Find Missouri Health Insurance Marketplace Coverage for 2026

Compare ACA plans and check subsidy savings from a licensed third-party health insurance agency.

Missouri Health Insurance Marketplace Guide

This guide, including the FAQs below, was created to help you understand the health insurance options available to you and your family in Missouri. An Affordable Care Act (ACA) Marketplace plan is cost-effective for many people.

These plans are also called Obamacare or exchange plans (exchange is another word for Marketplace). Missouri uses the federally-facilitated health insurance Marketplace, HealthCare.gov. The Marketplace website will let you shop for health plans offered by several private insurance companies (plan availability varies from one area of the state to another).

For 2026 coverage, eight insurers offer Marketplace plans in Missouri,1 down from nine in 2025 (see details below about premium changes and insurer participation).

If you buy a plan on the Marketplace, the government may help pay for it through an income-based advance premium tax credit. But because Congress did not extend the subsidy enhancements that had been in place since 2021, subsidies are smaller than they would otherwise have been, and available to fewer people in 2026. As a result, net premiums are significantly higher, and some people dropped their coverage altogether at the end of 2025.

*Values displayed by this tool are from data generated by CMS and reflect 2026 Marketplace health plans purchased in each state. The values returned are averages based on the plans purchased by consumers of each selected state: subsidy and premium values vary based on factors such as zip code, age, household size, and income.

Missouri Marketplace quick facts

Frequently asked questions about health insurance in Missouri

Who can buy Marketplace health insurance in Missouri?

You can buy individual and family health insurance from Missouri’s Marketplace if:4

- You live in Missouri.

- You are lawfully present in the U.S.

- You don’t have Medicare.

- You are not incarcerated.

Eligibility for financial assistance with your Marketplace coverage will depend on your income. In addition, to be eligible for financial assistance in the Marketplace:

When can I enroll in an ACA-compliant plan in Missouri?

In Missouri, the open enrollment period to sign up for 2026 ACA-compliant individual and family health plans ended on January 15, 2026.

But starting in the fall of 2026, for health coverage effective in 2027 and future years, the open enrollment period will be shorter. It will still begin on November 1, but it will end on December 15, and all plans selected during open enrollment will take effect January 1.

Outside of open enrollment, you can still make plan changes or enroll in the Marketplace if you qualify for a special enrollment period (SEP). Most SEPs require a qualifying life event, such as involuntary loss of coverage, marriage, or having a baby.

But if you’re an Alaska Native or American Indian, you can enroll anytime.7

Medicaid enrollment is also open year-round, for people who are Medicaid-eligible.

How do I enroll in a Marketplace plan in Missouri?

In Missouri, you have a few options to enroll in a Marketplace health plan:

- Directly through HealthCare.gov – the ACA exchange

- By phone at (800) 318-2596

- By contacting agents, navigators, certified application counselors or an approved enhanced direct enrollment entity.8

- By mailing in a paper application

Many people use the ACA Marketplace, including early retirees not yet on Medicare, self-employed people, and those who work for small businesses without health benefits.

How can I find affordable health insurance in Missouri?

In Missouri, you can find affordable health plans through the ACA Marketplace’s website: HeathCare.gov.

Under the ACA, you may qualify for income-based subsidies called Advance Premium Tax Credits (APTC). These credits lower your premiums.

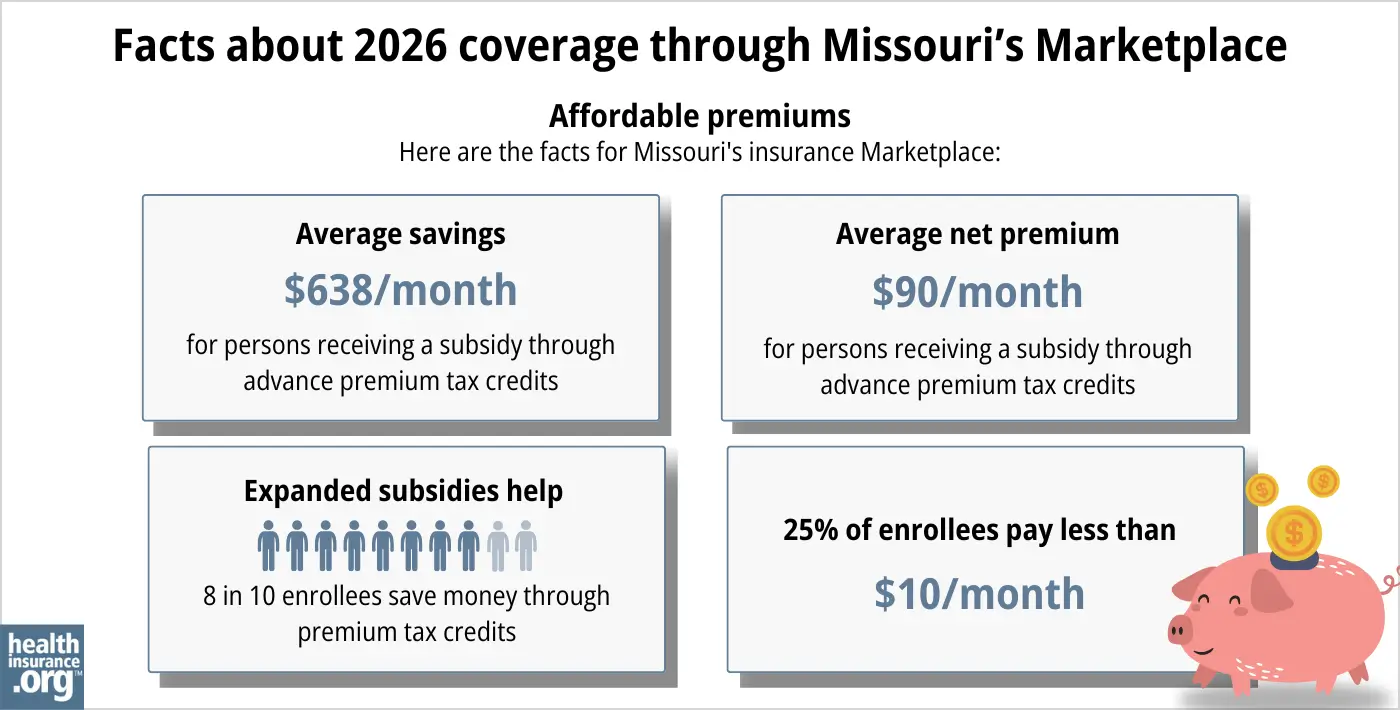

During the open enrollment period for 2026 coverage, 87% of the people who enrolled in coverage through Missouri’s exchange were receiving premium subsidies, saving an average of $638 per month. The average after-subsidy premium was about $90/month.9

But as described below, 2026 premium subsidies don’t cover as much of enrollees’ total premiums as they did in 2025, and fewer people are eligible for these subsidies. This is because Congress allowed federal subsidy enhancements to expire at the end of 2025.

If your income isn’t more than 250% of the federal poverty level, you may also receive cost-sharing reductions (CSR), as long as you enroll in a Silver-level plan.10 CSRs reduce your out-of-pocket costs when you use your health insurance.

Source: CMS.gov 9

Missourians may also find affordable coverage through Medicaid if eligible. Missouri expanded Medicaid eligibility guidelines in 2021, under the terms of a voter-approved ballot measure that implemented the ACA’s Medicaid expansion. This allows adults younger than 65 to enroll in Medicaid with a household income up to 138% of the poverty level. Learn more in our Missouri Medicaid guide.

Short-term plans are also a low-cost option for people who are not eligible for employer plans, Medicaid, Medicare, or subsidies through the exchange. However, short-term health insurance is not regulated by the ACA, so the policies generally do not cover pre-existing conditions, do not cover all of the ACA’s essential health benefits, and are only designed to provide temporary coverage.

How many insurers offer Marketplace coverage in Missouri?

Eight insurers (with varying coverage areas) are offering coverage through Missouri’s Marketplace for 2026,11 down from nine in 2025:12

- Blue Cross Blue Shield of Kansas City

- Celtic Insurance Company

- Cox Health Systems Insurance Company

- Healthy Alliance Life Insurance Company (Anthem)

- Medica Insurance Company

- Oscar Insurance Company

- Media WellFirst

- United Healthcare Insurance Company

As was the case in all states where they offered Marketplace coverage in 2025, Aetna left the market at the end of 2025. Missouri Marketplace enrollees with Aetna plans were able to select new coverage for 2026, during the open enrollment period in late 2025.

There were ten insurers offering plans in 2023,13, but Cigna exited Missouri’s individual insurance market at the end of 2023.14

Are Marketplace health insurance premiums increasing in Missouri?

The following average rate changes were approved for 202611 amounting to a weighted average rate increase of 23.1% before any subsidies are applied.15 (As described below, after-subsidy premium increases were much more significant.)

Missouri’s ACA Marketplace Plan 2026 APPROVED Rate Increases by Insurance Company |

|

|---|---|

| Issuer | Percent Increase |

| Aetna | exited the market |

| Blue Cross Blue Shield of Kansas City | -4.09% |

| Celtic Insurance Company | 24.37% |

| Cox Health Systems Insurance Company | 30.4% |

| Healthy Alliance Life Insurance Company (Anthem) | 22.67% |

| Medica Insurance Company | 29.19% |

| Oscar Insurance Company | 15.69% |

| Medica WellFirst (previously SSM) | 5.35% |

| United HealthCare Insurance Company | 14.86% |

Source: Missouri Department of Insurance11

The approved rate changes apply to full-price premiums. Since most people on Missouri’s exchange receive premium tax credits, they don’t pay the full price.16 If you qualify for subsidies, your net rate change depends on changes in your plan rates and your subsidy amounts.

Unfortunately, the federal subsidy enhancements that had been making Marketplace coverage much more affordable since 2021 expired at the end of 2025. Because Congress did not extend those subsidy enhancements, subsidies do not cover as much of the premiums as they did in 2025, and the “subsidy cliff” has returned. This has made coverage much less affordable than it was in 2025.

A note about rate review in Missouri: Prior to 2017, Missouri did not have an effective rate review program, but that changed in 2017 (as of 2026, only three states — Oklahoma, Tennessee, and Wyoming — do not have an effective rate review program and thus rely on the federal government for this).17

Since 2017, under the terms of SB865, the Missouri Department of Insurance has taken an active role in reviewing insurers’ proposed rate changes.18 State regulators determine whether the proposed rates are justified, although they are not allowed to prevent an insurer from implementing a rate change, even if the state does not consider it to be justified (this is the same as the federal rate review process).

For perspective, here’s a summary of how unsubsidized premiums have changed over the years in Missouri’s individual/family health insurance market:

- 2015: Average increase of 9%19

- 2016: Average increase of 14%20

- 2017: Average increase of 25.5%21

- 2018: Average increase of 40%22

- 2019: Average increase of 1.6%23

- 2020: Average decrease of 2%24

- 2021: Average increase of 4.7%.25

- 2022: Average increase of 2.3%.26

- 2023: Average increase of 11%27

- 2024: Average increase of 4.6%28

- 2025: Average decrease of 1.7%29

How many people are insured through Missouri’s Marketplace?

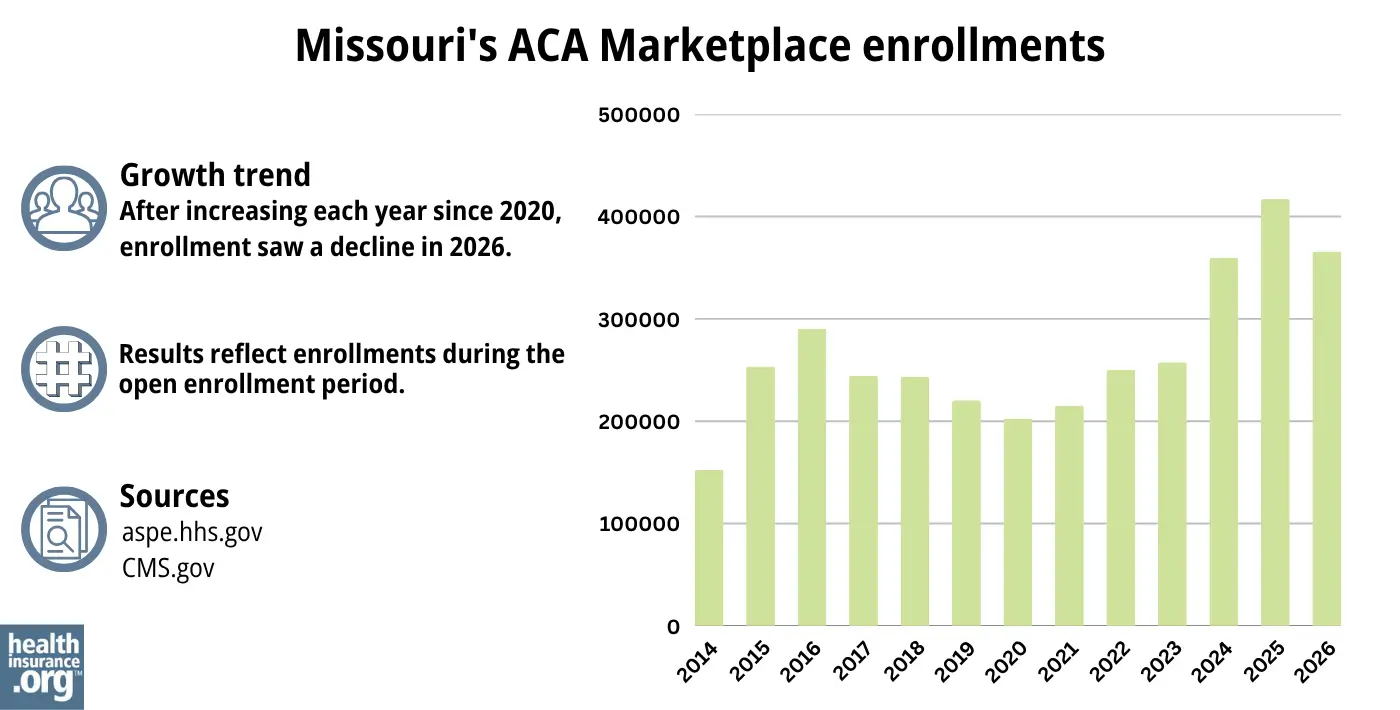

365,734 people selected plans through the Missouri exchange during the open enrollment period for 2026 coverage.9

The 2025 enrollment had been a significant new record high (see graph below). But enrollment declined significantly in 2026, because the expiration of federal subsidy enhancements made coverage much less affordable.

Source: 2014,30 2015,31 2016,32 2017,33 2018,34 2019,35 2020,36 2021,37 2022,38 2023,39 2024,40 202541 20269

Usually, when a state expands Medicaid, Marketplace enrollment drops. That’s because people with income between 100 and 138% of the federal poverty level transfer from Marketplace plans to Medicaid.

But Missouri’s Marketplace enrollment grew in 2022 and 2023 despite the 2021 expansion of Medicaid in Missouri. This growth was likely because of the subsidy enhancements under the American Rescue Plan and the Inflation Reduction Act, which made subsidies larger and more widely available.42 (Unfortunately, those subsidy enhancements expired at the end of 2025, making coverage much less affordable in 2026.)

The enrollment growth in 2024 and 2025 was also driven by the “unwinding” of the pandemic-era Medicaid continuous coverage rule. CMS reported that by April 2024, more than 124,000 Missouri residents had transitioned from Medicaid (MO HealthNet) to a Marketplace plan.43

What health insurance resources are available to Missouri residents?

HealthCare.gov

The official federal website where you can sign up for health insurance plans through the ACA Marketplace.

Missouri Department of Insurance

Oversees and regulates health plans, brokers, and agents.

MO HealthNet

Missouri’s Medicaid.

Missouri State Health Insurance Assistance Program (Missouri SHIP)

Helps Missourians with Medicare benefits.

Medicare Rights Center

National resource with a website and call center to provide information and help for people on Medicare.

Looking for more information about other options in your state?

Need help navigating health insurance options in Missouri?

Explore more resources for options in MO including short-term health insurance, dental, Medicaid and Medicare.

Speak to a sales agent at a licensed insurance agency.

Footnotes

- ”Health Insurance Rate Filings for 2026 Plan Year” Missouri Department of Commerce and Insurance. Accessed Dec. 4, 2025 ⤶

- ”2026 OEP State-Level Public Use File (ZIP)” Centers for Medicare & Medicaid Services, Accessed July 9, 2026 ⤶ ⤶

- ”Missouri 2026 Single Risk Pool Proposed Rate Filings as of 8/1/2025” Missouri Department of Insurance. Aug. 1, 2025 *The above is based on the most current data available. ⤶

- ”A quick guide to the Health Insurance Marketplace” HealthCare.gov. Accessed Dec. 4, 2025 ⤶

- Medicare and the Marketplace, Master FAQ. Centers for Medicare and Medicaid Services. Accessed Dec. 4, 2025 ⤶

- Premium Tax Credit — The Basics. Internal Revenue Service. Accessed Dec. 4, 2025 ⤶ ⤶

- “The Health Insurance Marketplace for American Indians and Alaska Natives” CMS.gov, Accessed Dec. 4, 2025 ⤶

- “Entities Approved to Use Enhanced Direct Enrollment” CMS.gov, Dec. 8, 2025 ⤶

- ”2026 Marketplace Open Enrollment Period Public Use Files” CMS.gov. April 2026 ⤶ ⤶ ⤶ ⤶

- “Federal Poverty Level (FPL)” HealthCare.gov, 2023 ⤶

- ”Missouri 2026 Single Risk Pool Final Rates as of 10/31/202” Missouri Department of Insurance. Oct. 31, 2025 ⤶ ⤶ ⤶

- ”Missouri Department of Commerce and Insurance releases health insurance rates for 2024 with more choices for Missourians” Missouri Department of Commerce and Insurance. Nov. 1, 2024 ⤶

- ”Missouri Department of Commerce and Insurance releases health insurance rates for 2023“ Missouri Department of Insurance. Nov. 1, 2022 ⤶

- ”Missouri Department of Commerce and Insurance releases health insurance rates for 2024 with more choices for Missourians” Missouri Department of Insurance. Nov. 1, 2023. ⤶

- ”2026 Final Gross Rate Changes – Missouri: +23.1%; ~417,000 enrollees looking at massive rate hikes in January (updated)” ACA Signups. Oct. 31, 2025 ⤶

- ”Effectuated Enrollment: Early 2025 Snapshot and Full Year 2024 Average” CMS.gov, July 24, 2025 ⤶

- ”State Effective Rate Review Programs” Centers for Medicare and Medicaid Services. Accessed Mar. 26, 2026 ⤶

- ”Missouri SB865; enacted 2016” BillTrack50. Accessed October 2023. ⤶

- Analysis Finds No Nationwide Increase in Health Insurance Marketplace Premiums. The Commonwealth Fund. December 2014. ⤶

- FINAL PROJECTION: 2016 Weighted Avg. Rate Increases: 12-13% Nationally* ACA Signups. October 2015. ⤶

- Avg. UNSUBSIDIZED Indy Mkt Rate Hikes: 25% (49 States + DC). ACA Signups. October 2016. ⤶

- Alabama, Hawaii, Missouri, Wyoming: Wrapping Up The 2018 Rate Hike Project W/An Assist From Avalere. ACA Signups. October 2017. ⤶

- 2019 Rate Hike Project Wrap-Up: FINAL/APPROVED Rate Changes For Missouri & New Hampshire. ACA Signups. November 2018. ⤶

- Missouri: *Final* Avg. 2020 #ACA Rate Changes: 2.0% Decrease. ACA Signups. October 2019. ⤶

- Missouri: Preliminary Avg. 2021 #ACA Premiums: +4.7% Indy Market, +9.25% Sm. Group. ACA Signups. September 2020 ⤶

- 2022 Rate Changes. ACA Signups. October 2021. ⤶

- Missouri: Final Avg. Unsubsidized 2023 #ACA Rate Changes: +11.0% (Updated). ACA Signups. July 2022. ⤶

- Missouri: *Final* Avg. Unsubsidized 2024 #ACA Rate Changes: +4.6%. ACA Signups. November 2023. ⤶

- ”Missouri: Preliminary avg. unsubsidized 2025 #ACA rate changes: -1.7%; SSM out” ACA Signups. Sep. 4, 2024 ⤶

- “ASPE Issue Brief (2014)” ASPE, 2015 ⤶

- “Health Insurance Marketplaces 2015 Open Enrollment Period: March Enrollment Report”, HHS.gov, 2015 ⤶

- “HEALTH INSURANCE MARKETPLACES 2016 OPEN ENROLLMENT PERIOD: FINAL ENROLLMENT REPORT” HHS.gov, 2016 ⤶

- “2017 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2017 ⤶

- “2018 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2018 ⤶

- “2019 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2019 ⤶

- “2020 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2020 ⤶

- “2021 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2021 ⤶

- “2022 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2022 ⤶

- “Health Insurance Marketplaces 2023 Open Enrollment Report” CMS.gov, 2023 ⤶

- ”HEALTH INSURANCE MARKETPLACES 2024 OPEN ENROLLMENT REPORT” CMS.gov, 2024 ⤶

- “2025 Marketplace Open Enrollment Period Public Use Files” CMS.gov, May 2025 ⤶

- “Health Insurance Marketplaces 2023 Open Enrollment Report” CMS.gov, Accessed August 2023 ⤶

- ”HealthCare.gov Marketplace Medicaid Unwinding Report” Centers for Medicare & Medicaid Services. Data through April 2024; Accessed Aug. 5, 2024 ⤶