Medicare in Nebraska

Original Medicare, Medicare Advantage, Part D prescription drug, and Medigap coverage in Nebraska

Medicare enrollment in Nebraska

As of February 2026, there were 395,998 Nebraska residents with Medicare coverage.1

Most Medicare beneficiaries are eligible for coverage because they’re at least 65 years old. But younger people gain Medicare eligibility if they have end-stage renal disease (ESRD) or amyotrophic lateral sclerosis (ALS), or after they’ve been receiving disability benefits for 24 months.

Nationwide, about 9% of all Medicare beneficiaries are under 65 and eligible due to disability.2 It’s about the same in Nebraska, with 9% of the state’s Medicare population eligible due to a disability. The rest of the state’s Medicare beneficiaries are at least 65 years old.1

- Read about Medicare’s open enrollment period and other important enrollment deadlines.

- Learn how Nebraska’s Medicaid program can provide assistance to Medicare beneficiaries with limited income and assets.

Medicare Advantage plan availability and enrollment in Nebraska

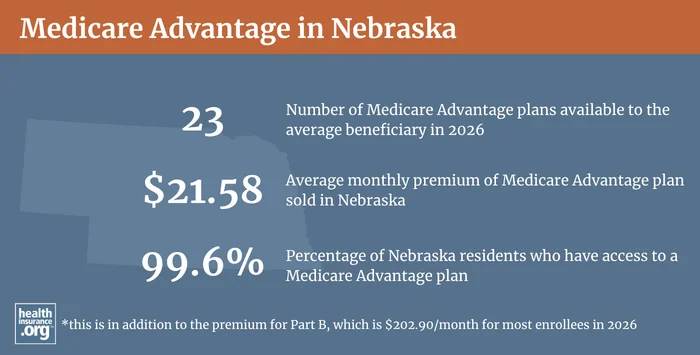

For 2026, Medicare Advantage plans are available in most areas of Nebraska, and the average Medicare beneficiary in the state can select from among 23 different Medicare Advantage plans. But there are six counties in the northwestern part of the state where Medicare Advantage plans aren’t available.3 CMS noted that 99% of Medicare beneficiaries in Nebraska would have access to Medicare Advantage plans.4 So while there continue to be some areas that don’t have these plans, the vast majority of beneficiaries can select them if that’s their choice.

As of early 2026, 135,860 Medicare beneficiaries in Nebraska were enrolled in private Medicare Advantage plans, amounting to about a third of the state’s Medicare population.1

Learn more about Medicare Advantage, Medicare’s annual open enrollment period, and the Medicare Advantage open enrollment period.

Sources: Medicare Advantage 2026 Spotlight: A First Look at Plan Offerings, KFF.org, Dec. 9, 2025; Fact Sheet: Medicare Open Enrollment for 2026, Centers for Medicare & Medicaid Services. Sep. 26, 2025

Learn about Medicare plan options in Nebraska by contacting a licensed agent.

Medicare supplement (Medigap) plan availability in Nebraska

According to the Medicare plan finder tool, 25 insurers in Nebraska offer Medigap plans in 2026.5 And according to an AHIP analysis, there were more than 168,000 Nebraska Medigap enrollees in 2023.6

Unlike other private Medicare coverage enrollment (Medicare Advantage and Medicare Part D plans), there is no annual open enrollment window for Medigap plans. Instead, federal rules provide a one-time six-month window when Medigap coverage is guaranteed issue. This window starts when a person is at least 65 and enrolled in Medicare Part B (you must be enrolled in both Part A and Part B to buy a Medigap plan).

People who aren’t yet 65 can enroll in Medicare if they’re disabled and have been receiving disability benefits for at least two years, and more than 34,000 Nebraska Medicare beneficiaries are under 65 years old.7 However, federal rules do not guarantee access to Medigap plans for people who are under 65.

The majority of the states have stepped in to ensure at least some access to private Medigap plans for disabled enrollees under the age of 65, and Nebraska joined them with legislation enacted in 2024. Starting in 2025, Nebraska Medigap insurers have been required to offer at least one plan to beneficiaries under age 65, with rates that can’t exceed 150% of the rate that would be charged if they were 65 years old.8

As of 2026, all of the Medigap carriers in Nebraska have chosen to offer Medigap Plan A to beneficiaries who are under the age of 65.9

Nebraska used to allow Medicare enrollees under the age of 65 to enroll in the state’s high-risk pool (NECHIP), but the high-risk pool ceased operations in 2023. The state’s new rule requiring at least some Medigap access for disabled beneficiaries took effect in 2025.

Disabled Medicare beneficiaries have access to the normal federally required Medigap open enrollment period when they turn 65, regardless of how long they’ve been enrolled in Original Medicare at that point. So while disabled beneficiaries can only choose Medigap Plan A while they’re under 65, they can select any plan available in their area when they turn 65. And they will be able to get the regular age-65 premiums, rather than the higher premiums that are charged when a beneficiary is under 65.

Learn what Medigap covers, who’s eligible for Medigap and when you can enroll.

Medicare Part D plan availability and enrollment in Nebraska

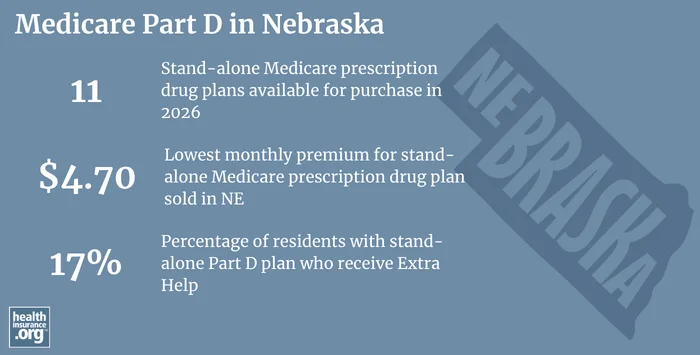

Insurers in Nebraska are offering 11 stand-alone Part D plans for 2026, with premiums that start as low as $4.70 per month.4

As of February 2026, there were 198,053 Medicare beneficiaries in Nebraska with stand-alone Medicare Part D plans.1 Another 121,966 had Medicare Part D coverage as part of their Medicare Advantage plans.1

Learn how Medicare Part D prescription drug coverage works, what it pays for, how and when to enroll.

Source: Fact Sheet: Medicare Open Enrollment for 2026, Centers for Medicare & Medicaid Services. Sep. 26, 2025

Resources for Medicare beneficiaries in Nebraska

- The Nebraska Senior Health Insurance Information Program (SHIIP) can provide assistance with a wide range of topics related to Medicare in Nebraska.

- Nebraska Medicare beneficiaries with limited income and assets may be eligible for Medicaid as well. (Nationwide, about 1 in 5 Medicare beneficiaries is also eligible for Medicaid.) You can contact the Nebraska Department of Health and Human Services to learn more about Medicaid eligibility for people who are enrolled in Medicare.

- The Nebraska Department of Insurance maintains a helpful consumer information page about Medicare supplements (Medigap), including a list of the companies that offer Medigap plans and how much they charge for a 65-year-old applicant.

Looking for more information about other options in your state?

Need help navigating health insurance options in Nebraska?

Explore more resources for options in NE including ACA coverage, short-term health insurance, dental and Medicaid.

Speak to a sales agent at a licensed insurance agency.

Footnotes

- “Medicare Monthly Enrollment – Nebraska” Centers for Medicare & Medicaid Services Data. Accessed May 2026. ⤶ ⤶ ⤶ ⤶ ⤶

- “Medicare Monthly Enrollment – U.S.” Centers for Medicare & Medicaid Services. Accessed May 2026. ⤶

- “Medicare Advantage 2026 Spotlight: A First Look at Plan Offerings” KFF.org. Dec. 9, 2025 ⤶

- “Fact Sheet: Medicare Open Enrollment for 2026” Centers for Medicare & Medicaid Services. Sep. 26, 2025 ⤶ ⤶

- “Supplement Insurance (Medigap) Plan A policies” Medicare plan comparison tool. Accessed June 1, 2026. ⤶

- “The State of Medicare Supplement Coverage” AHIP. May 2025 ⤶

- “Medicare Monthly Enrollment – Nebraska” Centers for Medicare & Medicaid Services Data. Accessed June 2026. ⤶

- “Nebraska Legislative Bill 852” BillTrack50. Enacted April 18, 2024 ⤶

- “Supplement Insurance (Medigap) Plans in Nebraska” Medicare plan comparison tool. Accessed June 1, 2026. ⤶