Medicare in Louisiana

Original Medicare, Medicare Advantage, Part D prescription drug, and Medigap coverage in Louisiana

Medicare enrollment in Louisiana

As of January 2026, there were 961,260 residents enrolled in Medicare in Louisiana.1

For most beneficiaries, Medicare benefits come with turning 65. But Medicare eligibility is also triggered for younger people if they’re disabled and have been receiving disability benefits for 24 months, or have been diagnosed with amyotrophic lateral sclerosis (ALS) or end-stage renal disease (ESRD).

In Louisiana, 13% of Medicare beneficiaries are under the age of 65,1 versus a nationwide average of about 9%.2

- Understand the difference between Medigap, Medicare Advantage, and Medicare Part D (including tips for picking the best coverage combination to meet your needs).

- Learn how Medicaid can provide assistance to Louisiana Medicare beneficiaries who have limited financial resources.

Medicare Advantage plan availability and enrollment in Louisiana

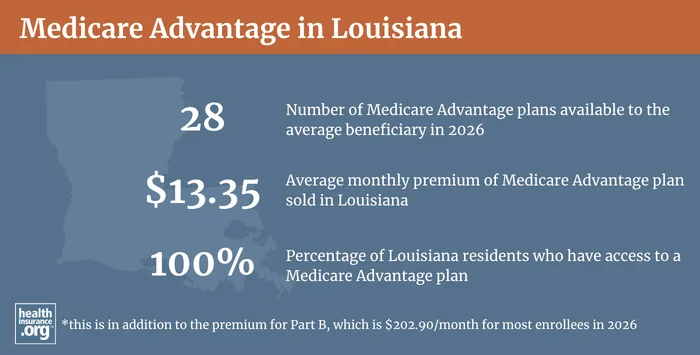

Medicare Advantage plans are available throughout Louisiana. 100% of people with Medicare have access to a Medicare Advantage plan in 2026.3

As of January 2026, Medicare Advantage enrollment in Louisiana stood at 551,9223 people, and 409,338 had Original Medicare.1

Learn more about Medicare Advantage, Medicare’s annual open enrollment period, and the Medicare Advantage open enrollment period.

Sources: Medicare Advantage 2026 Spotlight: A First Look at Plan Offerings, KFF.org, Dec. 9, 2025; Fact Sheet: Medicare Open Enrollment for 2026, Centers for Medicare & Medicaid Services. Sep. 26, 2025

Learn about Medicare plan options in Louisiana by contacting a licensed agent.

Medicare supplement (Medigap) enrollment and regulations in Louisiana

Medigap plans (also known as Medicare supplement plans) will pay some or all of the out-of-pocket costs enrollees would otherwise have to pay if they had only Original Medicare. According to an AHIP analysis, 151,914 Louisiana Medicare beneficiaries had supplemental coverage under Medigap plans as of 2023.4

Learn more about what Medigap plans cover and how they’re standardized.

For 2025, Medicare’s plan finder tool showed 24 Medigap insurers offering plans in the state.5 Medigap insurers in the state are required to maintain minimum loss ratios of at least 65% for individual policies, and at least 75% for employer group policies. This means that at least 65% (or 75% for group plans) of the premium revenue that the insurers bring in must be spent on enrollees’ medical claims.

Unlike other private Medicare coverage (Medicare Advantage and Medicare Part D plans), there is no annual open enrollment window for Medigap plans. Instead, federal rules provide a one-time six-month window when Medigap coverage is guaranteed-issue. This window starts when a person is at least 65 and enrolled in Medicare Part B. (You must be enrolled in both Part A and Part B to buy a Medigap plan.)

And since August 2022, Louisiana has had a “birthday rule” that allows a Medigap enrollee a 63-day window, following their birthday, during which they can switch to another Medigap plan of equal or lesser benefits, offered by the same insurer they already have, with no medical underwriting.6 This is the result of legislation (HB294) that Louisiana enacted in 2022.

Louisiana joined several other states that already had birthday rules on their books. The majority of those other states allow beneficiaries to use their birthday enrollment window to switch to another Medigap plan of equal or lesser benefits offered by any insurer, but Louisiana limits this opportunity only to plans offered by the beneficiary’s current insurer. Legislation was enacted in 2023 in Louisiana that lightly expanded this to allow people to also use the birthday rule window to switch to a plan offered by an affiliate of their current insurer (as opposed to only a plan offered by their current insurer).

Can I get Medigap in Louisiana if I’m under 65 and disabled?

In Louisiana, disabled Medicare beneficiaries under the age of 65 have the same six-month open enrollment period for Medigap plans as a person who becomes eligible for Medicare in Louisiana due to age. But premiums are dramatically higher for enrollees under the age of 65. (In most cases, they’re several times higher: 2026 premiums for Medigap Plan A for a 65-year-old Louisiana male range from $117 to $304/month; for a 50-year-old male, they range from $375 to $1,367/month).5

People who are enrolled in Medicare prior to age 65 have another Medigap open enrollment period when they turn 65. At that point, they can switch to a plan with the lower premiums that apply to people who are aging into Medicare, rather than qualifying due to disability.

Medicare Part D plan availability and enrollment in Louisiana

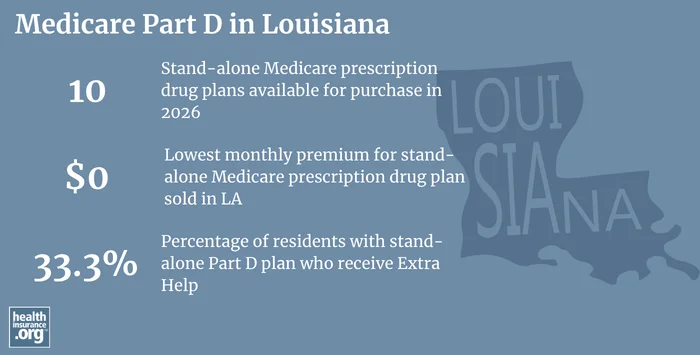

There are 10 stand-alone Medicare Part D plans for sale in Louisiana for 2026, with premiums that start at $0/month.3

As of January 2026, 290,469 beneficiaries of Medicare in Louisiana –had prescription coverage under stand-alone Medicare Part D plans.1 But a much larger population – 516,104 beneficiaries – had Medicare Part D coverage integrated with their Medicare Advantage plans.1 As Advantage enrollment has grown in Louisiana, enrollment in stand-alone Part D plans has dropped, since most Advantage plans have integrated Part D coverage.

Learn how Medicare Part D prescription drug coverage works, what it pays for, how and when to enroll.

Source: Fact Sheet: Medicare Open Enrollment for 2026, Centers for Medicare & Medicaid Services. Sep. 26, 2025

Resources for Medicare beneficiaries in Louisiana

These resources provide free assistance and information about Medicare programs and availability in Louisiana:

- Contact the Louisiana Senior Health Insurance Information Program for help with Medicare enrollment in Louisiana or have questions about Medicare eligibility in Louisiana

- The state has also created a user-friendly stoplight-style quick guide to private Medicare options.

- The Medicare Rights Center website provides information geared to Medicare beneficiaries, caregivers, and professionals.

Looking for more information about other options in your state?

Need help navigating health insurance options in Louisiana?

Explore more resources for options in LA including ACA coverage, short-term health insurance, dental and Medicaid.

Speak to a sales agent at a licensed insurance agency.

Footnotes

- “Medicare Monthly Enrollment – Louisiana” Centers for Medicare & Medicaid Services Data. Accessed May 2026. ⤶ ⤶ ⤶ ⤶ ⤶

- “Medicare Monthly Enrollment – US” Centers for Medicare & Medicaid Services Data, May 2026. ⤶

- “Fact Sheet: Medicare Open Enrollment for 2026” Centers for Medicare & Medicaid Services. Sep. 26, 2025 ⤶ ⤶

- “The State of Medicare Supplement Coverage” AHIP. May 2025 ⤶

- “Explore your Medicare coverage options” Medicare.gov. Accessed May 9, 2026 ⤶ ⤶

- “Louisiana RS 22 §1112” Louisiana State Legislature. Accessed May 9, 2026 ⤶