Medicare in North Carolina

Original Medicare, Medicare Advantage, Part D prescription drug, and Medigap coverage in North Carolina

In this article

Medicare enrollment in North Carolina

As of January 2026, there were 2,300,288 residents with Medicare in North Carolina.1 For most of them, Medicare coverage enrollment was triggered by turning 65. But more than 10% of North Carolina Medicare beneficiaries – almost 245,000 people – were under age 65 as of January 2026.1

Nationwide, there are more than 6 million people under the age of 65 who are covered by Medicare.2 This is because individuals also become eligible for Medicare after receiving Social Security disability benefits for two years or if they’ve been diagnosed with end stage renal disease or amyotrophic lateral sclerosis (ALS).

- Understand the difference between Medigap, Medicare Advantage, and Medicare Part D (including tips for picking the best coverage combination to meet your needs).

- Learn how Medicaid can provide assistance to North Carolina Medicare beneficiaries who have limited financial resources.

Medicare Advantage plan availability and enrollment in North Carolina

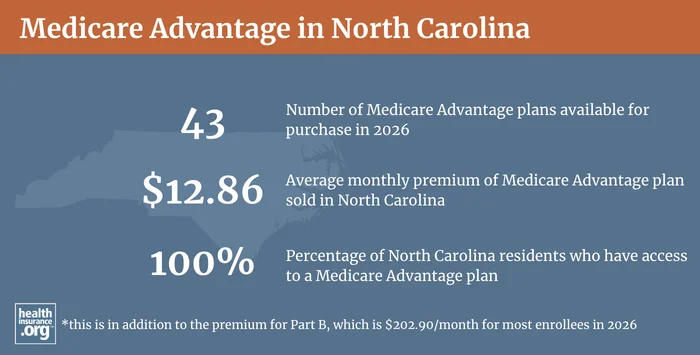

Since Medicare Advantage plans are offered by private insurers, plan availability varies from one area to another. There are Medicare Advantage plans marketed in all counties in North Carolina for 2026,3 and the average Medicare beneficiary in North Carolina can choose from among 33 Medicare Advantage plans for 2026.4

The average 2026 Medicare Advantage premium in North Carolina is $12.86/month (in addition to the premium for Part B, which is $202.90/month for most enrollees), but all Medicare beneficiaries in North Carolina have access to at least one $0-premium Medicare Advantage plan in 20255 (meaning they would only pay the Part B premium).

As of January 2026, 1,332,540 North Carolina residents were enrolled in Medicare Advantage plans while the other 967,748 Medicare beneficiaries had Original Medicare coverage.1

Learn more about Medicare Advantage, Medicare’s annual open enrollment period, and the Medicare Advantage open enrollment period.

Sources: Medicare Advantage 2026 Spotlight: A First Look at Plan Offerings, KFF.org, Dec. 9, 2025; Fact Sheet: Medicare Open Enrollment for 2026, Centers for Medicare & Medicaid Services. Sep. 26, 2025

Learn about Medicare plan options in North Carolina by contacting a licensed agent.

Medicare supplement (Medigap) enrollment and regulations in North Carolina

According to an AHIP analysis, there were 463,867 North Carolina Medicare beneficiaries enrolled in Medigap plans (also known as Medicare supplement insurance plans, or MedSupp) as of 2023.6

Medigap plans are sold by private insurers, but they’re standardized under federal rules and regulated by state laws and insurance commissioners.

Forty-eight insurers offered Medigap plans in North Carolina as of late 2025.7 The state’s plan comparison tool displays the plans based on how much they cost, to make it easy to compare the various options. Since the plan benefits are standardized (so for example, Plan G has the same benefits regardless of which insurer sells it), consumers can make their plan selection based on premiums and less tangible factors like customer service. North Carolina’s Medigap shopping guide is a useful resource for consumers.

North Carolina allows Medigap insurers to pick their own rating approach, so nearly all of the plans for sale in the state use attained-age rating,8 which means that an enrollee’s premiums will increase as they get older, regardless of how old they were when they first enrolled. The other two approaches to Medigap premiums are issue-age rating, in which premiums are based on the age the person was when they enrolled, and community rating (sometimes called “no age” rating), which means premiums don’t vary based on age; some states require one of these approaches, but North Carolina does not.

Federal rules require Medigap insurers to offer plans on a guaranteed-issue basis during an enrollee’s Medigap Open Enrollment Period, which begins when the person is at least 65 years old and enrolled in Medicare Part B. (An individual must be enrolled in Medicare Part A and Part B both to enroll in Medigap).9 Federal rules do not guarantee access to Medigap plans for people under age 65. But North Carolina is among the majority of the states that have enacted rules to ensure access to Medigap plans for disabled enrollees under age 65.

Can I get Medigap in North Carolina if I’m under 65 and disabled?

North Carolina law10 requires all Medigap insurers in the state to offer at least Plan A to people under age 65 who are enrolled in Medicare due to a disability. And if the insurer also offers either Plan C or Plan F to people who are 65 or older, they must also make that plan available to beneficiaries under age 65 who were eligible for Medicare prior to 2020.

If the insurer offers either Plan D or Plan G to people who are 65+, they must also offer that plan to people who are under 65 and eligible for Medicare. Under federal rules, as a result of the Medicare Access and CHIP Reauthorization Act of 2015 (MACRA), Medigap Plans C and F cannot be sold to people who become eligible for Medicare in 2020 or later.9

North Carolina Medicare beneficiaries under age 65 are granted a one-time six-month Medigap Open Enrollment Period that begins when they’re enrolled in Medicare Part B (or when they find out they’ve been retroactively enrolled in Part B). So they essentially have the same enrollment period as people who are turning 65, but it applies regardless of age, and it only guarantees access to Plan A and, in some cases, Plan C and Plan F or Plan D and Plan G.

But while state law in North Carolina guarantees access to Medigap plans for disabled beneficiaries under age 65, the insurers may charge significantly higher premiums for these enrollees.11 For example:12

- Medigap Plan A rates in 2026 for a person aged 55 range from $252 per month to $1,424 per month. In comparison, the same Plan A for a person aged 65 ranges in price from $94 per month to $329 per month.

- Medigap Plan G premiums in 2025 for a 55-year-old range from $419 per month to $1,346 per month, whereas a 65-year-old would pay between $102 and $387 per month for the same plans.

Disabled Medicare beneficiaries have access to another Medigap open enrollment period when they turn 65. At that point, they have access to any of the available plans (as opposed to only Plan A, D, and G when they were under 65), at the same prices as any other 65-year-old.

Medicare Part D plan availability and enrollment in North Carolina

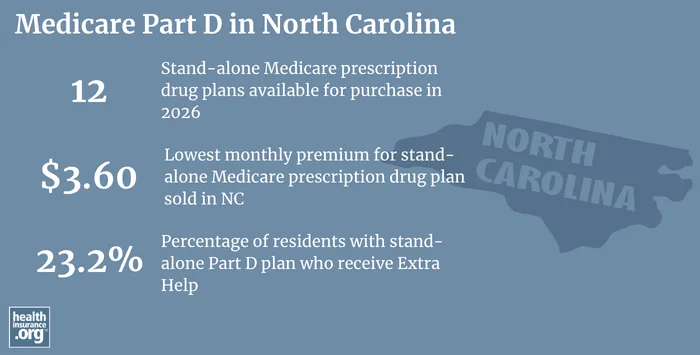

There are 12 stand-alone Medicare Part D prescription drug plans available for purchase in North Carolina for 2026, with monthly premiums starting at $3.60 per month.13

As of January 2026, 827,940 North Carolina beneficiaries were enrolled in stand-alone Medicare Part D prescription drug plans (which are called prescription drug plans or PDPs).1 Another 1,058,946 beneficiaries had Medicare Advantage plans that included integrated Medicare Part D coverage.1

Learn how Medicare Part D prescription drug coverage works, what it pays for, how and when to enroll.

Source: Fact Sheet: Medicare Open Enrollment for 2026, Centers for Medicare & Medicaid Services. Sep. 26, 2025

Resources for Medicare beneficiaries in North Carolina

Do you have questions about Medicare eligibility in North Carolina or need help selecting the best options for your specific situation? These resources provide free assistance and information.

- You can contact North Carolina’s Seniors’ Health Insurance Information Program (SHIIP) with questions related to Medicare enrollment in North Carolina. Visit the website or call 855-408-1212.

- North Carolina’s Senior Medicare Patrol Program (NCSMP) strives to “reduce Medicare error, fraud, and abuse” by educating Medicare beneficiaries and their caregivers about Medicare benefits, statements, explanations of benefits, etc.

Looking for more information about other options in your state?

Need help navigating health insurance options in North carolina?

Explore more resources for options in NC including ACA coverage, short-term health insurance, dental and Medicaid.

Speak to a sales agent at a licensed insurance agency.

Footnotes

- “Medicare Monthly Enrollment – North Carolina” Centers for Medicare & Medicaid Services Data. Accessed April 2026. ⤶ ⤶ ⤶ ⤶ ⤶

- “Medicare Monthly Enrollment – US” Centers for Medicare & Medicaid Services Data. Accessed, April 2026. ⤶

- “Medicare Open Enrollment in North Carolina, 2026” (Page 100) CMS.gov. Sep. 26, 2025 ⤶

- “Medicare Advantage 2026 Spotlight: First Look” KFF.org Dec. 9, 2025 ⤶

- “Medicare Open Enrollment 2026” CMS.gov. Sep. 26, 2025 ⤶

- “The State of Medicare Supplement Coverage” AHIP. May 2025 ⤶

- “Medigap Company Names Sold in NC” North Carolina Department of Insurance. Sep. 18, 2025 ⤶

- “Medicare Supplement Premium Comparison Database” North Carolina Department of Insurance, SHIIP. Accessed May 2, 2026 ⤶

- “Choosing a Medigap Policy” Medicare.gov. Accessed May 2, 2026 ⤶ ⤶

- “Chapter 58. Insurance” North Carolina General Assembly. Accessed April 30, 2026 ⤶

- “Medicare Supplement (Medigap) Plans” North Carolina Department of Insurance, SHIIP. Accessed May 2, 2026 ⤶

- “Supplement Insurance (Medigap) plans in North Carolina” Medicare.gov. Accessed May 2, 2026 ⤶

- “Fact Sheet: Medicare Open Enrollment for 2026” Centers for Medicare & Medicaid Services. Sep. 26, 2025 ⤶