Find Alaska Health Insurance Marketplace Coverage for 2026

Compare ACA plans and check subsidy savings from a licensed third-party health insurance agency.

Alaska Health Insurance Marketplace Guide

If you need help understanding the Alaska Marketplace and choosing the right health insurance plan for you and your family, this guide, including the FAQs below, is for you. For many, an Affordable Care Act (ACA) Marketplace plan may be a good option.

Alaska uses the federally facilitated HealthCare.gov Marketplace platform, where plans are available from two private health insurance companies — Moda and Premera.

If you enroll through the Marketplace, you may qualify for financial help from the government through an advance premium tax credit. Most Alaska Marketplace enrollees qualify for these subsidies, and that’s still true in 2026. But because Congress did not extend the subsidy enhancements that expired at the end of 2025, subsidies are available to fewer people in 2026, and don’t cover as much of the premium as they did in 2025.

And the return of the “subsidy cliff” (meaning the loss of all subsidies for households earning more than 400% of the poverty level) was particularly challenging in Alaska, where full-price premiums are much higher than the national average.1 This is true even though overall full price (pre-subsidy) premiums are actually slightly lower in Alaska in 2026 than they were in 2025. For 2027, the weighted average proposed rate increase in Alaska is higher than the national average (see details below).

Alaska was among the first states to implement a reinsurance program, which took effect in 2018. This has helped to keep unsubsidized premiums in the state’s individual/family market significantly lower than they would otherwise have been,2 and the program has been extended through 2027.3

For 20 years, Alaska required fully insured health plans (i.e., plans that aren’t self-insured) to cover out-of-network care under the state’s 80th-percentile rule. But Alaska’s Division of Insurance repealed the 80th Percentile Rule as of January 2024, in a move that generated controversy and a lawsuit filed by medical providers.4 In calling for repeal of the 80th Percentile Rule, Alaska’s insurance regulators expressed concerns that it may have driven healthcare prices higher than they would otherwise be, and noted that it might not be needed anymore, due to the federal No Surprises Act.5

*Values displayed by this tool are from data generated by CMS and reflect 2026 Marketplace health plans purchased in each state. The values returned are averages based on the plans purchased by consumers of each selected state: subsidy and premium values vary based on factors such as zip code, age, household size, and income.

Alaska Marketplace quick facts

Frequently asked questions about health insurance in Alaska

How can I find affordable health insurance in Alaska?

You can find affordable health insurance in Alaska by shopping on the ACA Marketplace/exchange (HealthCare.gov).

Depending on your income and circumstances, you may qualify for income-based subsidies called Advance Premium Tax Credits (APTC) under the ACA. These credits will reduce the amount you have to pay in premiums each month.

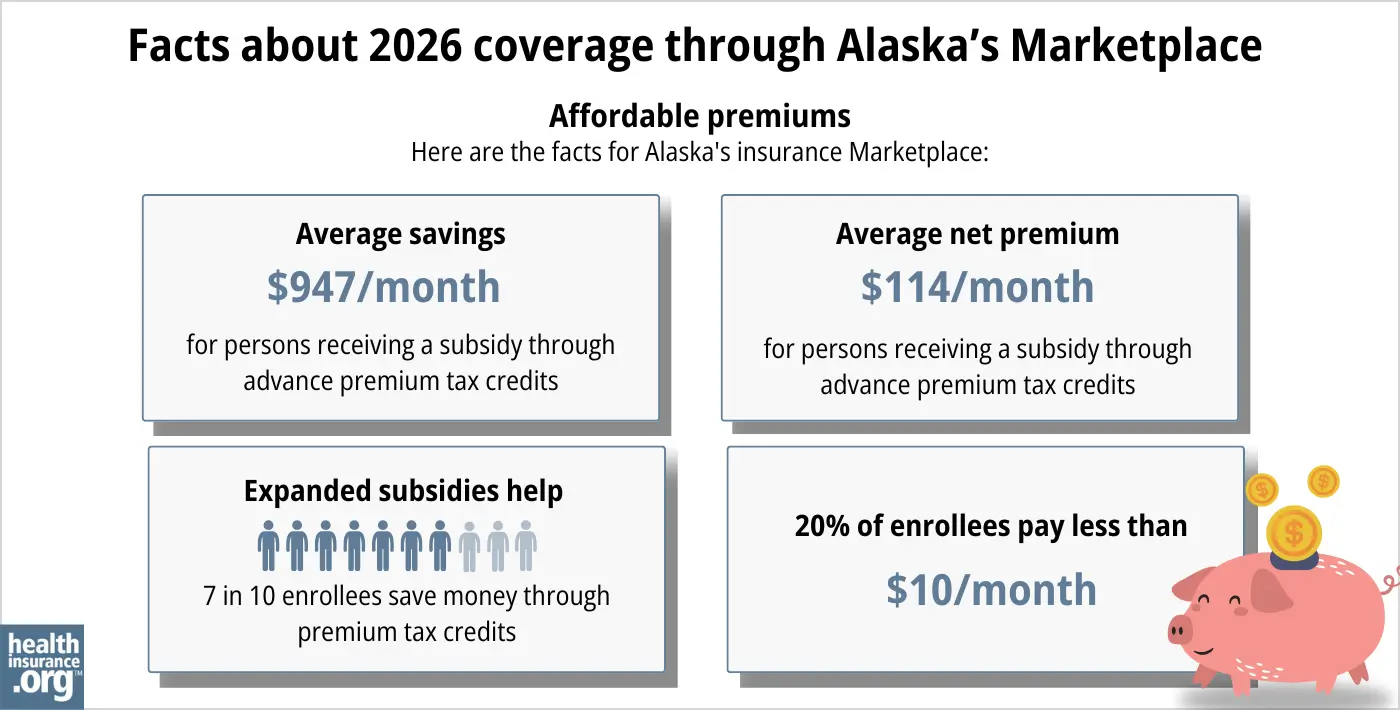

During the open enrollment period for 2026 coverage, 74% of Alaska Marketplace enrollees were eligible for premium subsidies. The average subsidy amount was $947/month, reducing the average subsidy-eligible enrollee’s net premium to $114/month.8

Source: CMS.gov9

Another way to save money while using the Alaska exchange is cost-sharing reductions (CSR).10 You can qualify for CSR if your income is no more than 250% of the prior year’s federal poverty level and you enroll in a Silver-level plan.11

For 2026 coverage, 250% of FPL in Alaska is $48,875 for a single individual and $100,475 for a household of four (note that the FPL numbers are higher in Alaska than they are in the continental United States).12

For 2027 coverage, 250% of FPL in Alaska will be $49,875 for a single individual and $103,125 for a household of four.

Alaska Natives and American Indians qualify for a special version of CSR — with no out-of-pocket costs — if their household income isn’t more than 300% of the federal poverty level. Unlike regular CSR, which is only available on Silver-level plans, the CSR for Alaska Natives and American Indians is available on any metal-level plan.13

If you’re not eligible for Marketplace subsidies, other ways to obtain affordable coverage include:

- Apply for Medicaid if you’re eligible: You can begin the enrollment process through HealthCare.gov (you’ll be directed to the state Medicaid program if it appears you’re eligible) or my.alaska.gov. Our Alaska Medicaid eligibility guide walks you through the details of Medicaid eligibility in Alaska.

- Look into short-term health insurance: If you’re looking for a more budget-friendly option, at least one insurer in Alaska offers temporary short-term health insurance plans. However, these plans are not regulated by the ACA and subsidies are not available to offset their cost.

Who can buy Marketplace health insurance in Alaska?

Here are the eligibility requirements for health coverage through the Marketplace in Alaska:14

- You must live in Alaska.

- You must be lawfully present in the U.S.

- You must not be incarcerated.

- You must not be enrolled in Medicare.

Although most Alaska residents are thus eligible to use the Marketplace, eligibility for financial assistance (premium subsidies and cost-sharing reductions) has stricter rules. It depends on your income and how it compares with the cost of the second-lowest-cost Silver plan in your area – which depends on your age and location. In addition, to qualify for Marketplace financial assistance you must:

- Not have access to affordable health coverage offered by an employer. If your employer offers coverage but you feel it’s too expensive, you can use our Employer Health Plan Affordability Calculator to see if you might qualify for premium subsidies in the Marketplace.

- Not be eligible for Medicaid or CHIP.

- Not be eligible for premium-free Medicare Part A.15

- If you’re married, you must file a joint tax return with your spouse.16 (with very limited exceptions)17

- Not be able to be claimed by someone else as a tax dependent.18

When can I enroll in an ACA-compliant plan in Alaska?

The open enrollment period to sign up for 2027 ACA-compliant individual and family health plans in Alaska is expected to run from November 1, 2026 until January 15, 2027.

The federal government finalized a rule change in 2025 that called for a shorter open enrollment period starting in the fall of 2026 (ending December 15), but a federal judge vacated that rule change in June 2026, and HHS appealed the judge’s ruling in July 2026.19 So as of early August 2026, there was still some uncertainty about the open enrollment deadline.

But regardless of how the court case plays out, consumers should plan to enroll by December 15, 2026. That might end up being the final day of open enrollment. But if not, it will be the last day to pick a plan with a January 1 effective date.

You can still make plan changes or enroll in the Marketplace beyond the open enrollment window. However, you must qualify for a special enrollment period (SEP). SEPs generally require a qualifying life event, such as losing your health coverage involuntarily or gaining a dependent.

But American Indians and Alaska Natives can enroll anytime, without a specific qualifying life event.13

How do I enroll in a Marketplace plan in Alaska?

To enroll in an Alaska Marketplace health plan, you can:

- Go to HealthCare.gov online – the ACA exchange website.

- Dial the Marketplace Call Center at (800) 318-2596.

- Contact an agent/broker, navigator, or certified application counselor.

- Enroll via an approved enhanced direct enrollment entity.20

Go to localhelp.HealthCare.gov to find a navigator, certified application counselor, or agent in your area.

How many insurers offer Marketplace coverage in Alaska?

Two insurance companies offer plans for 2026 in Alaska’s health insurance Marketplace,21 and both will continue to offer coverage in 2027:22

- Moda Assurance Company

- Premera Blue Cross Blue Shield of Alaska

Premera Blue Cross Blue Shield of Alaska offers coverage statewide in 2026, while Moda Assurance offers plans in the Municipality of Anchorage, Matanuska-Susitna Borough, Kenai Peninsula Borough, Fairbanks North Star Borough, and Southeast Alaska.21

Are Marketplace health insurance premiums increasing in Alaska?

The following average rate changes (before subsidies) have been proposed by Alaska’s Marketplace insurers for 2027, amounting to a weighted average proposed rate increase of 22.9%:23

Alaska’s ACA Marketplace Plan 2027 PROPOSED Rate Changes by Insurance Company |

|

|---|---|

| Issuer | Percent Increase |

| Moda Assurance Company | 9.3% |

| Premera Blue Cross Blue Shield of Alaska | 26.7% |

Source: RateReview.HealthCare.gov22

For 2026, Alaska was the only state in the country where average full-price premiums decreased.24 But for 2027, Alaska has among the highest proposed average rate increases in the country.

And even though full-price premium changes were quite small in Alaska for 2026, the net premiums that people are paying still increased after Congress failed to extend the subsidy enhancements that expired at the end of 2025. Across all enrollees, including those paying full price, the average net premium in the Alaska Marketplace in 2025 was $223/month,25 and that grew to $344/month in 2026.26

For perspective, here’s a look at how average pre-subsidy premiums have changed in Alaska’s individual/family market over the years:

- 2015: Average increase of 31% (largest in the nation)27

- 2016: Average increase of 39%28

- 2017: Average increase of 7.3% (and Moda exited the market)29

- 2018: Average decrease of 22%30 (reinsurance program took effect)

- 2019: Average decrease of 3.9%31

- 2020: Average rates unchanged32 (Moda rejoined the market).

- 2021: Average unweighted decrease of 2%33

- 2022: Average decrease of 3.7%34

- 2023: Average increase of 19.1%35

- 2024: Average increase of 16.4%36

- 2025: Average rate increase of 17.1%37

- 2026: Average rate decrease of 1.1% (only state where full-price premiums decreased for 2026).38

How many people are insured through Alaska’s Marketplace?

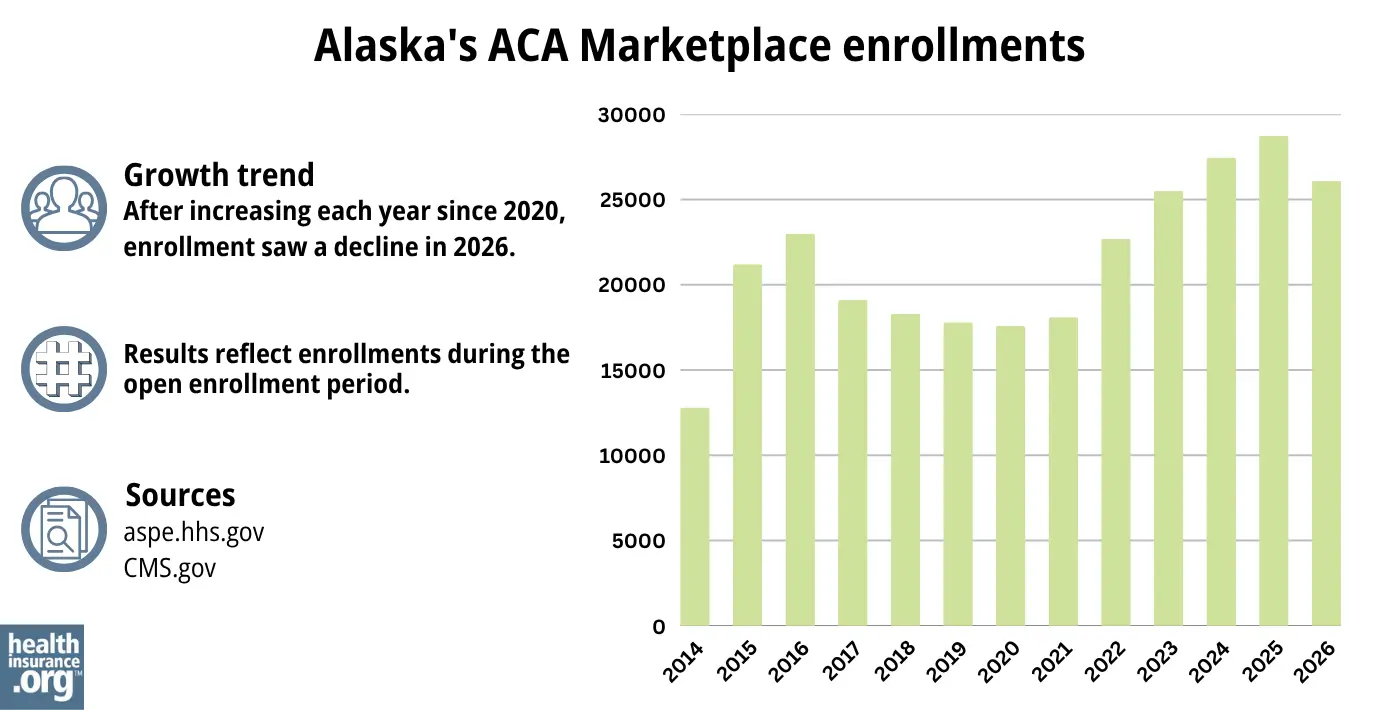

During open enrollment for 2026 health coverage, 26,079 people signed up for private health plans through Alaska’s exchange.39 This was lower than enrollment had been in 2024 and 2025; you can see previous year enrollments in the chart below.

Prior to 2026, Alaska’s Marketplace enrollment had been steadily increasing since 2020. This growth was due in part to American Rescue Plan subsidy enhancements, which continued through 2025 thanks to the Inflation Reduction Act.40 The expiration of these subsidy enhancements at the end of 2025 was the reason enrollment decreased in 2026, for the first time in several years.

The enrollment growth in 2024 and 2025 was also partly due to the “unwinding” of the pandemic-era Medicaid continuous coverage rule. By April 2024, more than 6,000 Alaska residents had transitioned from Medicaid to a Marketplace plan during the unwinding period.41

Source: 2014,42 2015, 43 2016,44 2017,45 2018,46 2019,47 2020,48 2021,49 2022,50 2023,51 2024,52 202553 20268

What health insurance resources are available to Alaska residents?

HealthCare.gov

The official federal website where you can sign up for health insurance plans through the ACA Marketplace.

Denali KidCare

Alaska’s children’s health insurance program.

United Way of Anchorage

Federally funded Navigator organization to assist with Medicaid and exchange enrollment in Alaska.

Alaska State Health Insurance Counseling and Assistance Programs (SHIP)

Enrollment counseling and advice to Medicare beneficiaries and their caregivers.

Medicare Rights Center

A national service for Medicare-related questions.

Alaska Comprehensive Health Insurance Association

Created by the Alaska State Legislature to provide coverage for residents unable to obtain individual health insurance.

Looking for more information about other options in your state?

Need help navigating health insurance options in Alaska?

Explore more resources for options in AK including short-term health insurance, dental, Medicaid and Medicare.

Speak to a sales agent at a licensed insurance agency.

Footnotes

- ”Hold Onto Your Hats: How much more will ALASKA residents pay if the improved #ACA subsidies aren’t extended?” ACA Signups. Aug. 11, 2025 ⤶

- Section 1332 State Innovation Waiver extension request. State of Alaska. March 2022 ⤶

- Alaska: State Innovation Waiver – Extension. Centers for Medicare and Medicaid Services. July 12, 2022. ⤶

- ”Despite opposition from health care providers, Dunleavy administration repeals longstanding regulation meant to hold down costs” Alaska Public Media. January 11, 2024. ⤶

- ”80th Percentile Rule” Alaska Division of Insurance. Accessed Dec. 9, 2025 ⤶

- ”2026 OEP State-Level Public Use File (ZIP)” Centers for Medicare & Medicaid Services, Accessed July 9, 2026 ⤶ ⤶

- ”Alaska Rate Review Submissions” RateReview.HealthCare.gov. Accessed Aug. 11, 2025 *The above is based on the most current data available. ⤶

- ”2026 Marketplace Open Enrollment Period Public Use Files” Centers for Medicare & Medicaid Services. Accessed March 2026 ⤶ ⤶

- “2026 Marketplace Open Enrollment Period Public Use Files” CMS.gov, March 2026 ⤶

- ”APTC and CSR Basics” Centers for Medicare & Medicaid Services. Oct. 2025 ⤶

- “Federal Poverty Level (FPL)” HealthCare.gov. Accessed Apr. 14, 2026 ⤶

- ”2025 Poverty Guidelines” United States Department of Health & Human Services. Accessed Aug. 11, 2025 ⤶

- “The Health Insurance Marketplace for American Indians and Alaska Natives” CMS.gov, Accessed Apr. 14, 2026 ⤶ ⤶

- “A quick guide to the Health Insurance Marketplace®” HealthCare.gov, Accessed Apr. 14, 2026 ⤶

- Medicare and the Marketplace, Master FAQ. Centers for Medicare and Medicaid Services. Accessed Apr. 14, 2026 ⤶

- Premium Tax Credit — The Basics. Internal Revenue Service. ⤶

- Updates to frequently asked questions about the Premium Tax Credit. Internal Revenue Service. February 2024. ⤶

- Premium Tax Credit — The Basics. Internal Revenue Service. Accessed Apr. 14, 2026 ⤶

- ”City of Columbus et al. v. Kennedy et al. (Columbus I)” O’Neill Institute, Georgetown Law. Accessed Aug. 2, 2026 ⤶

- “Entities Approved to Use Enhanced Direct Enrollment” CMS.gov, Apr. 7, 2026 ⤶

- ”Individual Health Insurance for 2026” Alaska Division of Insurance. Accessed Dec. 9, 2025 ⤶ ⤶

- ”Alaska Rate Review Submissions” RateReview.HealthCare.gov. Accessed Aug. 2, 2026 ⤶ ⤶

- ”Alaska Rate Review Submissions” RateReview.HealthCare.gov. Accessed Aug. 2, 2026. Weighted average based on enrollment totals in filings: 5,106 for Moda, and 18,561 for Premera ⤶

- ”2026 Rate Change Project” ACA Signups. Oct. 3, 2026 ⤶

- ”2025 Marketplace Open Enrollment Period Public Use Files” Centers for Medicare & Medicaid Services. Accessed Apr. 14, 2026 ⤶

- ”2026 Marketplace Open Enrollment Period Public Use Files” Centers for Medicare & Medicaid Services. Mar. 27, 2026 ⤶

- Analysis Finds No Nationwide Increase in Health Insurance Marketplace Premiums. The Commonwealth Fund. December 2014. ⤶

- Alaska: OUCH. Approved 2016 Individual Market Rate Hikes: 39% Weighted Avg. ACA Signups. August 2015. ⤶

- Premera’s Alaska rates to rise 7 percent next year, less than estimated. Anchorage Daily News. September 2016. ⤶

- 2018 Rate Hikes. ACA Signups. October 2017. ⤶

- 2019 Rate Hikes. ACA Signups. October 2018. ⤶

- 2020 Rate Changes. ACA Signups. October 2019. ⤶

- Alaska: Preliminary Avg. 2021 #ACA Premium Rate Change: -2% Indy Market, -1.9% Sm. Group (Unweighted). ACA Signups. October 2020. ⤶

- *APPROVED* Avg. 2022 #ACA Rate Changeapalooza! AK, CA, GA, HI, IL, KS, LA, MA, MS, MO, NE, NH, TX, WY. ACA Signups. November 2021. ⤶

- Alaska: Final Avg. Unsubsidized 2023 #ACA Rate Changes: +19.1%. ACA Signups. November 2022. ⤶

- Alaska: *Final* Avg. Unsubsidized 2024 #ACA Rate Changes: +16.4% (Updated). ACA Signups. November 2023. ⤶

- ”Alaska: Preliminary avg. unsubsidized 2025 #ACA rate changes: +17.1%” ACA Signups. Aug. 13, 2024 ⤶

- ”2026 Final Gross Rate Changes – Alaska: -1.1%…but up to ~27,000 enrollees are STILL likely looking at MASSIVE rate hikes regardless (updated)” ACA Signups. Oct. 31, 2025 ⤶

- ”2026 Marketplace Open Enrollment Period Public Use Files” Centers for Medicare & Medicaid Services. Accessed March 2026 ⤶

- “Health Insurance Marketplaces 2023 Open Enrollment Report” CMS.gov, Accessed August 2023 ⤶

- ”HealthCare.gov Marketplace Medicaid Unwinding Report” Centers for Medicare & Medicaid Services. Data through April 2024; Accessed Aug. 5, 2024 ⤶

- “ASPE Issue Brief (2014)” ASPE, 2015 ⤶

- “Health Insurance Marketplaces 2015 Open Enrollment Period: March Enrollment Report”, HHS.gov, 2015 ⤶

- “HEALTH INSURANCE MARKETPLACES 2016 OPEN ENROLLMENT PERIOD: FINAL ENROLLMENT REPORT” HHS.gov, 2016 ⤶

- “2017 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2017 ⤶

- “2018 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2018 ⤶

- “2019 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2019 ⤶

- “2020 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2020 ⤶

- “2021 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2021 ⤶

- “2022 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2022 ⤶

- “Health Insurance Marketplaces 2023 Open Enrollment Report” CMS.gov, 2023 ⤶

- ”HEALTH INSURANCE MARKETPLACES 2024 OPEN ENROLLMENT REPORT” CMS.gov, 2024 ⤶

- “2025 Marketplace Open Enrollment Period Public Use Files” CMS.gov, May 2025 ⤶