ACA-compliant coverage

What is ACA-compliant coverage?

ACA-compliant coverage refers to a major medical health insurance policy that conforms to the regulations set forth in the Affordable Care Act (ACA; also known as Obamacare).

The requirements for complying with the ACA differ depending on whether a plan is sold in the individual/small group market or the large group market, and on whether it's self-insured (meaning the employer pays claims directly) or fully insured (meaning the coverage is purchased from an insurance company by an individual or by a business).

Individual and small-group health insurance

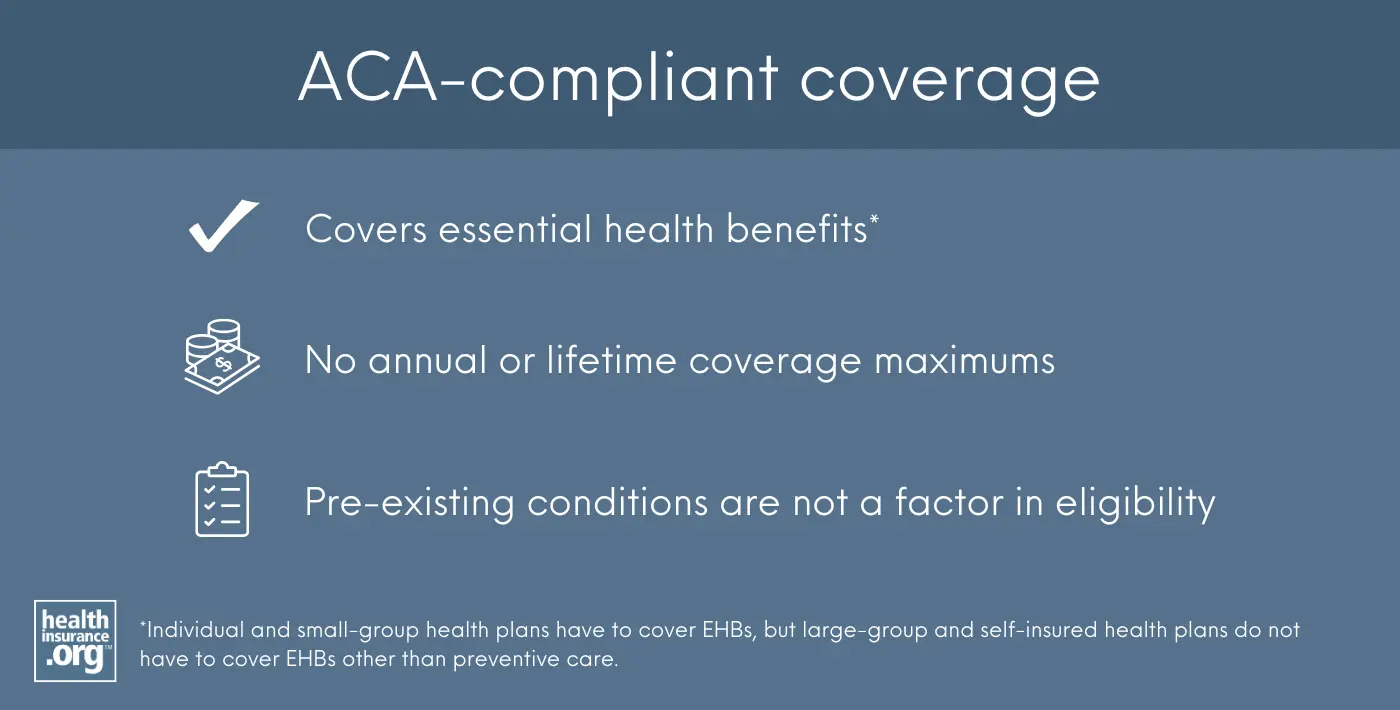

ACA-compliant individual and small-group policies must include coverage for the ten essential health benefits with no annual or lifetime coverage maximums.1 Individual and small-group coverage is guaranteed issue during open enrollment or a special enrollment period, so pre-existing conditions are not a factor in eligibility. ACA-compliant policies cannot be rescinded except in cases of fraud or intentional misrepresentation,2 and insurance companies must comply with the medical loss ratio (MLR) rules that require a carrier to spend at least 80% of premiums (85% for large-group plans) on medical expenses.

All individual and small-group health insurance policies with effective dates of January 1, 2014 or later are required to have the features listed above to be ACA-compliant, regardless of whether they are sold on or off-exchange. This has been the case since the ACA went into effect on January 1, 2014.

(Employees may still enroll in their employer’s existing small-group plans that were in effect before 2014, but if a small business purchases a new small-group plan from a health insurance company, it will be ACA-compliant, as non-ACA-compliant plans are no longer sold in the small-group market. Note that small employers are not required to offer coverage at all, and they also have the option to self-insure, in which case the ACA’s small-group rules would not be applicable.)

Large-group and self-insured health insurance

The ACA’s requirements for large-group plans and self-insured plans are different, so ACA compliance is measured in other ways for those plans. ("Large group" means 51 or more employees in most states, but 101 or more employees in California, Colorado, New York, and Vermont. However, Colorado will switch to the 51-employee threshold for large-group plans starting in 2026.)3

For example, large-group and self-insured plans don’t have to comply with the ACA’s 3:1 age-rating ratio, or 1.5:1 tobacco rating rule, as those are specific to individual and small-group plans.

And while individual and small-group health plans are required to cover the ACA’s essential health benefits, that’s not the case for large-group plans or self-insured plans of any size.4 The only EHB they're required to cover is preventive care (assuming the plan took effect after the ACA was signed into law on March 23, 2010).5

But for any other essential health benefits that a large group or self-insured plan does cover (assuming the plan took effect after the ACA was signed into law in March 2010), it cannot impose dollar limits on lifetime or annual benefits,6 and must comply with the ACA's cap on out-of-pocket costs.7

Large-group plans (and self-insured plans offered by employers with 50 or more employees) have to provide minimum value or else the employer faces a potential financial penalty.8

Fully-insured large group plans also have to comply with the ACA's MLR requirement, which means they have to spend at least 85% of premium revenue on claims and quality improvements, and no more than 15% on administrative expenses. Self-insured plans are not subject to MLR requirements.9

Grandfathered plans

Plans that were in force before 2014 have varying degrees of exemptions from the ACA’s rules. To be grandfathered, a plan must have already been in effect as of March 23, 2010, and while they are required to comply with some of the ACA’s regulations, they are exempt from many others.10

For example, grandfathered plans do not have to cover the cost of preventive care, do not have to cover pre-existing conditions, do not have to cover essential health benefits, and can still impose annual benefit limits. But they do, for example, have to allow young adults to stay on a parent’s plan until age 26, and grandfathered plans that aren't self-insured do have to comply with the ACA’s medical loss ratio rules.11

Grandfathered plans may continue to be renewed indefinitely as long as they are still offered by the carrier and the carrier does not make any substantial changes to the plan. But they are dwindling in number due to the normal turnover of insurance products.12 No individual or business has been able to purchase a new grandfathered plan since March 23, 2010, although eligible employees may still enroll in existing grandfathered plans.

Grandfathered plans count as minimum essential coverage (MEC), which broadly includes all individual market coverage and all employer-sponsored coverage.13 So if and when a grandfathered plan is terminated, the termination will trigger a special enrollment period during which a new plan can be purchased.

Grandmothered plans

Individual and small-group policies with effective dates before 2014, but after March 23, 2010, are not grandfathered. But some are still in existence, and they do not have to be fully ACA-compliant.

Originally, the ACA required these plans to terminate at their renewal date in 2014. At that point, the enrollee or business would have had an opportunity to transition to an ACA-compliant plan if they wanted to do so. But the Obama Administration announced in March 2014 that they could be renewed for another year instead, without becoming fully compliant with the ACA’s regulations.14 Ultimately, that extension has been renewed several times and these plans are now eligible to be renewed until further notice from the federal government, at the discretion of each state and carrier issuing the policy.

These plans are called “grandmothered” or “transitional” policies. They must abide by some ACA regulations, such as the ban on lifetime and annual limits for essential health benefits, but the coverage they offer can remain generally the same as it was before 2014. The majority of the states have opted to go along with the federal guidance that allows grandmothered plans to renew. But the number of people enrolled in these plans has been steadily decreasing over time, because these plans cannot be purchased by new enrollees.

Grandmothered plans also count as MEC, as they either fall under the general category of employer-sponsored insurance or individual market insurance.13

Plans that aren’t regulated by the ACA

The ACA specifically exempts some types of coverage (non-MEC) from its rules.

These plans include short-term health insurance (exempt from ACA rules specifically because it is not considered individual health insurance15), accident supplements, fixed-indemnity plans, dental/vision plans, critical illness insurance policies, travel insurance, and medical discount plans. These plans are not ACA-compliant coverage, and they continue to operate under state regulations much the way they did pre-ACA.

They also do not fulfill the shared responsibility provision (mandate requiring people to have health insurance), since they are not considered MEC. Although there’s no longer a federal penalty for not having MEC, there is a state-imposed penalty if you’re in DC, New Jersey, California, Massachusetts, or Rhode Island. Short-term health insurance is not available in any of those states, but other types of non-ACA-compliant coverage, such as fixed-indemnity plans, do tend to be available, and will not count as fulfilling a state-based individual mandate.16, 17, 18, 19, 20

It’s also important to note that some special enrollment periods for ACA-compliant individual/family coverage are only available if the applicant had minimum essential coverage for at least one of the 60 days before a qualifying life event — such as moving to a new area or getting married. That requirement cannot be fulfilled with a short-term health plan or an excepted benefit plan, since they aren’t considered minimum essential coverage.

Footnotes

- “Essential health benefits” HealthCare.gov. Accessed April 4, 2024 ⤶

- “§ 147.128 Rules regarding rescissions.” ECFR.gov. Accessed April 4, 2024 ⤶

- "Colorado SB 73" BillTrack50. Enacted May 1, 2024 ⤶

- "Federal Requirements on Private Health Insurance Plans" Congress.gov. Accessed Sep. 30, 2025 ⤶

- "Preventive Services Covered by Private Health Plans under the Affordable Care Act" KFF.org. Feb. 28, 2024 ⤶

- "FAQ about Affordable Care Act Implementation Part 66" U.S. Department of Labor. Apr. 2, 2024 ⤶

- "Maximum Annual Limitation on Cost Sharing" Congress.gov. Accessed Sep. 30, 2025 ⤶

- "Employer shared responsibility provisions" Internal Revenue Service. Accessed Sep. 30, 2025 ⤶

- "2024 Medical Loss Ratio Rebates" KFF.org. June 5, 2024 ⤶

- "Grandfathered health insurance plans" HealthCare.gov. Accessed Sep. 30, 2025 ⤶

- “Application of the New Health Reform Provisions of Part A of Title XXVII of the PHS Act to Grandfathered Plans” US Department of Labor. Accessed April 12, 2024 ⤶

- “Grandfathered Group Health Plans and Grandfathered Group Health Insurance Coverage” Federal Register. Dec. 15, 2020 ⤶

- "Minimum essential coverage" Centers for Medicare & Medicaid Services. Accessed Sep. 30, 2025 ⤶ ⤶

- “Commissioner letter” Department of Health and Human Services. Nov. 14, 2013 ⤶

- "Short-Term, Limited-Duration Insurance and Independent, Noncoordinated Excepted Benefits Coverage" (page 9). U.S. Departments of the Treasury, Labor, and Health & Human Services. April 3, 2024 ⤶

- “DC's Individual Responsibility Requirement” dchealthlink.com. Accessed April 12, 2024 ⤶

- “NJ Shared Responsibility Requirement” NJ.gov. Accessed April 12, 2024 ⤶

- “Minimum Essential Coverage for California Individual Mandate Law” CA.gov. Accessed April 12, 2024 ⤶

- “Massachusetts Individual Mandate” Massachusetts Health Connector. Accessed April 12, 2024 ⤶

- “RI Health Insurance Mandate” HealthSource RI. Accessed April 12, 2024 ⤶

Explore ACA-compliant health plans for comprehensive coverage.

Get your free quote now through licensed agency partners!