grandfathered health plan

What is a grandfathered health plan?

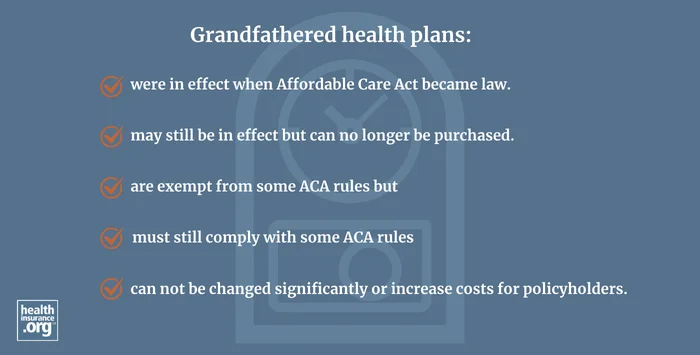

Grandfathered plans are health insurance plans that were already in effect as of March 23, 2010, when the Affordable Care Act was signed into law. In the individual market, they are plans that already covered the policyholder as of that date, and in the employer-sponsored market, they are plans that the employer had already implemented as of that date, and has continuously offered ever since, with at least one covered employee at all times.1

Employees can join an employer's existing grandfathered plan, but grandfathered plans have not been available for purchase (in the individual market, or by an employer) since the ACA was signed into law.

Most people with grandfathered coverage have employer-sponsored coverage. As of 2020, less than 7% of grandfathered plan enrollees were in the individual market.2

Also as of 2020 (the latest available data),3 about 14% of workers with employer-sponsored health plans were enrolled in grandfathered plans.4

What ACA rules apply to grandfathered plans?

Grandfathered plans don't have to comply with several significant ACA provisions.5 They do not have to cover preventive care with no cost-sharing, and they do not have to cap out-of-pocket costs. Grandfathered plans cannot, however, impose lifetime benefit limits on any essential health benefits that they cover (they aren't required to cover essential health benefits though), must allow insureds to keep their children on the plan until age 26, and must abide by the ACA's medical loss ratio rules (unless they're self-insured, as MLR rules don't apply to self-insured plans).

Are grandfathered plans required to remain in force?

Grandfathered plans are allowed to remain in force indefinitely — neither the state nor the federal government can force them to end. But they are not required to remain in force. Insurers can decide to terminate grandfathered plans, and some have done so over the years. Examples include Humana,6 Anthem Blue Cross in California,7 and Blue Cross Blue Shield of North Carolina.8

As time goes by and the pool of people on grandfathered plans shrinks and ages, insurers may be less likely to keep those plans in force. This is particularly true in the individual market, since no new members can join those plans unless they're a new dependent being added to a family's existing plan. But in the employer-sponsored market, new employees can join an existing grandfathered plan. This helps to prevent the overall membership pool from becoming older and less healthy over time.

The ACA specifically allows for the indefinite continuation of grandfathered plans, which is what President Obama was talking about when he said people would be able to keep their pre-ACA plans if they wanted to. But that doesn't mean that insurers are required to keep those policies in force. It's also important to understand that grandfathered plans are not the same as grandmothered plans.

How have the rules for grandfathered plans changed over time?

To retain grandfathered status, a plan cannot have been substantially changed since the ACA was enacted, and there are limits on how much cost-sharing can increase and how benefits can change.1

Employer-sponsored grandfathered plans were initially only allowed to keep their grandfathered status if they didn't switch to a new plan (or switch to a new third-party administrator, if the plan was self-insured). But updated rules allow grandfathered employer-sponsored plans to continue to be grandfathered even if they switch to a new insurer or administrator, as long as the coverage itself doesn't change in a way that would cause the plan to lose its grandfathered status.9

In February 2019, the Departments of the Treasury, Labor, and Health & Human Services published a request for comments on whether there should be rule changes to make it easier for employer-sponsored grandfathered plans to retain their grandfathered status going forward. (The request for comments did not pertain to individual market grandfathered health plans, and the subsequent rule changes do not either.)

So it was not surprising when the Trump administration published a proposed rule in July 2020 that included two modifications that would make it easier for employer-sponsored grandfathered plans to make changes to their coverage and still retain their grandfathered status. The administration accepted public comments on the proposed rule changes through mid-August, but received just 13 comments. The proposed rule was finalized in December 2020 with very few modifications, although the effective date was pushed out to June 15, 2021:

- The first modification allows HSA-qualified grandfathered group plans to increase cost-sharing as necessary to comply with IRS requirements for HDHPs:

- The IRS sets the rules for HDHPs, and they are indexed annually. There has never been a year when the IRS-mandated increase in minimum deductibles for HDHPs exceeded the allowable cost-sharing increases for grandfathered plans, but the new rule change will ensure that grandfathered employer-sponsored HDHPs can continue to be HSA-qualified even if that situation were to arise.

- The plans have explicit permission to raise deductibles as necessary to conform to IRS rules (so that enrollees could continue to contribute to their HSAs) and still retain their grandfathered status, even if the necessary deductible increase were to exceed the normal requirements for grandfathered plans.

- The second modification allows employer-sponsored grandfathered plans to potentially increase cost-sharing (copays, deductibles, out-of-pocket maximum) more than was previously allowed, without losing their grandfathered status:

- The previous rules allowed grandfathered plans to increase cost-sharing by an amount equal to medical inflation since March 2010 plus up to 15 percentage points.

- The updated rule allows employer-sponsored grandfathered plans the option to base cost-sharing increases on how much the premium adjustment percentage increases each year, plus 15 percentage points.

- The premium adjustment percentage is updated by HHS each year, and they changed the formula in 2020 to incorporate the change in individual market premiums. This resulted in a premium adjustment percentage that was larger than it would otherwise have been. Under the newly finalized rule, cost-sharing amounts on grandfathered group plans were expected to potentially be about 3 percentage points higher by 2026 than they would otherwise have been.

- The Biden administration subsequently reversed the 2020 rule change for the premium adjustment percentage, resetting it to the way it had been before 2020. But the second Trump administration reversed this again in 2025, for coverage effective in 2026. Under the second Trump administration's rule change, the indexing formula once again includes individual market premiums, resulting in a larger allowable percentage increase.

The rule changes do not apply to grandfathered plans in the individual/family market, but the vast majority of grandfathered plans are in the group market, where the rule changes do apply.

Footnotes

- "Grandfathered plans" Centers for Medicarei & Medicaid Services. Accessed Oct. 27, 2025 ⤶ ⤶

- "Final Rule on Grandfathered Health Plans Will Allow Higher Consumer Costs" Health Affairs. Dec. 14, 2020 ⤶

- "Internal Revenue Bulletin: 2024-47" Internal Revenue Service. Nov. 18, 2024 ⤶

- "Employer Health Benefits, 2020 Annual Survey" KFF.org. Accessed Oct. 27, 2025 ⤶

- "Grandfathered health insurance plans" HealthCare.gov. Accessed Oct. 27, 2025 ⤶

- "Humana Cuts Grandfathered Plans" Insurance News Net. Jan. 13, 2016 ⤶

- "Anthem Blue Cross termination notice" effective Dec. 31, 2022 ⤶

- "What happened to grandfathered health insurance?" Affordable Healthcare Coalition of North Carolina. Oct. 27, 2017 ⤶

- "Amendment to Regulation on “Grandfathered” Health Plans under the Affordable Care Act" CMS.gov. Accessed Aug. 13, 2024 ⤶