What are the deadlines for the ACA’s open enrollment period?

Learn when enrollment for 2027 ACA-compliant coverage starts and how deadlines will change

In this article

- When is the Affordable Care Act’s annual open enrollment period?

- Is the open enrollment schedule changing?

- What was the deadline to enroll in 2026 ACA-compliant health insurance coverage in the individual market?

- Outside of ACA’s open enrollment window, enrollment is only available with a special enrollment period

When is the Affordable Care Act’s annual open enrollment period?

The annual ACA open enrollment window for 2026 coverage ended in early 2026. The open enrollment period followed the same schedule that had been used for the last few years, with most states running open enrollment from November 1 through January 15.

Here’s everything we know right now about ACA open enrollment deadlines going forward:

Is the ACA open enrollment schedule changing?

In 2025, the U.S. Department of Health & Human Services (HHS) finalized a rule change implementing a shorter ACA open enrollment period starting in the fall of 2026.1 The rule clarified that open enrollment would end on December 15 in states that use HealthCare.gov, and that it could not extend past December 31 in states that run their own Marketplaces. The rule also required that all ACA plans selected during open enrollment would take effect on January 1, as there would no longer be an option for a February 1 start date unless an applicant was eligible for a special enrollment period.

However, the rule change requiring a shorter open enrollment period was vacated by a judge in June 2026.2

What it means: It’s possible the open enrollment schedule won’t be shortened, and will instead continue to have a January 15 deadline in most states. But HHS could appeal the ruling, so the case could continue. We will update this page as more information becomes available, so check back in the coming weeks.

We have been tracking open enrollment schedule announcements from state-run Marketplaces, and have detailed them below. We will continue to update this list if there are any developments related to the June 2026 court ruling.

In all states except Idaho, Pennsylvania, and Massachusetts, open enrollment for 2027 coverage will begin on November 1, 2026. (In Idaho and Pennsylvania, it will begin on October 15,3 and in Massachusetts, it will begin on October 23.4)

The dates for the end of open enrollment will depend on whether the June 2026 court ruling is appealed (and if so, the outcome of the appeal), and whether a state runs its own Marketplace platform or uses HealthCare.gov.

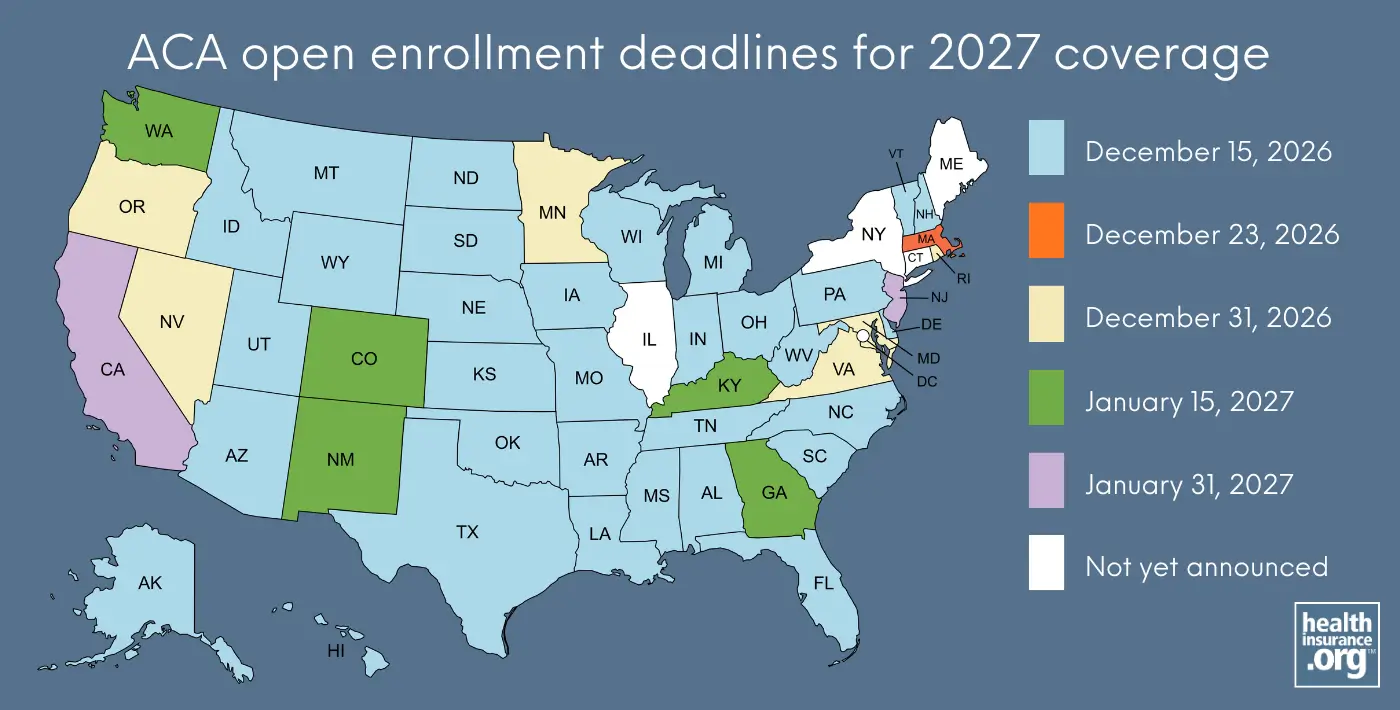

Here are the enrollment deadlines that have been announced by state-run Marketplaces as of mid July 2026, although as noted above, this could change in response to the vacatur of the federal rule change. States that have newly published their deadlines or extended their previously announced enrollment deadlines following the June 2026 court ruling are in bold font:

- California: January 315

- Colorado: January 156

- Georgia: January 157

- Kentucky: January 158

- Maryland: December 319

- Massachusetts: December 2310

- Minnesota: December 3111

- Nevada: December 3112

- New Mexico: January 1513

- New Jersey: January 3114

- Oregon: December 3115

- Pennsylvania: December 1516

- Rhode Island: December 3117

- Vermont: December 1518

- Virginia: December 3119

- Washington: January 1520

Connecticut's exchange clarified (before the vacatur was announced) that open enrollment “will end by December 31, 2026,” but notes that the exchange reserves the right to change this.21

We’ll continue to update this page as we get closer to open enrollment and state-run exchanges provide clarification on the deadlines that they’ll be using for 2027 coverage.

What was the deadline to enroll in 2026 ACA-compliant health insurance coverage in the individual market?

In most states, open enrollment for individual/family health coverage for 2026 ended on January 15, 2026, although it ended in December 2025 in Idaho, and there are several states where it continued until January 31, 2026. Washington, D.C. had the latest enrollment deadline of February 4, which was a last-minute extension.22

Outside of ACA’s open enrollment window, enrollment is only available with a special enrollment period

After open enrollment ends, people can normally only purchase coverage if they have a special enrollment period (SEP) triggered by a qualifying life event. You can learn more about special enrollment periods in our Special Enrollment Guide.

Read: Who doesn’t need a qualifying life event to enroll in health insurance outside of open enrollment?

Footnotes

- “Patient Protection and Affordable Care Act; Marketplace Integrity and Affordability” Federal Register, U.S. Department of Health & Human Services. June 25, 2025 ⤶

- “Columbus v. Kennedy; Memorandum Opinion” U.S. District Court for the District of Maryland. June 12, 2026 ⤶

- “How to Enroll” Your Health Idaho. Accessed July 13, 2026. And “Pennsylvanians dropping health coverage through Pennie citing higher plan costs as the number one reason” Pennie. June 9, 2026 ⤶

- “When is Open Enrollment and when do Health Connector plans start?” Massachusetts Health Connector. Accessed Apr. 22, 2026 ⤶

- "Dates and Deadlines" Covered California. Accessed July 13, 2026; Archived version of Federal Changes to Your Health Insurance (as of April 2026) showed a December 31 deadline, but that change has been removed from the version of the page that was live as of July 2026 ⤶

- Colorado is reverting to the normal January 15 end date, per email communication sent by Connect for Health Colorado on July 13, 2026 ⤶

- "Georgia Access Plan Year (PY) 2027 Qualified Health Plan (QHP) Application Instructions for Issuers” Georgia Access. Updated June 30, 2026; previous version, dated Mar. 30, 2026, is no longer live but it showed an open enrollment window running from Oct. 19 to Dec. 15 ⤶

- “Open Enrollment has ended!” Kentucky Health Benefit Exchange. Accessed July 2, 2026. Archived version of the page from May 11, 2026 showed that open enrollment was scheduled to end on December 31 at that point, but the deadline was changed to January 15 after the court ruling. ⤶

- “Maryland Health Benefit Exchange, Board of Trustees Meeting Minutes” Maryland Health Benefits Exchange. Apr. 20, 2026 ⤶

- "Stay Informed About Federal Changes" Massachusetts Health Connector. June 10, 2026 ⤶

- “2027 Open Enrollment Dates Announced” MNsure. May 21, 2026 ⤶

- “When can I enroll?” Nevada Health Link. Accessed June 16, 2026 ⤶

- "Need Insurance? A Guide to Understanding Your Enrollment Options" BeWellnm. Accessed July 13, 2026; archived version (as of May 2026) showed an end date of December 31 ⤶

- "NJ Department of Banking and Insurance Announces Grant Opportunity for Community Organizations to Help New Jerseyans Enroll in Health Coverage" New Jersey Department of Banking and Insurance. July 9, 2026 ⤶

- “April board meeting” (starting at the 51-minute mark). Oregon Health Insurance Marketplace. Apr. 16, 2026 (this deadline was still being noted as of the June 26, 2026 Oregon Marketplace board meeting) ⤶

- “Pennsylvanians dropping health coverage through Pennie citing higher plan costs as the number one reason” Pennie. June 9, 2026 ⤶

- “Open Enrollment operated differently this year. Stay connected to us… and stay covered.” Health Source RI. Accessed June 16, 2026 ⤶

- “Health Insurance Changes: Stay informed!” Vermont Health Connect. Accessed June 16, 2026 ⤶

- “How to enroll” Virginia's Health Insurance Marketplace. Accessed June 16, 2026 ⤶

- “Enrollment Periods” Washington Healthplanfinder. Accessed July 2, 2026. Archived version of the page from June 1, 2026 showed that open enrollment was scheduled to end on December 31 at that point, but the deadline was changed to January 15 after the court ruling. ⤶

- “Plan Year 2027 Qualified Health Plan Solicitation for Participation in the Individual and/or Small Business Health Options Program (Small Group) Marketplaces” Access Health CT. April 20, 2026 ⤶

- “DC Health Link Enrollment Deadline Extended” HillRag. Feb. 2, 2026 ⤶