Find Louisiana Health Insurance Marketplace Coverage for 2026

Compare ACA plans and check subsidy savings from a licensed third-party health insurance agency.

Louisiana Health Insurance Marketplace Guide

This guide, including the FAQs below, was created to help make it easier to choose the right health insurance for yourself and your family. A plan from the Affordable Care Act (ACA) Marketplace may be a good choice for many people.

Louisiana uses the federal health insurance exchange to help people sign up for ACA plans. The exchange is also known as the ACA Marketplace or Obamacare Marketplace.

The federal government runs the Louisiana Marketplace website, HealthCare.gov, which lets you shop for health plans offered by five private insurance companies1 (this includes two separate Blues affiliates; see details below regarding insurer participation and premium changes for 2026). Plan availability varies from one part of the state to another.

If you buy a plan from the Marketplace, the government may help pay your premiums through an income-based advance premium tax credit (APTC). See details below about how premium tax credits changed for 2026.

*Values displayed by this tool are from data generated by CMS and reflect 2026 Marketplace health plans purchased in each state. The values returned are averages based on the plans purchased by consumers of each selected state: subsidy and premium values vary based on factors such as zip code, age, household size, and income.

Louisiana Marketplace quick facts

Frequently asked questions about health insurance in Louisiana

Who can buy Marketplace health insurance in Louisiana?

If these apply to you, you can buy individual and family health insurance from Louisiana’s Marketplace:

- You live in Louisiana.

- You are lawfully present in the U.S.

- You’re not enrolled in Medicare.

- You’re not incarcerated.

Many people, like early retirees not yet on Medicare, self-employed people, and those who work for small businesses without health benefits, buy health insurance on the Marketplace.

Eligibility for financial assistance, such as premium subsidies and cost-sharing reductions, is based on your income and how it compares with the cost of the second-lowest-cost Silver plan in your area (which depends on your age and location). In addition, you may qualify for financial assistance in the Marketplace if:

- You don’t have access to affordable health coverage through your employer. If your employer offers coverage, but you feel it’s too expensive, our Employer Health Plan Affordability Calculator can help you understand if you might qualify for premium subsidies.

- You’re not eligible for Medicaid/CHIP.

- You’re not eligible for premium-free Medicare Part A.4

- You file a joint tax return with your spouse, if you’re married.5

- You can’t be claimed by someone else as a tax dependent.5

When can I enroll in an ACA-compliant plan in Louisiana?

In Louisiana, the open enrollment period for ACA-compliant individual and family health plans ended on January 15, 2026.6

To enroll in 2026 coverage for the remainder of the year, or to switch to a different plan, you’ll need a special enrollment period (SEP). To qualify for a SEP, you’ll generally need a qualifying life event, although Native Americans can enroll year-round without a qualifying life event.

Starting in the fall of 2026, the open enrollment period will be shorter. In Louisiana (and all other states that use the HealthCare.gov Marketplace platform), the open enrollment period will run from November 1 to December 15, 2026. All plans selected during open enrollment will take effect on January 1.

How do I enroll in a Marketplace plan in Louisiana?

You can enroll in a Louisiana health insurance Marketplace plan:

- Directly through HealthCare.gov, the ACA exchange website

- By phone at (800) 318-2596 (TTY: 1-855-889-4325). Talk to an agent 24 hours a day, seven days a week, except for holidays.

- With the help of agents, navigators, or certified application counselors (available over the phone or online; some offer in-person meetings as well).

- Via an approved enhanced direct enrollment entity.7

How can I find affordable health insurance in Louisiana?

In Louisiana, people who don’t have access to Medicare, Medicaid, or an employer-sponsored plan can find affordable coverage on the ACA Marketplace (HealthCare.gov).

Most Louisiana Marketplace enrollees qualify for income-based premium subsidies called Advance Premium Tax Credits (APTC). These subsidies are still available in 2026, but they don’t cover as much of enrollees’ total premiums as they did in 2025, and they’re no longer available to anyone whose household income is more than 400% of the federal poverty level.

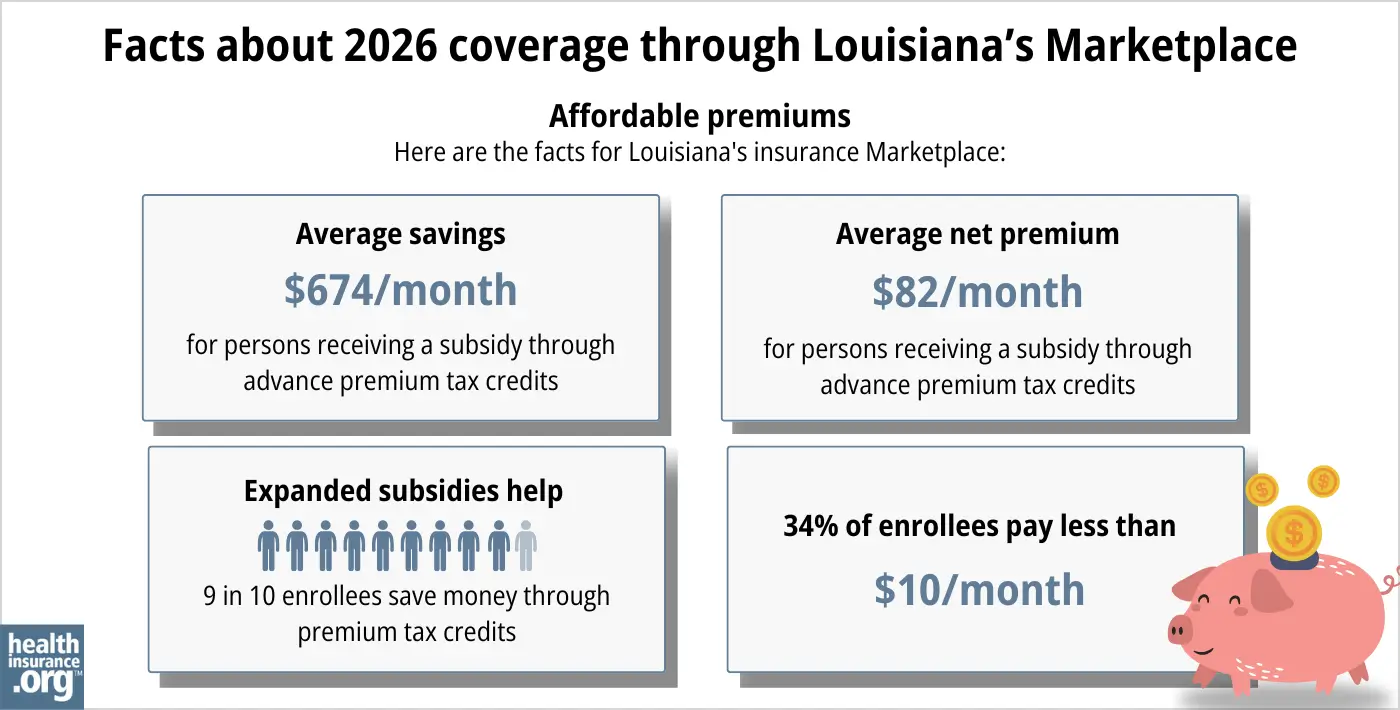

During the open enrollment period for 2026 coverage, 91% of Marketplace enrollees in Louisiana qualified for APTC. The average subsidy amounted to $674/month, reducing the average net premium to about $582/month for subsidy-eligible enrollees.8

Source: CMS.gov8

In addition to APTC, you may qualify for cost-sharing reductions (CSR), which help you pay for your deductibles and out-of-pocket expenses.9 CSR benefits are only available on Silver-level plans, and your income must be no more than 250% of the federal poverty level to be eligible for CSR. For 2026 coverage, that amounts to $39,125 for a single individual, and $80,375 for a family of four.10

Another way to find affordable health insurance in Louisiana is through the state’s Medicaid program. Louisiana has expanded Medicaid under the ACA, so adults under age 65 are eligible for Medicaid with a household income up to 138% of the poverty level.

Short-term plans may be a low-cost alternative for those who are not eligible for employer coverage, Medicare, Medicaid, or Marketplace subsidies. However, short-term plans are not subject to ACA regulations, so they generally offer less robust benefits and fewer consumer protections.

How many insurers offer Marketplace coverage in Louisiana?

Five private insurance companies are offering coverage through Louisiana’s health insurance Marketplace for 2026:11

- Ambetter from Louisiana Healthcare Connections

- HMO Louisiana (Louisiana Blue)

- Blue Cross Blue Shield of LA (LA Health Service and Indemnity Company)

- UnitedHealthcare

- CHRISTUS Health Plan Louisiana

As is the case in most states, plan availability varies throughout the state, as each insurer sets its own coverage area.

Are Marketplace health insurance premiums increasing in Louisiana?

The following average premium increases were approved for Louisiana’s Marketplace insurers for 2026.12 The overall average rate change amounted to an increase of 23.7% for 2026, before subsidies were applied13 (net premiums increased much more significantly, as described below).

Louisiana’s ACA Marketplace Plan 2026 APPROVED Rate Changes by Insurance Company |

|

|---|---|

| Issuer | Percent Increase |

| Ambetter from Louisiana Healthcare Connections | 23.1% |

| Louisiana Health Service & Indemnity Company (Blue Cross Blue Shield of Louisiana) | 32.5% |

| CHRISTUS Health Plan Louisiana | 14% |

| HMO Louisiana (Louisiana Blue, a BCBSLA subsidiary) | 12.2% |

| UnitedHealthcare | 23% |

Source: Louisiana Department of Insurance12

Rate changes are calculated based on full-price premiums, before any premium subsidies are applied. However, because most people using Louisiana’s exchange receive premium tax credits, they don’t pay the full cost of their coverage.14

If you qualify for these subsidies, your actual rate change depends on your plan’s cost and the subsidy amount you receive. It’s important to understand that because Congress didn’t extend the federal subsidy enhancements that had been in place since 2021, subsidies don’t cover as much of enrollees’ premium in 2026, and are available to fewer people. This caused net premiums to increase by much more than the percentage increases that applied to full-price plans.

For perspective, here’s a summary of how average full-price premiums have changed over time for individual/family health insurance in Louisiana:

- 2015: Average increase of 12%15

- 2016: Average preliminary increase of 15.4%16

- 2017: Average increase of 26.8%17

- 2018: Average increase of 21.4%18

- 2019: Average decrease of 6.4%19

- 2020: Average increase of 11.7%20

- 2021: Average increase of 6.9%21

- 2022: Average increase of 4.8%22

- 2023: Average increase of 2.5%23

- 2024: Average increase of 1.3%24

- 2025: Average decrease of 7.9%25

How many people are insured through Louisiana’s Marketplace?

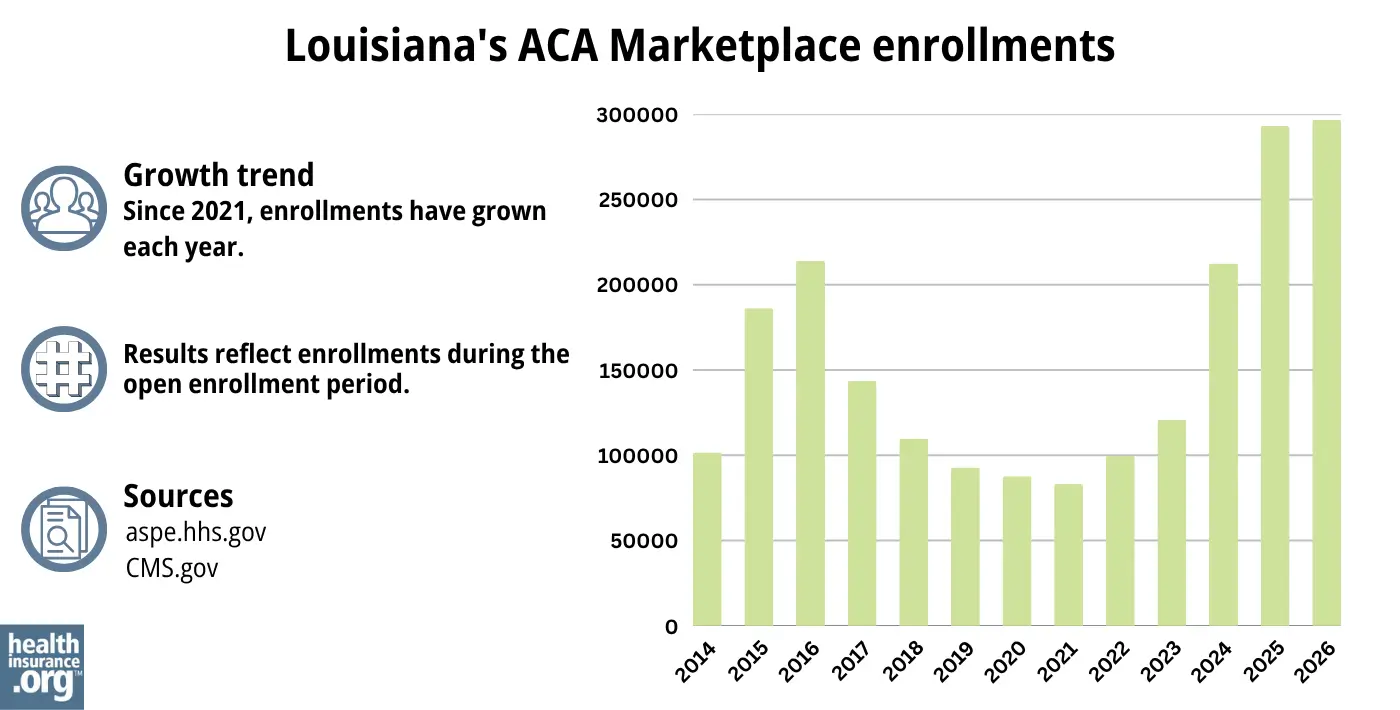

During the open enrollment period for 2026 coverage, 296,648 people enrolled in private health plans through the Marketplace in Louisiana.8 Unlike most states, this was an increase from the year before, when 292,994 people enrolled through the Marketplace in Louisiana.26 (Nationwide, enrollment dropped by about 5%)27

Both the 2026 and 2025 enrollment numbers were much higher than enrollment had been in recent years, and new record high enrollments were set in Louisiana in both 2025 and 2026 (see chart below). Prior to 2025, the record high had been in 2016, just before Medicaid expansion took effect in Louisiana. (Medicaid expansion generally results in a decrease in Marketplace enrollment, as people with income between 100% and 138% of the poverty level transition from being eligible for Marketplace subsidies to being eligible for Medicaid.)

Source: 2014,28 2015,29 2016,30 2017,31 2018,32 2019,33 2020,34 2021,35 2022,36 2023,37 2024,38 202526 20268

The enrollment growth in recent years is due in part to the subsidy enhancements created by the American Rescue Plan and the Inflation Reduction Act. Those subsidy enhancements expired at the end of 2025, however, making Marketplace plans much less affordable in 2026.

And the enrollment growth for 2024 and 2025 was also partially due to the “unwinding” of the pandemic-era Medicaid continuous coverage rule. Louisiana Medicaid began to disenroll people from the program in mid-2023. CMS reported that more than 112,000 Louisiana residents transitioned from Medicaid to Marketplace coverage during the unwinding process.39

What health insurance resources are available to Louisiana residents?

HealthCare.gov

The official website where residents of Louisiana can shop for and buy health insurance plans that meet their needs.

Department of Health & Hospitals

This is a governmental body responsible for health services and programs in Louisiana.

Louisiana Department of Insurance

The Louisiana Department of Insurance provides various resources related to health insurance, helping people understand their options and make informed choices.

Medicare Rights Center

A national organization that offers assistance and information about Medicare through its website and call center.

Louisiana Senior Health Insurance Information Program (SHIP)

Assists people on Medicare, providing information and guidance about their health insurance options.

Louisiana Department of Health – Medicaid

Oversees the state’s Medicaid program, which provides health coverage for eligible low-income individuals and families.

Looking for more information about other options in your state?

Need help navigating health insurance options in Louisiana?

Explore more resources for options in LA including short-term health insurance, dental, Medicaid and Medicare.

Speak to a sales agent at a licensed insurance agency.

Footnotes

- ”Louisiana Rate Review Submissions” RateReview.HealthCare.gov. And “Health Rate Filing Search for Individual and Small Group Markets” Louisiana Department of Insurance. Accessed Sep. 21, 2025 ⤶

- ”2026 OEP State-Level Public Use File (ZIP)” Centers for Medicare & Medicaid Services, Accessed July 9, 2026 ⤶ ⤶

- ”Louisiana Rate Review Submissions” RateReview.HealthCare.gov. And “Health Rate Filing Search for Individual and Small Group Markets” Louisiana Department of Insurance. Accessed Sep. 21, 2025 *The above is based on the most current data available. ⤶

- Medicare and the Marketplace, Master FAQ. Centers for Medicare and Medicaid Services. Accessed Mar. 4, 2026 ⤶

- Premium Tax Credit — The Basics. Internal Revenue Service. Accessed Mar. 4, 2026 ⤶ ⤶

- “When can you get health insurance?” HealthCare.gov, 2023 ⤶

- “Entities Approved to Use Enhanced Direct Enrollment” CMS.gov, Dec. 8, 2025 ⤶

- ”2026 Marketplace Open Enrollment Period Public Use Files” CMS.gov. April 2026 ⤶ ⤶ ⤶ ⤶

- Saving money on health insurance; Cost-sharing reductions. HealthCare.gov. Accessed November 2023. ⤶

- “Federal Poverty Level (FPL)” HealthCare.gov. Accessed Sep. 21, 2025 ⤶

- ”Louisiana Rate Review Submissions” RateReview.HealthCare.gov. And “Health Rate Filing Search for Individual and Small Group Markets” Louisiana Department of Insurance. Accessed Sep. 21, 2025

⤶ - ”Health Rate Filing Search for Individual and Small Group Markets” Louisiana Department of Insurance. Accessed Sep. 21, 2025 ⤶ ⤶

- ”2026 FINAL Gross Rate Changes – Louisiana: +23.7% (updated – slight drop from requested)” ACA Signups. Aug. 29, 2025 ⤶

- ”Effectuated Enrollment: Early 2025 Snapshot and Full Year 2024 Average” CMS.gov, July 24, 2025 ⤶

- Analysis Finds No Nationwide Increase in Health Insurance Marketplace Premiums. The Commonwealth Fund. December 2014. ⤶

- Louisiana: *Requested* 2016 Weighted Avg. Rate Hikes: 15.4%. ACA Signups. September 2015. ⤶

- Avg. UNSUBSIDIZED Indy Mkt Rate Hikes: 25% (49 States + DC). ACA Signups. October 2016. Approved as filed: Health Rate Filing Search for Individual and Small Group Markets. Louisiana Department of Insurance. Accessed November 2023. ⤶

- Louisiana: APPROVED Rate Hikes: 7.2% If CSRs *Are* Paid, 21.4% If They *Aren’t*. ACA Signups. September 2017. ⤶

- Obamacare premiums to drop in Louisiana in 2019 after years of rate hikes. The Advocate. August 2018. ⤶

- Louisiana: *Final* Avg. 2020 ACA Premiums: 11.7% Increase. ACA Signups. October 2019. ⤶

- Louisiana: Preliminary Avg. 2021 ACA Premiums: +6.9% Indy, +5.2% Sm. Group (Unweighted). ACA Signups. October 2020. ⤶

- Louisiana: 2022 ACA Premiums: +4.8% Indy, +6.9% Sm. Group. ACA Signups. September 2021. ⤶

- Louisiana: Final Avg. Unsubsidized 2023 #ACA Rate Changes: +2.5% (Unweighted). ACA Signups. November 2022. ⤶

- Open Enrollment for Health Insurance Coverage Underway. Louisiana Department of Insurance. November 15, 2023. ⤶

- ”Open Enrollment for Health Insurance Coverage Runs Through January 15” Louisiana Department of Insurance. Nov. 6, 2024 ⤶

- “2025 Marketplace Open Enrollment Period Public Use Files” CMS.gov, May 2025 ⤶ ⤶

- ”Breaking: CMS posts semifinal 2026 Open Enrollment report: 23.0M QHPs, down “only” 1.3M…” ACA Signups. Jan. 28, 2026 ⤶

- “ASPE Issue Brief (2014)” ASPE, 2015 ⤶

- “Health Insurance Marketplaces 2015 Open Enrollment Period: March Enrollment Report”, HHS.gov, 2015 ⤶

- “HEALTH INSURANCE MARKETPLACES 2016 OPEN ENROLLMENT PERIOD: FINAL ENROLLMENT REPORT” HHS.gov, 2016 ⤶

- “2017 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2017 ⤶

- “2018 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2018 ⤶

- “2019 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2019 ⤶

- “2020 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2020 ⤶

- “2021 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2021 ⤶

- “2022 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2022 ⤶

- “Health Insurance Marketplaces 2023 Open Enrollment Report” CMS.gov, 2023 ⤶

- ”HEALTH INSURANCE MARKETPLACES 2024 OPEN ENROLLMENT REPORT” CMS.gov, 2024 ⤶

- HealthCare.gov Marketplace Medicaid Unwinding Report. Centers for Medicare and Medicaid Services. Data through April 2024; Accessed Aug. 6, 2024 ⤶