covers, eligibility and plan costs.

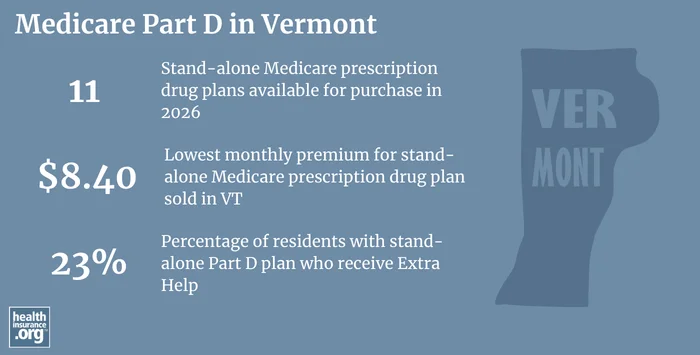

Medicare Part D plan availability and enrollment in Vermont

As of December 2025, 85,393 Vermont Medicare beneficiaries had stand-alone Medicare Part D prescription drug plans, and another 49,245 had Part D coverage integrated with their Medicare Advantage coverage.2 In total, about 80% of Vermont’s Medicare beneficiaries had Part D coverage, either as a stand-alone plan or as part of an Advantage plan.2

For 2026 coverage, there are 11 stand-alone Medicare Part D plans available in Vermont, with premiums starting at $8.40 per month.13

Learn how Medicare Part D prescription drug coverage works, what it pays for, how and when to enroll.

Source: Fact Sheet: Medicare Open Enrollment for 2026, Centers for Medicare & Medicaid Services. Sep. 26, 2025

Resources for Medicare beneficiaries in Vermont

Questions about Medicare in Vermont?

- The Vermont State Health Insurance Program can help with questions related to Medicare enrollment, eligibility, or coverage in Vermont.

- The Vermont Department of Financial Regulation, Insurance Division, oversees and licenses health insurance companies, brokers, and agents in Vermont. They can answer questions, provide information, and address consumer complaints about entities licensed under their authority.

- The Medicare Right Center provides information and assistance to Medicare beneficiaries and their caregivers.

- Medicare beneficiaries with low income and assets can get assistance through Vermont’s Medicaid program.

Looking for more information about other options in your state?

Need help navigating health insurance options in Vermont?

Explore more resources for options in VT including ACA coverage, short-term health insurance, dental and Medicaid.

Speak to a sales agent at a licensed insurance agency.

Footnotes

- “Medicare Monthly Enrollment, December 2025 – US” Centers for Medicare & Medicaid Services Data, Accessed Apr. 20, 2026 ⤶ ⤶ ⤶

- “Medicare Monthly Enrollment, December 2025 – Vermont” Centers for Medicare & Medicaid Services Data. Accessed Apr. 20, 2026 ⤶ ⤶ ⤶ ⤶ ⤶

- “Medicare Advantage 2026 Spotlight: A First Look at Plan Offerings” KFF.org Dec. 9, 2026 ⤶

- ”Fact Sheet: Medicare Open Enrollment in Vermont, 2026” And “Fact Sheet: Medicare Open Enrollment in Vermont, 2025” Centers for Medicare & Medicaid Services. Accessed Apr. 20, 2026 ⤶

- “Age 65+ Monthly Medicare Supplement Rates of Standardized Plans” Vermont Department of Financial Regulation. Accessed Apr. 20, 2026 ⤶

- “The State of Medicare Supplement Coverage” AHIP. May 2025 ⤶

- “Medicare Supplement Insurance Minimum Standards Rule” See section 15, Subsection F. Vermont.gov. Accessed Apr. 17, 2026 ⤶

- “Medigap Enrollment and Consumer Protections Vary Across States” KFF.org. Jul. 11, 2018 ⤶

- “Medicare Supplement Rates” Vermont.gov. August 2025 ⤶

- “Market Rating Reforms” CMS.gov. Dec. 10, 2021 ⤶

- “Shopping for Medicare Supplement Insurance” Vermont Department of Financial Regulation. Accessed Apr. 20, 2026 ⤶

- “Act 99 Report: Medicare Supplement Open Enrollment Study. Vermont Department of Financial Regulation. January 24, 2023 ⤶

- “Fact Sheet: Medicare Open Enrollment in Vermont 2026” (137) Centers for Medicare & Medicaid Services. Sep. 26, 2025 ⤶