Find Washington Health Insurance Marketplace Coverage for 2026

Compare ACA plans and check subsidy savings from a licensed third-party health insurance agency.

Washington Health Insurance Marketplace Guide

We created this health insurance guide, including the FAQs below, to help you understand the coverage options and potential financial assistance available to you and your family in the state of Washington.

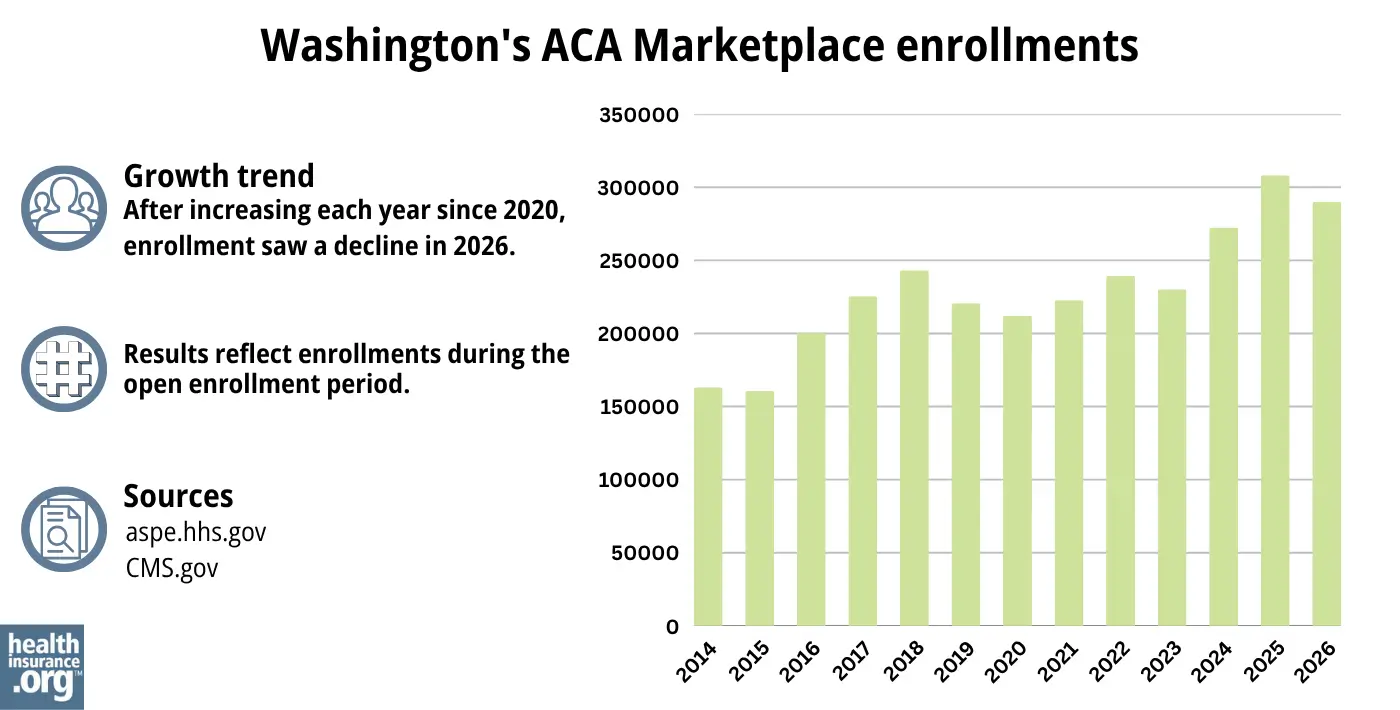

Washington runs its own health insurance exchange (Marketplace), called Washington Healthplanfinder. Residents who need to buy their own health insurance – including those who aren’t eligible for Medicare, Medicaid, or an affordable employer-sponsored health plan – can use Washington Healthplanfinder to compare plans and enroll in coverage. About 290,000 people selected coverage through Washington Healthplanfinder for 2026.1

Twelve private insurers offer 2026 coverage through Washington’s exchange, with varying service areas. This is up from 11 in 2025, as one new insurer joined the exchange for 2026. For 2027, all 12 insurers have filed Marketplace plans, with an overall proposed average rate increase of more than 22%, before subsidies are applied (details below).

Public option (Cascade Select Plans) and standardized plans (Cascade Plans) — collectively known as Cascade Care — became available as of 2021 in Washington. By 2026, nine out of ten Washington Healthplanfinder enrollees were in Cascade Care plans.2

Washington is among the states that provide additional state-funded subsidies, in addition to federal health insurance subsidies.3 The Cascade Select (public option) program has been growing over time, and the plans became available statewide for the first time in 2025.4

For 2026, Washington’s state-funded subsidies (Cascade Care Savings) amount to $55 per member per month for most enrollees with household income up to 250% of the federal poverty level.5 This is smaller than the Cascade Care Savings subsidy that was provided in 2025, but Washington has begun using premium alignment (silver loading) for the 2026 plan year,6 which makes Gold plans more affordable for most enrollees, even with the smaller Cascade Care Savings and the expiration of the federal subsidy enhancements.5 As a result, Bronze plan enrollments decreased in Washington for 2026, whereas they increased significantly in most states.

(In Washington, insurers are adding a 43% load to the cost of Silver plans sold through Washington Healthplanfinder, to account for the fact that the federal government stopped funding cost-sharing reductions several years ago.5 This increases the cost of Silver plans, which also increases the size of premium subsidies, since premium subsidy amounts are based on the cost of Silver coverage. This rule will continue to be in place for 2027.)7

Washington’s exchange can be used by undocumented immigrants, under a 2023 waiver the state obtained from the federal government.8 As described below, this includes DACA recipients, who are no longer eligible to use the Marketplaces in other states.

Washington ACA Marketplace quick facts

Frequently asked questions about health insurance in Washington

Who can buy Marketplace health insurance in Washington?

To be eligible to enroll in private health coverage through Washington Healthplanfinder, you must:11

- Live in Washington

- Not be incarcerated

- Not be enrolled in Medicare

Under the ACA, a person must also be lawfully present in the U.S. to use the exchange/Marketplace in any state. But Washington obtained federal permission to allow undocumented immigrants to enroll in health plans through Washington Healthplanfinder starting with the 2024 plan year. The approval is effective through 2028,12 but could be extended in the future.

Undocumented immigrants are not eligible for federal subsidies, but Washington Healthplanfinder can provide them with state-funded Cascade Care Savings subsidies if their income doesn’t exceed 250% of the poverty level.12

A federal rule change took effect in November 2024, allowing DACA recipients to enroll in the Marketplaces nationwide, with access to the same income-based federal subsidies that are available to U.S. citizens and lawfully present residents. But a subsequent rule change revoked that access as of August 25, 2025.

DACA recipients can still use Washington Healthplanfinder (which isn’t the case for other state-run Marketplaces or HealthCare.gov) because Washington has federal permission for undocumented immigrants to use the Marketplace. But they are no longer eligible for federal subsidies due to the 2025 rule change13 (state-funded subsidies are still available).

In addition to basic enrollment eligibility, additional parameters must be met to qualify for financial assistance. To be eligible for income-based federal Advance Premium Tax Credits (APTC), state-funded Cascade Care Savings (state subsidies), or federal cost-sharing reductions (CSR), you must:

- Not have access to an affordable plan offered by an employer. If you are eligible to sign up for an employer’s plan and aren’t sure whether it’s considered affordable, you can use our Employer Health Plan Affordability Calculator to see if you might qualify for premium subsidies for a plan obtained through Washington Healthplanfinder.

- Not be eligible for Apple Health (Medicaid/CHIP).

- Not be eligible for premium-free Medicare Part A.14

- File a joint tax return with your spouse, if you’re married.15 (with very limited exceptions)16

- Not be able to be claimed by someone else as a tax dependent.15

Beyond those basic requirements, premium subsidy eligibility depends on your household’s income and how it compares with the cost of the second-lowest-cost Silver plan in your area – which depends on your age and location.

When can I enroll in an ACA-compliant plan in Washington?

Washington Healthplanfinder has announced that open enrollment for 2027 coverage will run from November 1, 2026 through December 31, 2026.17 All plans selected during open enrollment will take effect January 1.

This is shorter than open enrollment has been in the past (for 2026 coverage, it continued through January 15, 2026),1 due to a federal rule change that requires open enrollment to end no later than December 31.

Outside of the annual open enrollment period, you may still be able to enroll or make a plan change if you experience a qualifying life event, such as giving birth or losing other health coverage. And Native Americans can enroll year-round, without a specific qualifying life event.

Enrollment in Washington’s Apple Health (Medicaid) is available year-round for eligible applicants.

How do I enroll in a Marketplace plan in Washington?

To enroll in an ACA Marketplace/exchange plan in Washington, you can:

- Visit Washington Healthplanfinder – the state’s health insurance exchange – to compare the health plans that are available in your area, determine whether you’re eligible for financial assistance (including federal subsidies and Washington’s Cascade Care Savings), and enroll in coverage during open enrollment or during a special enrollment period.

- Enroll in coverage through Washington Healthplanfinder with the help of an insurance agent or broker, or an exchange-certified Navigator.

You can reach Washington Healthplanfinder’s customer service team at 855-923-4633 (TTY/TDD: 855-627-9604). They are available Monday through Friday, 7:30 am to 5:30 pm.

How can I find affordable health insurance in Washington?

When you enroll in a health plan through Washington Healthplanfinder, you may find that you’re eligible for premium subsidies under the ACA. And for those with income up to 250% of the federal poverty level, the assistance may be more robust than it is in many other states, as both federal and state subsidy programs are available in Washington.

The state-funded subsidy program is called Cascade Care Savings. It’s available to enrollees who select a Silver or Gold Cascade Care plan through Washington Healthplanfinder, if their household income isn’t more than 250% of FPL.

For 2026, most applicants with household income up to 250% of the federal poverty level get an additional $55 per member per month from the Cascade Care Savings program, which reduces their premium costs. This is a smaller amount than the program provided in 2025, but the state’s new approach of premium alignment (silver loading, which increases the cost of Silver plans and thus results in larger federal premium subsidies) ensures that Gold Cascade Care plans remain affordable.5

Applicants with eligible income who aren’t eligible for federal subsidies (including undocumented immigrants) get $250 per member per month in Cascade Care Savings.

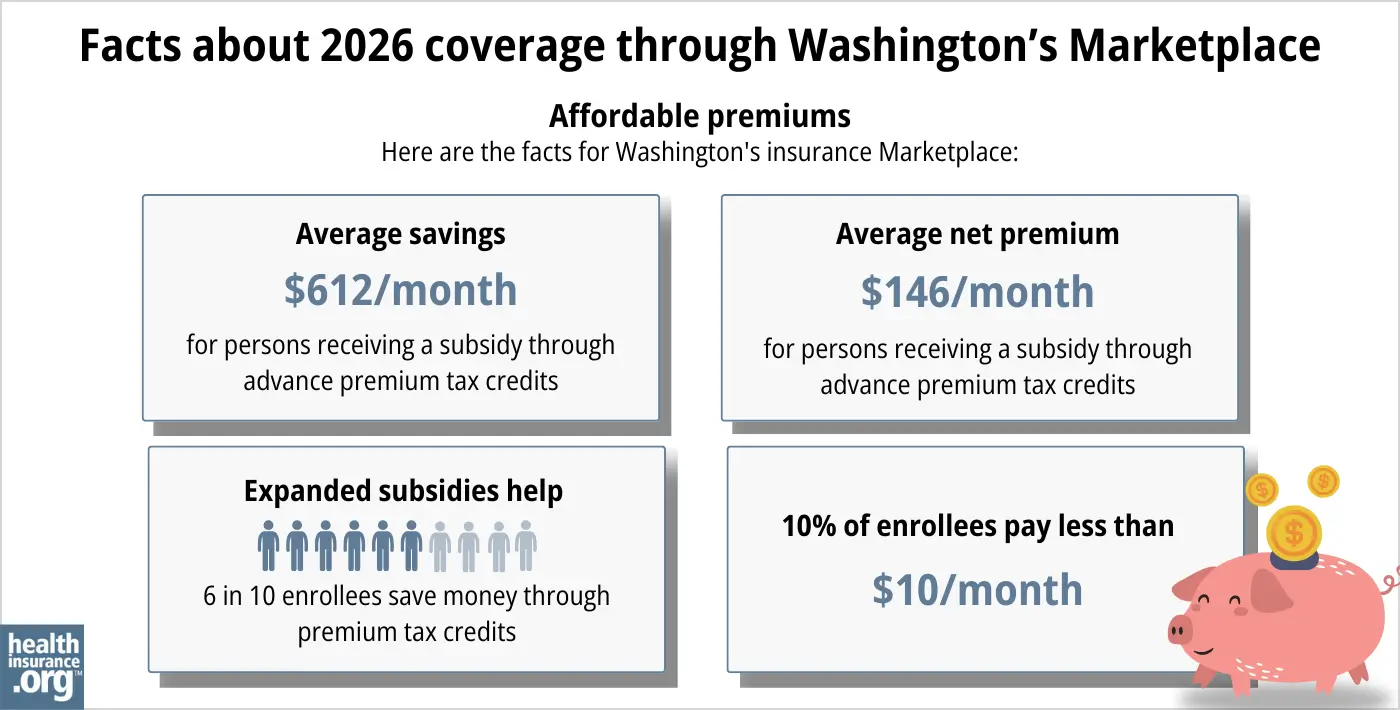

Nearly 64% of Washington Healthplanfinder enrollees qualified for federal APTC during the open enrollment period for 2026 coverage. These subsidies covered an average of $612/month, reducing the average APTC-eligible enrollee’s net premium to about $146/month.18 (For those eligible for Washington’s Cascade Care subsidy, it’s provided in addition to federal APTC, further reducing their monthly premiums.)

Source: CMS.gov18

Applicants with household income up to 250% of the federal poverty level are also eligible for federal cost-sharing reductions (CSR), which will reduce the deductible and other out-of-pocket expenses for Silver-level plans. About 17% of the people who selected plans through Washington Healthplanfinder for 2026 were receiving CSR benefits.18

And as noted above, Washington is among the states where additional state-funded subsidies are available. Starting in 2023, Washington began offering state-funded premium subsidies for applicants with income up to 250% of the poverty level, as long as they select a Cascade Care Silver or Gold plan. The Cascade Care Savings are available in addition to the federal premium subsidies and cost-sharing reductions.19

(Note that federal APTC can be used with any metal-level plan, federal CSR is available with any Silver-level plan, and Cascade Care Savings are available with Silver or Gold Cascade Care plans. To receive all three benefits at once, an eligible enrollee would need to have income up to 250% of the poverty level and select a Silver Cascade Care plan.)

Depending on your income and circumstances, you may be able to enroll in free or low-cost health coverage through Apple Health (Washington Medicaid). Learn more about whether you might be eligible for Medicaid in Washington.

Starting in July 2024, a limited number of undocumented immigrant adults in Washington were able to enroll in Medicaid (Apple Health) if their income wasn’t more than 138% of the federal poverty level.20 This coverage is free, whereas the Marketplace coverage for undocumented immigrants averages about $210/month after the state-funded subsidies are applied.21

But the state only had enough funding to provide Apple Health coverage to 13,000 undocumented immigrants, and that enrollment cap was reached within just a couple of days. After that, undocumented residents could apply and be put on a waiting list in case spots opened up, but Washington announced in early 2026 that enrollment in Apple Health Expansion was officially closed due to funding concerns. Coverage continues for people already enrolled in the program (for now), but nobody new can join.22

Apple Health sought additional funding from the state legislature, to further expand Apple Health coverage for undocumented immigrants.23 But although the budget that was approved in 2025 did continue funding for Apple Health Expansion, it kept that funding at the existing level.24 And H.R. 1 (the “One Big Beautiful Bill Act”), enacted in 2025, will trigger Medicaid funding cuts nationwide, which puts more pressure on Apple Health going forward.22

How many insurers offer Marketplace coverage in Washington?

Twelve insurers are offering Marketplace coverage for 2026 in Washington, including one newcomer,25 and all twelve will continue to offer Marketplace coverage in 2027:2

- BridgeSpan Health Company

- Community Health Plan of Washington

- Coordinated Care Corporation

- Kaiser Foundation Health Plan of the Northwest

- Kaiser Foundation Health Plan of Washington

- LifeWise Health Plan of Washington

- Molina Healthcare of Washington

- Premera Blue Cross

- Regence BlueCross BlueShield of Oregon

- Regence BlueShield

- UnitedHealthcare of Oregon

- WellPoint Washington, Inc. (new for 2026)

(Note: Providence Health Plan is exiting the individual market in Washington at the end of 2026, but Providence only offers off-exchange plans in Washington in 2026,26 so this does not affect anyone with Marketplace coverage.)

There were 12 participating insurers in 2024, but PacificSource (which offered Marketplace plans in four counties in 2024, and was the only carrier that offered PPO plans27) exited the Washington market at the end of 2024.28

(Note: PacificSource continued to offer Marketplace coverage for 2026 in Idaho, Montana, and Oregon, but has announced that those plans will terminate at the end of 2026 and the company will no longer offer Marketplace coverage in any state as of 2027.)

So there were 11 participating insurers for 2025. All of them are continuing to offer plans in 2026, plus one new insurer (Wellpoint Washington), bringing the number of participating carriers back to a dozen.

Are Marketplace health insurance premiums increasing in Washington?

For 2027, the following average rate increases have been proposed by the insurers that offer individual/family coverage offered through Washington Healthplanfinder, amounting to an overall average rate increase of more than 22%, before subsidies are applied:2

Washington’s ACA Marketplace Plan 2027 PROPOSED Rate Increases by Insurance Company |

|

|---|---|

| Issuer | Percent Increase |

| BridgeSpan Health Company | 12.65% |

| Community Health Plan of Washington | 24.5% |

| Coordinated Care Corporation | 27.8% |

| Kaiser Foundation Health Plan of the Northwest | 9.5% |

| Kaiser Foundation Health Plan of Washington | 14% |

| LifeWise Health Plan of Washington | 21.3% |

| Molina Healthcare of Washington | 25.8% |

| Premera Blue Cross | 24% |

| Regence BlueCross BlueShield of Oregon | 17.4% |

| Regence BlueShield | 8.6% |

| UnitedHealthcare of Oregon | 26.4% |

| Wellpoint Washington, Inc. | 13.7% |

Source: Washington Office of the Insurance Commissioner2

It’s important to note that average rate changes apply to full-price premiums, and most enrollees do not pay full price. These subsidies change each year to keep pace with the cost of the second-lowest-cost Silver plan in each area. But starting in 2026, federal subsidies require enrollees to pay a larger share of the premium themselves (compared with what they were paying between 2021 and 2025), because Congress did not extend the federal subsidy enhancements that expired at the end of 2025.

However, Washington adopted a new premium alignment (silver loading) approach starting with the 2026 plan year — and continuing in the 2027 plan year — 7 helping to “preserve consumer affordability and stability in Washington state’s individual health insurance market.”29

Under the state’s new rules, insurers must add a 43.5% load to the premiums for on-exchange Silver plans,30 to account for the cost of cost-sharing reductions and the assumption that the only people who will select Silver plans have income that doesn’t exceed 200% FPL (meaning they’re eligible for the strongest cost-sharing reduction benefits). This has the effect of raising Silver plan premiums relative to other metal levels. This increases premium subsidies, since subsidy amounts are based on the cost of Silver-level coverage.

Stakeholders note that although Washington’s state-funded premium subsidies are smaller for 2026 than they were for 2025, and although Congress did not extend the federal subsidy enhancements, people eligible for both federal subsidies and state-funded subsidies “will continue to have access to affordable net premiums”5 due to the new premium alignment approach.

As a result of Washington’s premium alignment, Gold plan enrollment increased sharply, and Bronze plan enrollment decreased for 2026. Nationwide, there was an increase in Bronze plan selections, but that didn’t happen in Washington due to state subsidies — only available on Silver and Gold plans — and the new premium alignment approach.

For perspective, here’s an overview of how average full-price premiums have changed in Washington’s individual/family market over the years:

- 2015: Average increase of 1.9%31

- 2016: Average increase of 4.2%32

- 2017: Average increase of 13.6%33

- 2018: Average increase of 36.4%34

- 2019: Average increase of 13.6%35

- 2020: Average decrease of 3.3%36

- 2021: Average decrease of 3.2%37

- 2022: Average increase of 4.17%38

- 2023: Average increase of 8.18%39

- 2024: Average increase of 8.9%40

- 2025: Average increase of 10.7%41

- 2026: Average increase of 21%25

How many people are insured through Washington’s Marketplace?

During the open enrollment period for 2026 coverage, 290,109 people selected plans through Washington Healthplanfinder.18

Source: 2014,42 2015,43 2016,44 2017,45 2018,46 2019,47 2020,48 2021,49 2022,50 2023,51 2024,52 202553 202618

This was a drop from the record-high enrollment in 2025, but it was still higher than 2024’s enrollment, which had also been a record-high at that point.

The record high enrollments in 2024 and 2025 were due to the continued enhancement of premium subsidies under the American Rescue Plan and Inflation Reduction Act, as well as the “unwinding” of the pandemic-era Medicaid continuous coverage rule. CMS reported that more than 89,000 Washington residents transitioned from Medicaid (Apple Health) to Marketplace coverage during the “unwinding” process.54

What health insurance resources are available to Washington residents?

Washington Healthplanfinder

The state-based health insurance exchange, where individuals and families can enroll in health plans and receive subsidies based on household income. Washington Healthplanfinder is also the enrollment portal for income-based Apple Health (Medicaid) and CHIP enrollment.

Washington State Office of the Insurance Commissioner

Licenses and regulates the state’s health insurance companies, brokers, and agents. Provide assistance and information to consumers who have questions or complaints about regulated entities.

Washington Statewide Health Insurance Benefits Advisors (SHIBA)

A local service that can answer questions and provide information, counseling, and assistance related to Medicare in Washington.

Looking for more information about other options in your state?

Need help navigating health insurance options in Washington?

Explore more resources for options in WA including short-term health insurance, dental, Medicaid and Medicare.

Speak to a sales agent at a licensed insurance agency.

Footnotes

- “Open enrollment through Washington Healthplanfinder ends, with federal actions and lapsed tax credits creating uncertainty and higher costs” Washington Healthplanfinder. Jan. 24, 2026 ⤶ ⤶

- ”Thirteen health insurers request average 22.4% rate increase for 2027 individual market” Washington State Office of the Insurance Commissioner. May 26, 2026 ⤶ ⤶ ⤶ ⤶

- “Cascade Care” Washington Health Benefit Exchange. Accessed Dec. 9, 2025 ⤶

- ”Cascade Select will be available across Washington in 2025” Washington Health Benefit Exchange. Oct. 15, 2024 ⤶

- ”Final Cascade Care Savings amounts for plan year 2026 released” Washington Health Benefit Exchange. Sep. 30, 2025 ⤶ ⤶ ⤶ ⤶ ⤶

- ”Washington State also jumps on the Premium Alignment bandwagon to mitigate tax credit expiration” ACA Signups. Sep. 15, 2025 ⤶

- ”Health carrier rate development components (R 2025-02)” Washington Office of the Insurance Commissioner. Apr. 15, 2026 ⤶ ⤶

- ”Washington: State Innovation Waiver” Centers for Medicare and Medicaid Services. December 2022 ⤶

- ”2026 OEP State-Level Public Use File (ZIP)” Centers for Medicare & Medicaid Services, Accessed July 9, 2026 ⤶ ⤶

- ”Insurers seek 21.2% average rate change for 2026 individual health insurance market” Washington State Office of the Insurance Commissioner. May 27, 2025 *The above is based on the most current data available. ⤶

- ”Health Insurance for Everyone” Washington Healthplanfinder. Accessed May 28, 2026 ⤶

- ”Washington: State Innovation Waiver” Centers for Medicare & Medicaid Services. December 9, 2022. ⤶ ⤶

- ”Health Care Options for Immigrants; Deferred Action for Childhood Arrivals update” Washington Healthplanfinder. Accessed Aug. 29, 2025 ⤶

- Medicare and the Marketplace, Master FAQ. Centers for Medicare and Medicaid Services. Accessed May 28, 2026 ⤶

- Premium Tax Credit — The Basics. Internal Revenue Service. Accessed May 28, 2026 ⤶ ⤶

- Updates to frequently asked questions about the Premium Tax Credit. Internal Revenue Service. February 2024. ⤶

- “Enrollment Periods” Washington Healthplanfinder, Accessed Dec. 9, 2025 ⤶

- ”2026 Marketplace Open Enrollment Period Public Use Files” CMS.gov. April 2026 ⤶ ⤶ ⤶ ⤶ ⤶

- “Cascade Care” Washington Health Benefit Exchange, Accessed Dec. 9, 2025 ⤶

- ”Apple Health Expansion” Washington State Health Care Authority. Accessed Dec. 9, 2025 ⤶

- ”WA expanding health care options for undocumented immigrants” The Seattle Times. Mar. 11, 2024 ⤶

- ”Apple Health Expansion enrollment update – December 2025” Washington Health Care Authority. Feb. 20, 2026 ⤶ ⤶

- ”Washington Health Care Authority seeks more funding to expand Medicaid for undocumented adults” Northwest Public Broadcasting. Dec. 20, 2024 ⤶

- ”Inside Olympia: Details of the 2025-2027 biennial budget” Washington State Hospital Association. Accessed Dec. 9, 2025 ⤶

- ”Fourteen health insurers approved to sell plans in Washington’s 2026 individual health insurance market” Washington State Office of the Insurance Commissioner. Oct. 10, 2025 ⤶ ⤶

- ”Fourteen health insurers approved to sell plans in Washington’s 2026 individual health insurance market” Washington Office of the Insurance Commissioner. Oct. 10, 2025 ⤶

- “2025 Qualified Health and Dental Plan Certification” Washington Health Benefit Exchange. Sep. 12, 2024 ⤶

- ”PacificSource lays off 29, will largely pull out of Washington” Lund Report. Mar. 28, 2024 ⤶

- ”Emergency Rule: Plan Year 2026 development of uniform cost-sharing reduction factor (R 2025-01, R 2025-07)” Washington Office of the Insurance Commissioner. June 29, 2025 ⤶

- ”Rule-Making Order” Washington Insurance Commissioner. June 29, 2025 ⤶

- ”Washington slashes exchange rates, doubles plans” Healthcare Dive. August 29, 2014. ⤶

- ”Washington State: 2016 *approved* rate increases: 4.2% weighted avg. (potentially up to 5%)” ACA Signups. Aug. 27, 2015 ⤶

- ”Avg. UNSUBSIDIZED Indy Mkt Rate Hikes: 25% (49 States + DC)” ACA Signups, October 2016 ⤶

- ”2018 Rate Hikes” ACA Signups, October 2017 ⤶

- ”2019 Rate Hikes” ACA Signups, October 2018 ⤶

- ”Washington State: *Approved* 2020 ACA Exchange Premium Rate Changes: 3.3% Decrease!“Washington Office of the Insurance Commissioner, September 14, 2022 ⤶

- ”Kreidler approves average rate decrease of 3.2% for Washington’s 2021 Exchange health insurers” Washington Office of the Insurance Commissioner, September 24, 2020 ⤶

- ”Average 4.17% rate change approved for 2022 Exchange health insurance market” Washington Office of the Insurance Commissioner, September 20, 2021 ⤶

- ”12 insurers approved for 2023 Exchange health insurance market, 8.18% average rate change“Washington Office of the Insurance Commissioner, September 14, 2022 ⤶

- “Average rate increase of 8.9% approved for 2024 individual health insurance market” Washington Office of the Insurance Commissioner, September 13, 2023 ⤶

- ”Average 10.7% rate increase approved for 2025 individual health insurance market” Washington State Office of the Insurance Commissioner. Sep. 11, 2024 ⤶

- “ASPE Issue Brief (2014)” ASPE, 2015 ⤶

- “Health Insurance Marketplaces 2015 Open Enrollment Period: March Enrollment Report”, HHS.gov, 2015 ⤶

- “HEALTH INSURANCE MARKETPLACES 2016 OPEN ENROLLMENT PERIOD: FINAL ENROLLMENT REPORT” HHS.gov, 2016 ⤶

- “2017 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2017 ⤶

- “2018 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2018 ⤶

- “2019 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2019 ⤶

- “2020 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2020 ⤶

- “2021 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2021 ⤶

- “2022 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2022 ⤶

- “2023 Marketplace Open Enrollment Period Public Use Files” CMS.gov, March 2023 ⤶

- ”HEALTH INSURANCE MARKETPLACES 2024 OPEN ENROLLMENT REPORT” CMS.gov, 2024 ⤶

- “2025 Marketplace Open Enrollment Period Public Use Files” CMS.gov, May 2025 ⤶

- ”State-based Marketplace (SBM) Medicaid Unwinding Report” Centers for Medicare & Medicaid Services. Data through September 2024 ⤶