Find Iowa Health Insurance Marketplace Coverage for 2026

Compare ACA plans and check subsidy savings from a licensed third-party health insurance agency.

Iowa Health Insurance Marketplace Guide

If you’re looking for an affordable health insurance plan in Iowa, this state guide, including the FAQs below, can help you better understand your coverage options. For many, an Affordable Care Act (ACA) Marketplace plan, also called Obamacare or an exchange plan, is a cost-effective option.

Iowa uses the federally run health insurance exchange, so residents use HealthCare.gov to compare plans and enroll in coverage.

Six private insurance companies offer health plans through Iowa’s exchange/Marketplace for 2026, including one newcomer. But for 2027, one carrier is leaving the market, so there will only be five participating insurers (see below for details on insurer participation and premium changes for 2027).

As described below, gross premium increases for 2026 were fairly significant, although well below the national average. But a much more important factor for consumers was the net (after-subsidy) premium increases that happened because Congress failed to extend the subsidy enhancements that had been in place since 2021.

Iowa still has a fairly large number of residents enrolled in pre-ACA individual health insurance plans (grandmothered or grandfathered plans). As of 2026, about 17,700 people were enrolled in Wellmark’s pre-ACA individual market plans in Iowa.1 None of these enrollees are receiving premium subsidies, since subsidies are not available for pre-ACA plans. It’s important for people with pre-ACA plans to understand Marketplace options and subsidy eligibility before renewing their pre-ACA coverage.

*Values displayed by this tool are from data generated by CMS and reflect 2026 Marketplace health plans purchased in each state. The values returned are averages based on the plans purchased by consumers of each selected state: subsidy and premium values vary based on factors such as zip code, age, household size, and income.

Iowa Marketplace quick facts

Frequently asked questions about health insurance in Iowa

Who can buy Marketplace health insurance in Iowa?

Anyone who meets the following criteria can buy Marketplace health coverage in Iowa:

- You must live in Iowa

- You must be a U.S. citizen, national, or lawfully present

- You must not be incarcerated

- You must not be enrolled in Medicare

Eligibility for financial assistance (premium subsidies and cost-sharing reductions) is based on your income. Moreover, to qualify for financial assistance with your Marketplace plan, you must:

- Not have access to affordable health coverage through an employer. If your employer offers coverage, but you feel it’s too expensive, use our Employer Health Plan Affordability Calculator to see if you might qualify for premium subsidies in the Marketplace.

- Not qualify for Medicaid or CHIP.

- Not be eligible for premium-free Medicare Part A.4

- If married, file a joint tax return.5

- Not be able to be claimed by someone else as a tax dependent.5

When can I enroll in an ACA-compliant plan in Iowa?

The open enrollment period for 2026 ACA-compliant individual and family health insurance ended on January 15, 2026 in Iowa.6

The open enrollment period for 2027 coverage might be shorter, ending on December 15. But in June 2026, a judge vacated the federal rule change mandating the shorter open enrollment period.7

HHS could appeal the judge’s ruling, or may simply continue to use the open enrollment schedule that was used for the past several years, with a January 15 end date. Iowa Marketplace enrollees should pay close attention to any communications they receive from the Marketplace regarding deadlines for 2027 coverage.

Outside of the open enrollment period, you can only enroll or switch to a different individual market plan if you have a qualifying life event. Examples of qualifying life events include loss of health coverage, gaining a dependent, or permanent relocation (assuming you already had coverage prior to the move). Native Americans can enroll year-round without a specific qualifying life event.

If you have questions about open enrollment, you can learn more in our comprehensive guide to open enrollment. We also have a comprehensive guide to special enrollment periods.

How do I enroll in a Marketplace plan in Iowa?

You can enroll in an Iowa health insurance Marketplace plan by:

- Visiting HealthCare.gov

- Calling 1-800-318-2596 (TTY: 1-855-889-4325). The call center is available 24 hours a day, seven days a week, but it’s closed on holidays.

You can also find local help from local insurance agents, brokers, certified application counselors or an approved enhanced direct enrollment entity.8 They can review options and help you pick a plan to fit your needs. Find local help at localhelp.HealthCare.gov

How can I find affordable health insurance in Iowa?

You can find affordable health plans in Iowa on the ACA Marketplace (HealthCare.gov).

During the open enrollment period for 2026 overage:9

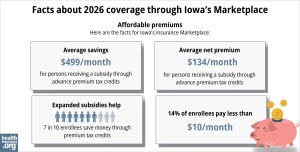

- 76% of Iowa Marketplace enrollees qualified for premium subsidies.

- These premium subsidies (called Advance Premium Tax Credits or APTC) saved Iowa Marketplace enrollees about $499/month on average in 2026.

- Across all Iowa Marketplace enrollees, including the 12% who paid full price, average net premiums amounted to about $235/month. Among enrollees who qualified for a premium subsidy, the average net premium was about $134/month.

Marketplace subsidies are still available in 2026, but they don’t cover as much of enrollees’ total premiums as they did in 2025. And subsidies are no longer available to applicants with total household income above 400% of the federal poverty level.

Source: CMS.gov9

In addition to APTC, if your household income isn’t more than 250% of the federal poverty level, you may also be eligible for cost-sharing reductions (CSR). CSRs help reduce deductibles and out-of-pocket expenses. Note that you must select a Silver-level plan to take advantage of CSR benefits.

Depending on your household income, you may qualify for Iowa Medicaid instead of Marketplace subsidies.

As of 2023, there were still nearly 30,000 people in Iowa who were enrolled in individual grandfathered or grandmothered health plans.10 By 2026, there were still nearly 18,000 people enrolled in these plans.1

These pre-ACA plans do not have to comply with various aspects of the ACA, and people enrolled in these plans cannot get the financial assistance that’s available via the Iowa Health Insurance Marketplace. If you’re enrolled in a pre-2014 health plan, it’s important to double-check your options in the Iowa Marketplace during open enrollment, to see if a newer plan might provide better coverage and/or lower premiums.

How many insurers offer Marketplace coverage in Iowa?

In Iowa, five companies will offer plans through the exchange for 2027:1

- Oscar Insurance Company

- Wellmark Health Plan of Iowa, Inc

- UnitedHealthcare

- Iowa Total Care (Ambetter)

- Avera Health Plans

Six carriers offered exchange plans in Iowa for 2026, but Medica is exiting the individual market in Iowa at the end of 2026. Roughly 4,000 Iowa enrollees will need to select replacement coverage for 2027, due to Medica’s exit.11

Iowa’s Marketplace insurer participation has changed a bit in recent years. Avera Health Plans was new for 2026.12 And UnitedHealthcare and Iowa Total Care (Ambetter) were new for 2025.1314

Are Marketplace health insurance premiums increasing in Iowa?

The following average rate changes have been proposed for 2027 by Iowa’s individual market insurers.1 (Average rate changes are calculated before subsidies are applied.)

Iowa’s ACA Marketplace Plan 2027 PROPOSED Rate Increases by Insurance Company |

|

|---|---|

| Issuer | Percent Increase |

| Avera Health Plans | 14.8% |

| Medica Insurance Company | Exiting market |

| Oscar Insurance Company | 11.9% |

| Wellmark Health Plan of Iowa, Inc | 5% |

| UnitedHealthcare | 11.8% |

| Iowa Total Care (Ambetter) | 16.8% |

Source: Iowa Insurance Division1

Since Wellmark has the large majority of the market share, the overall weighted average rate increase is fairly close to Wellmark’s average, at about 6.7%, before any subsidies are applied.1 This is quite a bit lower than the averages we’re seeing in other states for 2027.

The average full-price rate change in Iowa was also smaller than the national average for 2026.15

But most Iowa exchange enrollees receive premium tax credits and thus don’t pay the full premium amount themselves. If you qualify for subsidies, your actual rate change will also depend on how much your subsidy amount changes. Starting in 2026, subsidies cover a smaller share of enrollees’ total premiums (compared with 2021-2025), and they are available to fewer people. Because Congress failed to extend the federal subsidy enhancements, rates increased significantly for most enrollees.16

To show the magnitude of these rate increases, here are some examples of the sort of net premium increases that people saw in Iowa City for 2026:17

- 40-year-old earning $40,000:

- Lowest-cost plan in 2025 was $33/month

- Lowest-cost plan in 2026 is $152/month

- 60-year-old earning $63,000:

- Lowest-cost plan in 2025 was $189/month

- Lowest-cost plan in 2026 is $748/month (due to the subsidy cliff)

For perspective, here’s a summary of how full-price (unsubsidized) average premiums have changed in Iowa’s individual/family health insurance market over the years:

- 2015: Average increase of 11%.18

- 2016: Average increase of 22.3%.19

- 2017: Average increase of 28.8%.20

- 2018: Average increase of 51%.21

- 2019: Average decrease of 7.9%.22

- 2020: Average decrease of 10.8%.23

- 2021: Average decrease of 0.2%.24

- 2022: Average increase of 6.6%.25

- 2023: Average increase of 2.3%.26

- 2024: Average decrease of 5.5%27

- 2025: Average decrease of 3.1%28

- 2026: Average increase of 15.3%16,29

How many people are insured through Iowa’s Marketplace?

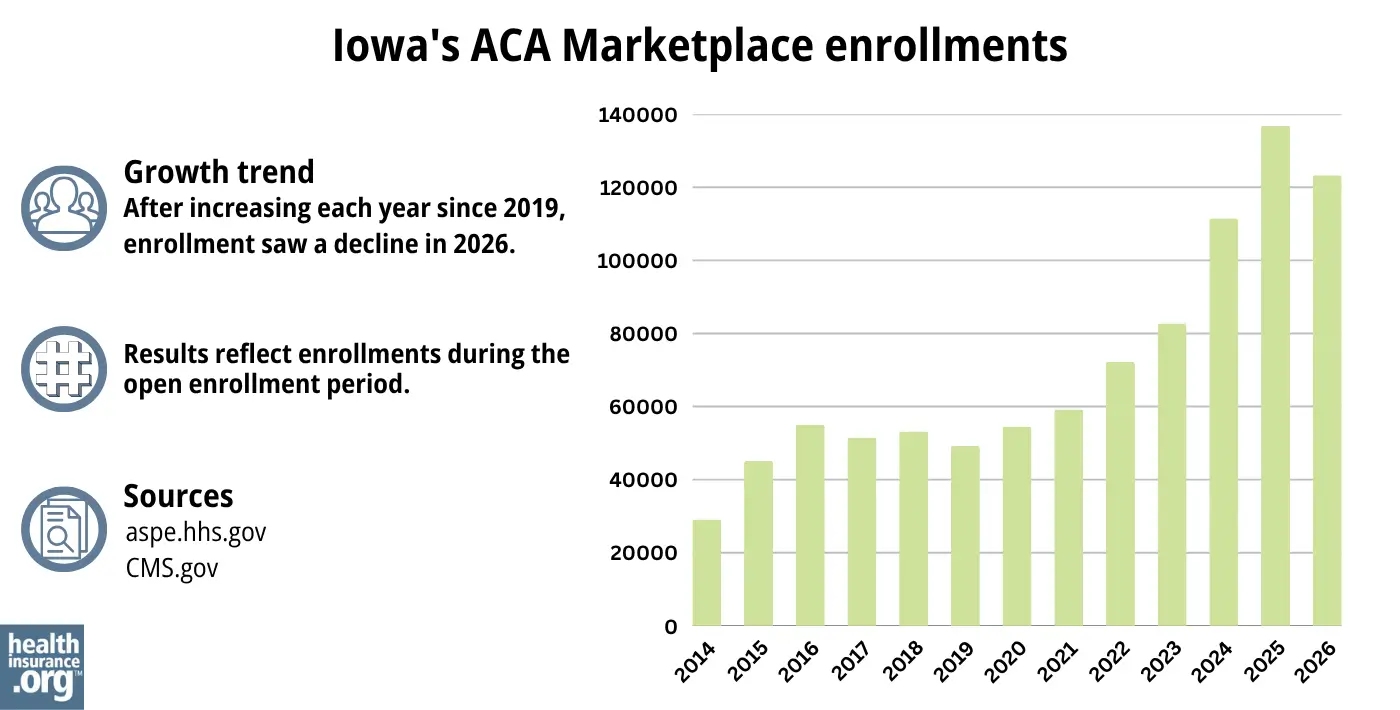

123,304 people selected individual market coverage through the Iowa exchange during the open enrollment period for 2026 coverage,9 which was a reduction from the record-high enrollment Iowa’s exchange had in 2025.

The drop in enrollment for 2026 was due primarily to the fact that Congress did not extend the federal subsidy enhancements that expired at the end of 2025.

The increase in enrollment for the past several years before that (see graph below) was due in large part to the existence of those subsidy enhancements, which were created by the American Rescue Plan (ARP) and extended through 2025 by the Inflation Reduction Act.

The enrollment increase was also partly due to the “unwinding” of the pandemic-era Medicaid continuous coverage rule, as Medicaid disenrollments resumed in the spring of 2023, after a three-year pause. As a result, some people who were previously enrolled in Medicaid transitioned to a Marketplace plan instead.

Source: 2014,30 2015,31 2016,32 2017,33 2018,34 2019,35 2020,36 2021,37 2022,38 2023, 39 2024,40 202541 20269

What health insurance resources are available to Iowa residents?

HealthCare.gov

This is the ACA Marketplace, where you can enroll in a health insurance plan online. You may also get help by calling (800) 318-2596.

Iowa Insurance Division

Get information about insurance and other products regulated by the Iowa Insurance Division (IID). You can also file complaints about insurance with the IID.

Iowa Senior Health Insurance Information Program (SHIIP)

Helps answer questions and provide help to Medicare beneficiaries.

Looking for more information about other options in your state?

Need help navigating health insurance options in Iowa?

Explore more resources for options in IA including short-term health insurance, dental, Medicaid and Medicare.

Speak to a sales agent at a licensed insurance agency.

Footnotes

- ”Health Insurance Rate Increase Data” Iowa Insurance Division. Accessed July 2, 2026 ⤶ ⤶ ⤶ ⤶ ⤶ ⤶

- ”2026 OEP State-Level Public Use File (ZIP)” Centers for Medicare & Medicaid Services, Accessed July 9, 2026 ⤶ ⤶

- ”Iowa Rate Review Submissions” RateReview.HealthCare.gov. Accessed Sep. 17, 2025. *The above is based on the most current data available. ⤶

- Medicare and the Marketplace, Master FAQ. Centers for Medicare and Medicaid Services. Accessed Mar. 20, 2026 ⤶

- Premium Tax Credit — The Basics. Internal Revenue Service. Accessed Mar. 20, 2026 ⤶ ⤶

- “When can you get health insurance?” HealthCare.gov. Accessed July 2, 2026 ⤶

- ”City of Columbus et al. v. Kennedy et al. (Columbus I)” O’Neill Institute, Health Care Litigation Tracker. Shorter OEP vacated June 12, 2026 ⤶

- “Entities Approved to Use Enhanced Direct Enrollment” CMS.gov, Apr. 7, 2026 ⤶

- ”2026 Marketplace Open Enrollment Period Public Use Files” CMS.gov. April 2026 ⤶ ⤶ ⤶ ⤶

- Annual Health Care Costs Report. Iowa Insurance Division. Nov. 15, 2023 ⤶

- ”Medica to exit ACA market in 3 states” Becker’s Payer Issues. June 30, 2026 ⤶

- ”Iowa Health Plans” Avera Health Plans. Accessed Oct. 20, 2025 ⤶

- ”New 2025 Individual Exchange plans and prior authorization information” UnitedHealthcare. Oct. 1, 2024 ⤶

- ”Ambetter Health Expands Health Insurance Offering into Iowa in 2024” Centene Corporation. Oct. 2, 2024 ⤶

- ”2026 Rate Change Project” ACA Signups. Sep. 2, 2025 ⤶

- ”2026 FINAL Gross Rate Changes – Iowa: +15.3% avg (updated)” ACA Signups. Oct. 3, 2025 ⤶ ⤶

- ”See Plans & Prices” (zip 52227) HealthCare.gov. Accessed Oct. 31, 2025 ⤶

- Analysis Finds No Nationwide Increase in Health Insurance Marketplace Premiums. The Commonwealth Fund. December 2014. ⤶

- Iowa: Approved 2016 Rate Hikes Look Like 22.3% (I Think). ACA Signups. August 2015. ⤶

- Avg. UNSUBSIDIZED Indy Mkt Rate Hikes: 25% (49 States + DC). ACA Signups. October 2016. ⤶

- 2018 Rate Hikes. ACA Signups. October 2017. ⤶

- 2019 Rate Hikes. ACA Signups. October 2018. ⤶

- 2020 Rate Changes. ACA Signups. October 2019. ⤶

- Iowa: Preliminary Avg. 2021 #ACA Premiums: -0.2% Individual Market; +0.7% Sm. Group. ACA Signups. October 2020. ⤶

- Iowa: Approved Avg. 2022 #ACA Rate Changes: +6.6% Indy Market; +1.2% Sm. Group. ACA Signups. October 2021. ⤶

- Iowa: Final Avg. Unsubsidized 2023 #ACA Rate Changes: +2.3% (Updated). ACA Signups. August 2022. ⤶

- Iowa: *Final* Avg. Unsubsidized 2024 #ACA Rate Changes: -5.5%. ACA Signups. November 2023 ⤶

- ”Iowa: Preliminary avg. unsubsidized 2025 #ACA rate changes: -3.1% (unweighted)” ACA Signups. Aug. 30, 2025 ⤶

- ”Health Insurance Rate Increase Data” Iowa Insurance Division. Accessed Sep. 17, 2025 ⤶

- “ASPE Issue Brief (2014)” ASPE, 2015 ⤶

- “Health Insurance Marketplaces 2015 Open Enrollment Period: March Enrollment Report”, HHS.gov, 2015 ⤶

- “HEALTH INSURANCE MARKETPLACES 2016 OPEN ENROLLMENT PERIOD: FINAL ENROLLMENT REPORT” HHS.gov, 2016 ⤶

- “2017 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2017 ⤶

- “2018 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2018 ⤶

- “2019 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2019 ⤶

- “2020 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2020 ⤶

- “2021 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2021 ⤶

- “2022 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2022 ⤶

- “Health Insurance Marketplaces 2023 Open Enrollment Report”CMS.gov, 2023 ⤶

- ”HEALTH INSURANCE MARKETPLACES 2024 OPEN ENROLLMENT REPORT” CMS.gov, 2024 ⤶

- “2025 Marketplace Open Enrollment Period Public Use Files” CMS.gov, May 2025 ⤶