Find Minnesota Health Insurance Marketplace Coverage for 2026

Compare ACA plans and check subsidy savings from a licensed third-party health insurance agency.

Minnesota Health Insurance Marketplace Guide

We’ve compiled this guide, including the FAQs below, to help you choose the right health insurance plan for you and your family. An ACA Marketplace/exchange plan – or Obamacare – is a good option for many people who don’t have access to Medicare, Medicaid, or employer-sponsored health insurance. We’re here to walk you through how the Marketplace works, and understand the available financial assistance.

In Minnesota, you can sign up for ACA Marketplace coverage through MNsure, the state’s health insurance exchange/Marketplace, where six private insurers offer health insurance policies. There will be some carrier changes for 2027, including one consolidation and one new insurer; see below for details regarding carrier participation and premium changes. If eligible, you may also get help to lower your monthly insurance cost (premium) and your out-of-pocket expenses through MNsure.

People in Minnesota can also sign up for MinnesotaCare – Minnesota’s Basic Health Program – or income-based Medical Assistance (Medicaid) through MNsure. If you’re eligible for one of these programs based on your income, MNsure will let you know and guide you through the enrollment process.1

Frequently asked questions about health insurance in Minnesota

Who can buy Marketplace health insurance in Minnesota?

To be eligible to enroll in private health coverage through the Marketplace in Minnesota (MNsure), you must:

- Be a Minnesota resident

- Be either a United States citizen or national, or be lawfully present

- Not be incarcerated

- Not have Medicare coverage

While most Minnesota residents are eligible to enroll in individual/family coverage through MNsure, eligibility for financial assistance (premium subsidies and cost-sharing reductions) is different. It depends on your income, and to qualify for financial assistance with your Marketplace plan you must also:

- Not be eligible to enroll in an affordable employer-sponsored health insurance plan. If your employer (or your spouse’s employer) offers coverage but you feel it’s too expensive, you can use our Employer Health Plan Affordability Calculator to see if you might qualify for premium subsidies in the Marketplace.

- Not be eligible for Medical Assistance (Minnesota Medicaid) or MinnesotaCare.

- Not be eligible for premium-free Medicare Part A.4

- If married, file a joint tax return with your spouse.5 (with very limited exceptions)6

- Not be able to be claimed by someone else as a tax dependent.5

When can I enroll in an ACA-compliant plan in Minnesota?

In Minnesota, the open enrollment period for a 2027 ACA-compliant individual or family health plan is currently scheduled to run from November 1, 2026, to December 31, 2026.7

This is shorter than the enrollment window that was used for the last several years, due to a federal rule change requiring open enrollment to end no later than December 31. However, a judge vacated that federal rule in June 2026.8 Depending on whether that ruling is appealed, Minnesota may revert to a January 15 deadline for open enrollment; these details were still unresolved as of June 2026.

To enroll or switch plans outside of the open enrollment window, you’ll need a qualifying life event.9

Enrollment in Medical Assistance (Medicaid) and MinnesotaCare (the state’s Basic Health Program) is available year-round. And Native Americans can enroll in Marketplace plans through MNsure year-round.

How do I enroll in a Marketplace plan in Minnesota?

To enroll in an ACA Marketplace plan in Minnesota, you can:

- Visit MNsure – Minnesota’s health insurance marketplace. MNsure provides an online platform to shop, compare, and choose the best health plans.

- Purchase individual and family health coverage through insurance agents or brokers, or with help from an MNsure Navigator.10

You can also call MNsure’s contact center by dialing 651-539-2099 (or 855-366-7873 if you’re outside the Twin Cities). The contact center operates from 8 a.m. to 4 p.m. from Monday to Friday.

How can I find affordable health insurance in Minnesota?

You may find affordable health insurance options in Minnesota by signing up through MNsure.

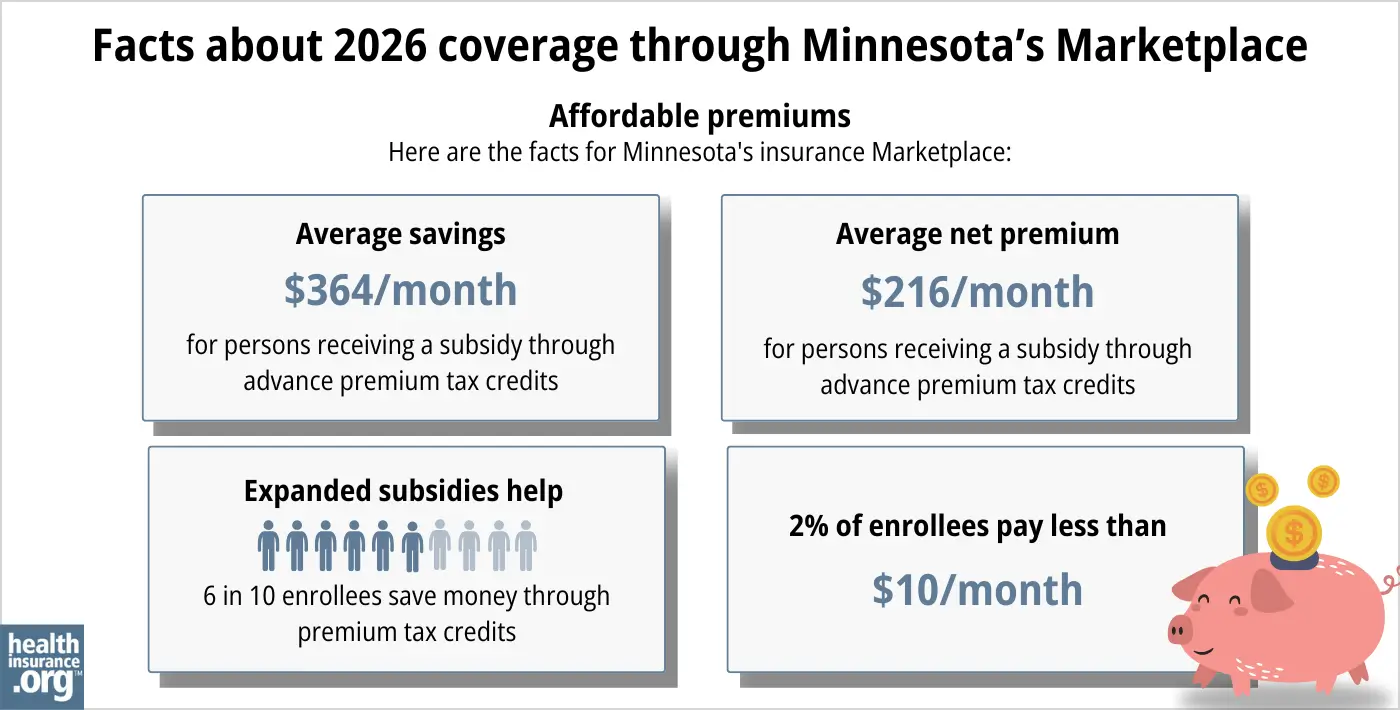

Under the Affordable Care Act, there are income-based subsidies – a type of financial assistance – called Advance Premium Tax Credits (APTC). APTCs can help lower your premium payments and reduce your overall expenses.

However, of the people who selected a plan through MNsure during the open enrollment period for 2026 coverage, just under 50% were eligible for APTC,11 down from 61% the year before.12 The reduction in the number of people eligible for APTC was due to the expiration of federal subsidy enhancements at the end of 2025, which caused the return of the “subsidy cliff.“13

Note: The percentage of subsidy-eligible enrollees is lower in Minnesota than in most states, and the average APTC amount is also lower in Minnesota. But that’s because Minnesota has a Basic Health Program for people earning up to 200% of the federal poverty level. So while individuals with income under 200% of FPL qualify for large premium subsidies in other states, they instead qualify for premium-free or very low-cost Basic Health Program coverage in Minnesota.

Source: CMS.gov 14

If your household income is no more than 250% of the federal poverty level, you may also qualify for cost-sharing reductions (CSR). These reductions can lower your deductibles and out-of-pocket expenses. Combining APTCs and CSRs might make an ACA plan the most budget-friendly health insurance choice for you.

You can also find inexpensive health insurance through Medicaid (called Medical Assistance in Minnesota). Check to see if you meet the criteria for Medicaid in Minnesota.

If your income is too high for Medical Assistance but not more than 200% of the poverty level, you may find that you’re eligible for MinnesotaCare. This is the state’s Basic Health Program, which we referenced above as a reason for MNsure’s smaller-than-average premium subsidies, and smaller percentage of subsidy-eligible enrollees.

Minnesota also has a reinsurance program, which helps to keep premiums lower than they would otherwise be for people whose income is too high to qualify for premium subsidies.15

But the reinsurance program’s waiver is currently only approved through 2027.16 Legislation introduced in 2026 would have directed the state to seek an extension for the reinsurance program, but the measures did not advance.17

Lawmakers have warned that the expiration of the reinsurance program would drive premiums significantly higher.18 But it’s important to understand that reinsurance really only keeps premiums lower for the people who don’t qualify for a premium subsidy (in Minnesota, that’s about half of the Marketplace enrollees, plus anyone who buys individual market coverage outside of MNsure).

For those who do get subsidies, the subsidies are smaller with the reinsurance program in place (because the reinsurance program drives down the price of the benchmark plan on which subsidy amounts are based). Without the reinsurance program, those subsidies would be larger.

How many insurers offer Marketplace coverage in Minnesota?

Six insurers offer exchange plans in Minnesota for 2026,19

- Blue Plus

- HealthPartners, Inc.

- Health Partners Insurance Company (new to MNsure for 2026)

- Medica

- UCare

- Quartz

Plan availability varies by area, but most Minnesotans can choose from at among at least three insurers’ plans for 2026.20

For 2027, however, there will be some changes:

- UCare plans will no longer be available.21 UCare was acquired by Medica in early 2026,22 and while the plans have been maintained separately for the 2026 plan year, only the Medica-branded plans will be available for 2027.

- Aspirus Health Plan is joining MNsure for 2027, with plans that will be available for purchase when open enrollment begins in November 2026.21

HealthPartners Insurance Company, which was new to MNsure for 2026, is affiliated with HealthPartners, Inc., which already offered MNsure plans in 2025. Some existing HealthPartners, Inc. enrollees were moved to plans offered by HealthPartners Insurance Company, unless they selected a different option during open enrollment.19

Are Marketplace health insurance premiums increasing in Minnesota?

For 2027, the following average rate changes have been proposed by the insurers that offer individual/family coverage through MNsure,21 amounting to a weighted average rate increase of just under 12%.23

Minnesota’s ACA Marketplace Plan 2027 PROPOSED Rate Increases by Insurance Company |

|

|---|---|

| Issuer | Percent Increase |

| Aspirus Health Plan | New for 2027 |

| Blue Plus | 10.3% |

| HealthPartners, Inc. | 12.4% |

| Medica | 13% |

| UCare | Acquired by Medica |

| Quartz | 10% |

| HealthPartners Insurance Company | 12.3% |

Source: Minnesota Commerce Department21

The average proposed rate increases are for full-price plans. However, about half of the people who were enrolled in private plans through MNsure in 2026 were getting premium tax credits that helped to reduce their premium costs.24 For these enrollees, net premium changes depend on how much their own plan’s premium changes, as well as how much their subsidy amount changes.

Subsidies are adjusted each year to match changes in the benchmark plan (the second-lowest-cost Silver plan) in each area. Unfortunately, the subsidy enhancements that had been in effect since 2021 expired at the end of 2025. This resulted in people having to pay a larger share of the premium themselves, and fewer people qualifying for subsidies. This will continue to be the case in 2027 and future years.

In Minnesota, about half of MNsure enrollees were eligible for premium subsidies in 2026, versus about 61% in 2025. And the average after-subsidy premium (across all enrollees) in 2026 was $437/month, versus $307/month in 2025.25

Here are examples of the sort of premium increases that people experienced in Minneapolis for 2026:26

- 40-year-old earning $40,000:

- Lowest-cost plan in 2025 was $105/month

- Lowest-cost plan in 2026 is $240/month

- 60-year-old earning $63,000:

- Lowest-cost plan in 2025 was $345/month

- Lowest-cost plan in 2026 is $722/month

For perspective, here’s an overview of how average full-price premiums have changed over time in Minnesota’s individual/family health insurance market:

- 2015: Average increase of 4.5%27

- 2016: Average increase of 41.4%28

- 2017: Average increase of 56.6%29

- 2018: Average decrease of 5.3%30

- 2019: Average decrease of 12.4%31

- 2020: Average decrease of 1%32

- 2021: Average increase of 2%33

- 2022: Average increase of 9.5%34

- 2023: Average increase of 1.5%35

- 2024: Average increase of about 4.5%36

- 2025: Average increase of about 8.8%37

- 2026: Average increase of about 22%1938

How many people are insured through Minnesota’s Marketplace?

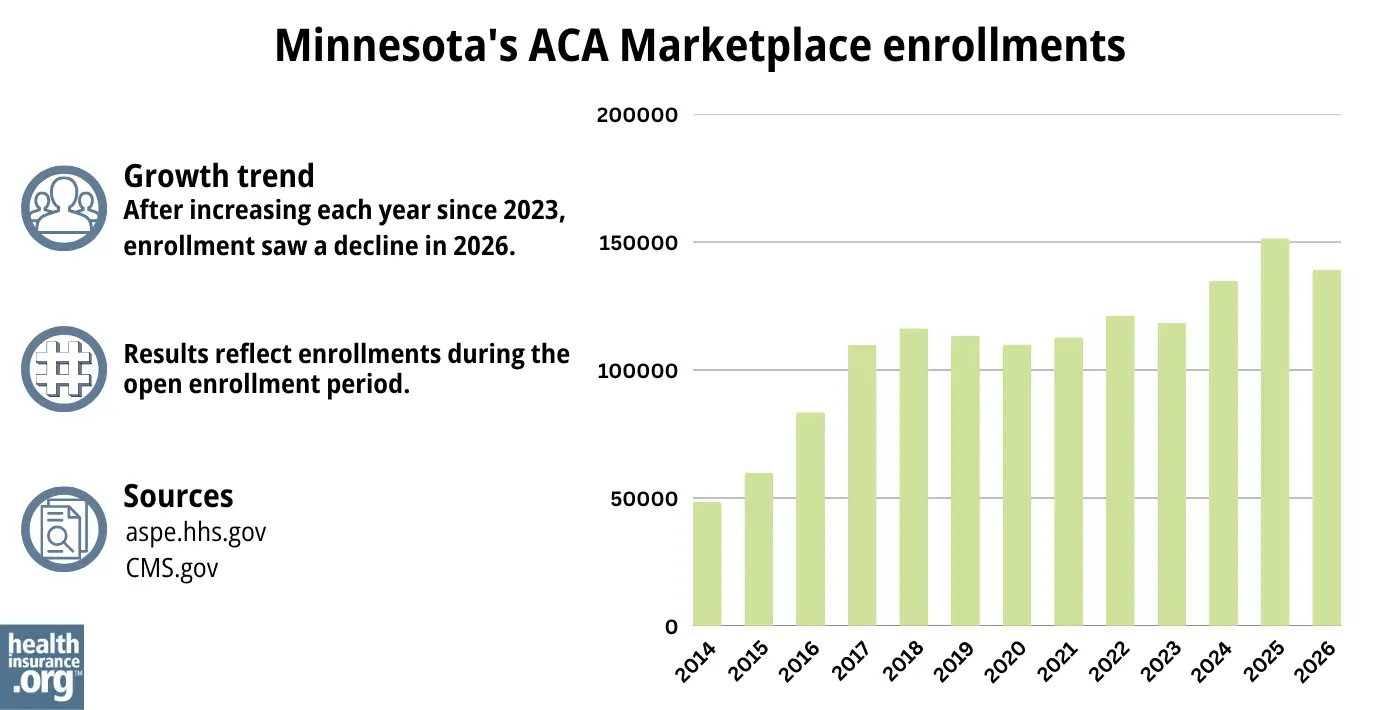

During the open enrollment period for 2026 coverage, 139,251 people enrolled in private plans through MNsure.39

This was down about 8% from the year before, when a record-high 151,512 people enrolled during the open enrollment period for 2025 coverage.40 The drop in enrollment was primarily due to the expiration of the federal subsidy enhancements at the end of 2025.

In both cases, these numbers don’t include people enrolled in MinnesotaCare and Medical Assistance.

Source: 2014,41 2015,42 2016,43 2017,44 2018,45 2019,46 2020,47 2021,48 2022,49 2023,50 2024,51 202552 202614

What health insurance resources are available to Minnesota residents?

MNsure: Minnesota’s health insurance marketplace provides financial help for individual plan premiums exclusively to state residents. To reach MNsure for more information, dial (651) 539-2099 or (855) 366-7873 if outside the Twin Cities.

Minnesota Department of Human Services: The Minnesota Department of Human Services offers health care coverage programs and resources. You can call their customer service at 651-297-3862 or 800-657-3672 for assistance.

Local tribal or county health care office: To receive assistance with health care programs, you can contact your local tribal or county health care office.

Minnesota State Health Insurance Assistance Program: You can find information and resources for Minnesota’s Medicare beneficiaries.

Medical Assistance: Minnesota’s Medical Assistance (Medicaid) program helps low-income individuals and families with medical coverage. This program has eligibility requirements, and more information is available on the Minnesota Department of Health website.

Looking for more information about other options in your state?

Need help navigating health insurance options in Minnesota?

Explore more resources for options in MN including short-term health insurance, dental, Medicaid and Medicare.

Speak to a sales agent at a licensed insurance agency.

Footnotes

- Applying for Medical Assistance (MA) and MinnesotaCare. Minnesota Department of Human Services. Accessed June 2, 2026 ⤶

- ”2026 OEP State-Level Public Use File (ZIP)” Centers for Medicare & Medicaid Services, Accessed July 9, 2026 ⤶ ⤶

- ”Individual Market Proposed Average Rate Changes for Plan Year 2026” Minnesota Commerce Department. Accessed July 15, 2025 *The above is based on the most current data available. ⤶

- Medicare and the Marketplace, Master FAQ. Centers for Medicare and Medicaid Services. Accessed June 2, 2026 ⤶

- Premium Tax Credit — The Basics. Internal Revenue Service. Accessed Apr. 2, 2026 ⤶ ⤶

- Updates to frequently asked questions about the Premium Tax Credit. Internal Revenue Service. February 2024. ⤶

- ”2027 Open Enrollment Dates Announced” MNsure. May 21, 2026 ⤶

- ”Columbus v. Kennedy; Memorandum Opinion” United States District Court for the District of Maryland. June 12, 2026 ⤶

- “Open Enrollment Period” MNsure.org, Accessed Apr. 2, 2026 ⤶

- ”Navigators” MNsure. Accessed Apr. 2, 2026 ⤶

- “2026 Marketplace Open Enrollment Period Public Use Files” CMS.gov, Accessed Apr. 2, 2026 ⤶

- “2025 Marketplace Open Enrollment Period Public Use Files” CMS.gov, Accessed Apr. 2, 2026 ⤶

- ”MNsure Board of Directors Meeting Minutes” MNsure. Jan. 28, 2026 ⤶

- ”2026 Marketplace Open Enrollment Period Public Use Files” CMS.gov. April 2026 ⤶ ⤶

- 2023 Health Insurance Rates. Minnesota Commerce Department. Accessed November 2023. ⤶

- ”Section 1332: State Innovation Waivers” Centers for Medicare & Medicaid Services. Accessed Apr. 2, 2026 ⤶

- ”Minnesota HF3388” and “Minnesota SF3936” and “Minnesota HF4106” BillTrack50. Accessed Apr. 2, 2026 ⤶

- ”Minnesota races to save reinsurance program before waiver deadline” Reinsurance Business. Mar. 6, 2026 ⤶

- ”Individual Market Final Average Rate Changes for Plan Year 2026” Minnesota Commerce Department. Accessed Nov. 13, 2025 ⤶ ⤶ ⤶

- ”Make a Plan to Enroll: MNsure Now Open for 2026 Enrollment” MNsure. Nov. 3, 2025 ⤶

- ”Individual Market Proposed Average Rate Changes for Plan Year 2027” Minnesota Commerce Department. Accessed June 16, 2026 ⤶ ⤶ ⤶ ⤶

- ”Medica Completes Acquisition of Certain UCare Contracts and Assets” Medica. Jan. 2, 2026 ⤶

- ”2027 Rate Changes – Minnesota: +11.9% indy, +15.1% sm. group (preliminary)” ACA Signups. June 17, 2026 ⤶

- “2026 Marketplace Open Enrollment Period Public Use Files” CMS.gov, Accessed June 16, 2026 ⤶

- “2026 Marketplace Open Enrollment Period Public Use Files” and “2025 Marketplace Open Enrollment Period Public Use Files” CMS.gov, Accessed Apr. 2, 2026 ⤶

- ”Compare Health Insurance Plans and Prices” (zip code 55401) MNsure. Accessed Nov. 13, 2025 ⤶

- ”With 4.5% average increase, MNsure rates to remain lowest in nation” MinnPost. Oct. 1, 2014 ⤶

- ”FINAL PROJECTION: 2016 Weighted Avg. Rate Increases: 12-13% Nationally*” ACA Signups. October 2015. ⤶

- ”Avg. UNSUBSIDIZED Indy Mkt Rate Hikes: 25% (49 States + DC)” ACA Signups. October 2016. ⤶

- ”UPDATE: Minnesota: Avg. Rate DROP In 2018 Thanks To (Troubled) Reinsurance Program” ACA Signups. Oct. 2, 2017 ⤶

- ”Minnesota: APPROVED 2019 #ACA Rates: 12.4% Lower, But Would Have Dropped 18.9% W/Out #ACASabotage” ACA Signups. Oct. 2, 2018 ⤶

- ”Minnesota: *Final* 2020 ACA Premiums: 1.0% *Decrease*” ACA Signups. Oct 1, 2019 ⤶

- ”Minnesota: APPROVED Avg. 2021 #ACA Premiums: +2.0% Indy, +2.8% Sm. Group” ACA Signups. Oct. 6, 2020 ⤶

- ”Minnesota: Approved Avg. 2022 #ACA Rate Changes: +9.5% Individual Market; +2.7% Sm. Group; Families Will Save $684/Yr On Average Thanks To The #AmRescuePlan” ACA Signups. Oct. 11, 2021 ⤶

- ”Minnesota: Final Avg. Unsubsidized 2023 #ACA Rate Changes: +1.5%” ACA Signups. Sep. 30, 2022 ⤶

- ”MN Dept of Commerce approves 2024 rates for individual and small group health insurance in Minnesota” Minnesota Commerce Department, September 2023. and “Minnesota: *Final* Avg. Unsubsidized 2024 #ACA Rate Change: +4.5%” ACA Signups. October 2023. ⤶

- ”Minnesota: *Final* avg. unsubsidized 2025 #ACA rate change: +8.8% (updated)” ACA Signups. June 18, 2024. ⤶

- ”2026 Final Gross Rate Changes – Minnesota: +22.1% avg (up from 16.9% preliminary filings)” ACA Signups. Oct. 1, 2025 ⤶

- “2026 Marketplace Open Enrollment Period Public Use Files” Centers for Medicare & Medicaid Services. Accessed Apr. 2, 2026 ⤶

- “2025 Marketplace Open Enrollment Period Public Use Files” CMS.gov, Accessed July 15, 2025 ⤶

- “ASPE Issue Brief (2014)” ASPE, 2015 ⤶

- “Health Insurance Marketplaces 2015 Open Enrollment Period: March Enrollment Report”, HHS.gov, 2015 ⤶

- “HEALTH INSURANCE MARKETPLACES 2016 OPEN ENROLLMENT PERIOD: FINAL ENROLLMENT REPORT” HHS.gov, 2016 ⤶

- “2017 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2017 ⤶

- “2018 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2018 ⤶

- “2019 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2019 ⤶

- “2020 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2020 ⤶

- “2021 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2021 ⤶

- “2022 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2022 ⤶

- “Health Insurance Marketplaces 2023 Open Enrollment Report” CMS.gov, 2023 ⤶

- ”HEALTH INSURANCE MARKETPLACES 2024 OPEN ENROLLMENT REPORT” CMS.gov, 2024 ⤶

- “2025 Marketplace Open Enrollment Period Public Use Files” CMS.gov, May 2025 ⤶