cost sharing

What is cost-sharing?

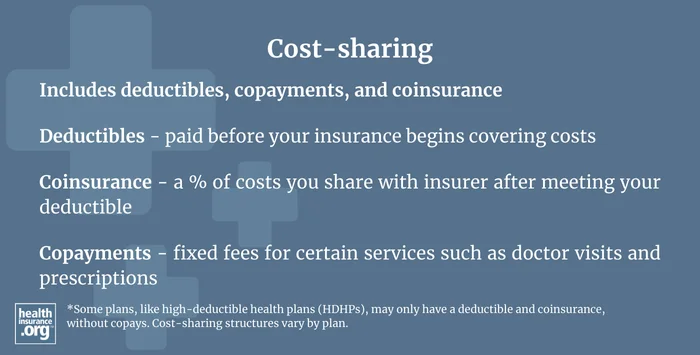

Cost-sharing refers to the patient’s portion of costs for healthcare services covered by their health insurance plan. The patient is responsible for paying cost-sharing amounts out-of-pocket.

Cost-sharing can be in the form of a deductible, copayment, or coinsurance; most plans incorporate all of these types of cost-sharing, with the specifics depending on the service that's provided and whether or not the patient has met their deductible (coinsurance generally applies after you've met the deductible, whereas you'll be paying towards your deductible before that point; copays generally apply to other services, such as office visits or prescription drugs, if they aren't counted towards the deductible).

Some health plans, like HDHPs, don't have copays and instead just have a deductible or a deductible plus coinsurance (as of 2026, all Bronze and Catastrophic Marketplace plans are considered HDHPs, even if they have copays). The specifics will vary from one plan to another.

Are premiums part of cost-sharing?

Cost-sharing comes into play when a policyholder receives medical care and a claim is submitted to their insurance plan. Health insurance premiums – the monthly payments you must make to keep your coverage in force, regardless of whether or not you use a healthcare service – are not considered cost-sharing amounts. Premiums are not counted as part of your out-of-pocket exposure under Medicare or a commercial plan obtained through an employer or in the individual/family market.

However, premiums are counted as part of the allowable out-of-pocket costs under Medicaid and the Children's Health Insurance Program (CHIP), which are capped at 5% of enrollees' household income.1 So for Medicaid and CHIP, premiums and cost-sharing are both counted as out-of-pocket costs. But under private health insurance or Medicare, "out-of-pocket costs" generally only refer to cost-sharing incurred when a person has medical claims (even though premiums are also paid out-of-pocket).

Is there a cap on the total amount of cost-sharing I'm required to pay?

Under the Affordable Care Act, most health plans must have an out-of-pocket maximum (referred to as maximum OOP, or MOOP) of no more than $10,600 in cost-sharing for a single individual in 2026 (this limit is indexed each year; for 2027, it will be $12,000, although it's possible some plans could have even higher out-of-pocket limits).2

Many plans have out-of-pocket limits below the allowable maximum, but they cannot be higher. Once your cost-sharing amounts have reached your plan's maximum out-of-pocket limit for the year, the health insurance plan will pay 100% of your remaining covered costs that year.

The ACA's limits on out-of-pocket costs only apply to in-network services that fall within the umbrella of essential health benefits. And it does not apply to grandmothered or grandfathered plans, or to plans that aren't regulated by the ACA at all, such as short-term health insurance.

Original Medicare does not have a cap on cost-sharing amounts, although most enrollees have supplemental coverage (from an employer, Medicaid, or a Medigap plan) that covers some or all of their cost-sharing expenses.

Medicare Advantage plans cannot require members to pay in-network cost-sharing over $9,250 in 2026,3 although most plans have cost-sharing limits below this, with a median of about $5,400 in 2025.4 (Note that the out-of-pocket limits for Medicare Advantage plans do not include the cost of prescription drugs. Prescriptions are covered by most Medicare Advantage plans but with separate cost-sharing, capped at $2,100 in 2026).

Where can I find information on what cost-sharing my plan requires?

Your health insurance ID card may provide some or all of this information. It's common for ID cards to list the plan's copay and deductible amounts, and the coinsurance percentage, but the exact dollar amount of the coinsurance charge will depend on the amount of the claim, since it's a percentage rather than a flat dollar amount.

You can also find comprehensive information in your certificate of insurance, certificate of coverage, or summary plan description (SPD). These are all names used for a document published by your health plan that explains the terms and conditions of your health insurance policy. The certificate of insurance will list the amount of your individual and/or family deductible as well as copayments or coinsurance amounts you will be required to pay for covered services.

Footnotes

- "Understanding the Impact of Medicaid Premiums & Cost-Sharing: Updated Evidence from the Literature and Section 1115 Waivers" KFF.org. Sep. 9, 2021 ⤶

- "Patient Protection and Affordable Care Act, HHS Notice of Benefit and Payment Parameters for 2027; and Basic Health Program" Centers for Medicare & Medicaid Services. Feb. 11, 2026 ⤶

- "What You'll Pay in Out-of-Pocket Medicare Costs in 2026" National Council on Aging. Nov. 24, 2025 ⤶

- "Analysis of the 2025 Medicare Advantage Plan Landscape" Better Medicare Alliance. Accessed Nov. 13, 2024 ⤶