Find Wyoming Health Insurance Marketplace Coverage for 2026

Compare ACA plans and check subsidy savings from a licensed third-party health insurance agency.

Wyoming Health Insurance Marketplace Guide

We created this guide, including the FAQs below, to help you understand the health coverage options and possible financial assistance available to you and your family in Wyoming.

Wyoming uses the federally-facilitated health insurance exchange enrollment platform, HealthCare.gov, commonly known as the Marketplace, for enrollment in Affordable Care Act (ACA) plans.

The Wyoming Marketplace provides access to health insurance products from two private insurers for 2026. There were three in 2025, but Mountain Health CO-OP, which had offered coverage in Wyoming since 2021, exited the state at the end of 2025. See more details below about premium changes and insurer participation for 2026.

Depending on your income and other circumstances, you may qualify for financial assistance when you buy your coverage through the Wyoming Marketplace. Even after federal subsidy enhancements expired at the end of 2025, most enrollees in Wyoming qualify for advance premium tax credits (premium subsidies), and some also qualify for cost-sharing reductions that lower their out-of-pocket medical costs.1

*Values displayed by this tool are from data generated by CMS and reflect 2026 Marketplace health plans purchased in each state. The values returned are averages based on the plans purchased by consumers of each selected state: subsidy and premium values vary based on factors such as zip code, age, household size, and income.

Wyoming Marketplace quick facts

Frequently asked questions about health insurance in Wyoming

Who can buy health insurance through the Marketplace in Wyoming?

To qualify for health coverage through the Marketplace in Wyoming, you must:4

- Live in Wyoming

- Be lawfully present in the United States

- Not be incarcerated

- Not be enrolled in Medicare

Eligibility for financial assistance in the form of premium subsidies and cost-sharing reductions (CSR) depends on your income and how it compares with the cost of the second-lowest-cost Silver plan in your area – which depends on your age and location. (See more details below about premium subsidies and CSR benefits.). In addition, to qualify for financial assistance with your ACA plan you must:

- Not have access to affordable health coverage through your employer. If your employer offers coverage but you feel it’s too expensive, you can use our Employer Health Plan Affordability Calculator to see if you might qualify for premium subsidies in the Marketplace.

- Not be eligible for Medicaid or CHIP.

- Not be eligible for premium-free Medicare Part A.5

- If married, file a joint tax return with your spouse.6

- Not be able to be claimed by someone else as a tax dependent.6

When can I enroll in an ACA-compliant plan in Wyoming?

In Wyoming, the open enrollment period for 2026 individual market coverage ended on January 15, 2026.7

The open enrollment period will become shorter, however, starting in the fall of 2026. The deadline to enroll will be December 15, and all plans selected during open enrollment will take effect January 1. There will no longer be an opportunity to sign up after December 15 without a special enrollment period.

Outside of open enrollment, a special enrollment period is necessary to enroll or make changes to your coverage.

Most special enrollment periods are triggered by a qualifying life event, such as giving birth or losing other health coverage. But Native Americans can enroll year-round.

If you have questions about open enrollment, you can learn more in our comprehensive guide to open enrollment. We also have a comprehensive guide to special enrollment periods.

How do I enroll in a Marketplace plan in Wyoming?

To enroll in an ACA Marketplace plan in Wyoming, you can:

- Visit HealthCare.gov – the federally-facilitated health insurance Marketplace that’s used in Wyoming. Here you will find an online platform to compare plans, determine whether you’re eligible for financial assistance, and enroll in the plan that best meets your needs.

- Purchase individual and family health coverage with the help of an insurance agent or broker, a Navigator or certified application counselor, or an approved enhanced direct enrollment entity.8

You can also call HealthCare.gov’s contact center by dialing 1-800-318-2596 (TTY: 1-855-889-4325). The call center is available 24 hours a day, seven days a week, but it’s closed on holidays.

How can I find affordable health insurance in Wyoming?

Wyoming residents can use the federally-facilitated enrollment platform – HealthCare.gov – to shop for individual and family health plans.

Before Marketplace subsidies are applied, Wyoming has among the most expensive individual market coverage in the country; only West Virginia has higher average premiums.9 But that means Marketplace subsidies in Wyoming are also among the largest in the country, ensuring that coverage is affordable for most enrollees.

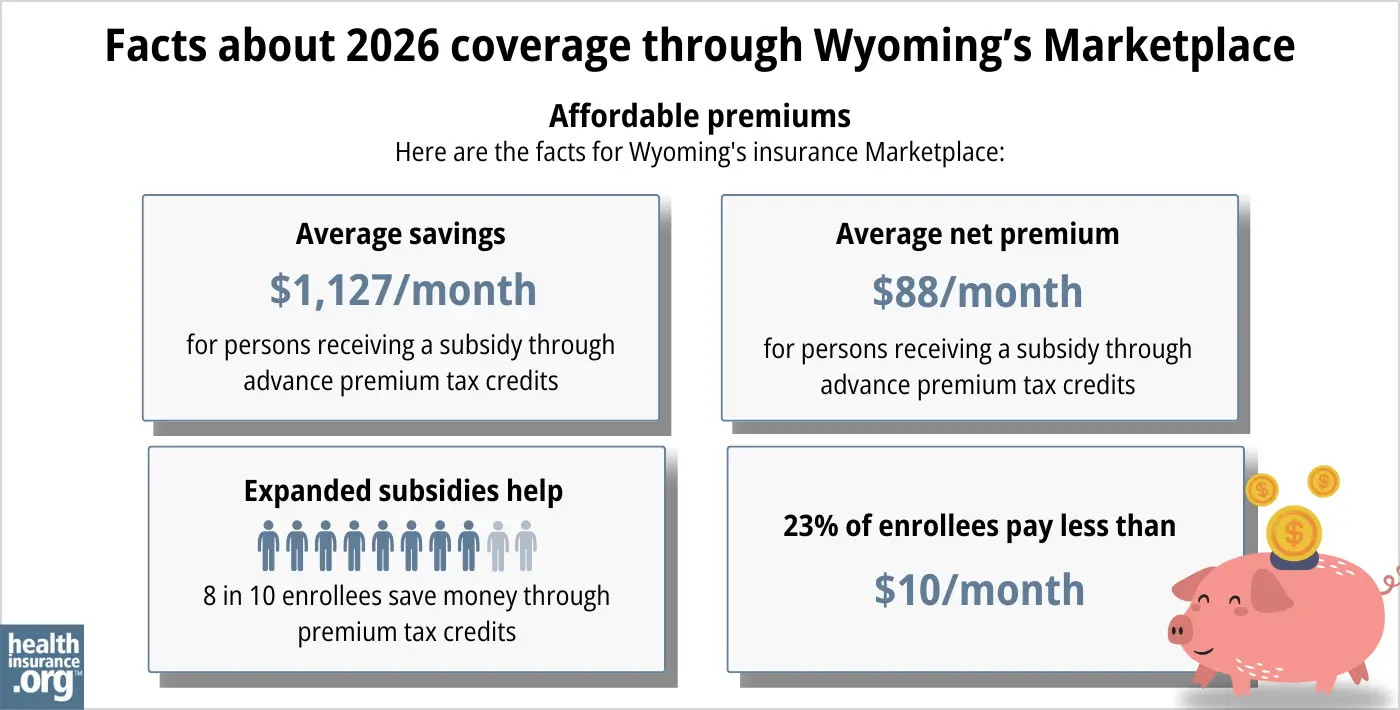

During the open enrollment period for 2026 coverage, 87% of the people who enrolled in plans through the Wyoming Marketplace were eligible for premium subsidies (premium tax credit). The average subsidy amount was about $1,127/month, leaving the average subsidy-eligible enrolling paying only about $88/month for their coverage.9

But because Wyoming has such high full-price premiums, the return of the “subsidy cliff” in 2026 (due to the failure of Congress to extend federal subsidy enhancements) was particularly significant in Wyoming. For people who lost their subsidy altogether because their income was over 400% of the federal poverty level, full-price premiums are particularly expensive in Wyoming.

In addition to the premium subsidies, Marketplace enrollees with household incomes up to 250% of the federal poverty level also qualify for cost-sharing reductions (CSR) that reduce the out-of-pocket expenses on Silver-level plans.10

Between the premium subsidies and cost-sharing reductions, you may find that an ACA plan is the cheapest health insurance option for you.

Source: CMS.gov9

Wyoming has not yet expanded Medicaid eligibility under the ACA. The state legislature has considered Medicaid expansion numerous times over the years, but the legislation has never been successful.

As a result, there is a coverage gap in the state: Non-disabled adults under age 65 who don’t have children are ineligible for both Medicaid and Marketplace subsidies if their income is below the poverty level.

How many insurers offer Marketplace coverage in Wyoming?

Two insurers offer coverage through Wyoming’s exchange (Marketplace) for 2026:

- Blue Cross Blue Shield of Wyoming

- UnitedHealthcare

A third carrier, Mountain Health CO-OP, offered plans in 2025 but exited the Wyoming market at the end of 2025,11 due in large part to Congress’s failure to extend the premium subsidy enhancements that expired at the end of 2025.12

Mountain Health CO-OP is one of just three remaining ACA-created CO-OPs in the country. The CO-OP began in Montana, but expanded into Wyoming as of the 2021 plan year (and Idaho as of the 2015 plan year). Their plans continue to be available in Idaho and Montana in 2026.

There were roughly 9,600 Wyoming residents with Mountain Health CO-OP plans in 2025.13 All of them had to select new coverage for 2026.

UnitedHealthcare was new to Wyoming’s Marketplace for 2025,14 and continues to offer coverage in 2026.

Are Marketplace health insurance premiums increasing in Wyoming?

The following average rate increases were approved for Wyoming’s Marketplace insurers for 2026, before subsidies are applied.15

Wyoming’s ACA Marketplace Plan 2026 APPROVED Rate Increases by Insurance Company |

|

|---|---|

| Issuer | Percent Increase |

| Blue Cross Blue Shield of Wyoming | 25.39% |

| Mountain Health CO-OP/Montana Health CO-OP | Exited market |

| UnitedHealthcare | 30.07% |

Source: RateReview.HealthCare.gov15

Wyoming is one of three states that do not have an effective rate review program, so the proposed rates and plans are reviewed by the federal government (CMS) instead of state regulators.16

If we don’t count Mountain Health CO-OP’s enrollees (since they had to select new plans from one of the other two carriers for 2026), the weighted average rate increase for 2026 was 25.9%, before subsidies are applied.17

When we talk about overall average rate changes, keep in mind that they only reflect how full-price premiums change from one year to the next. They don’t account for subsidies or for the fact that a person’s rates will increase each year based on their age, even if their insurer doesn’t change its average premiums at all.

Most enrollees in Wyoming’s exchange receive premium subsidies, which offset the majority of the cost of their coverage.9 But because Congress didn’t extend the subsidy enhancements that had been in place since 2021, subsidies don’t cover as much of the premium cost in 2026. Some people lost access to subsidies altogether. For most enrollees, the expiration of the federal subsidy enhancements had a larger impact than the overall rate increases described above.

Here’s a summary of how average pre-subsidy premiums have changed over the years in Wyoming’s individual/family health insurance market (note that these numbers are unweighted averages for years with multiple carriers, as enrollment numbers were often redacted):

- 2015: Average increase of 5%18

- 2016: Average increase of 6%19 (only one participating insurer)

- 2017: Average increase of 7.4%20

- 2018: Average increase of 55%21 (Largely due to elimination of federal funding for CSR)

- 2019: Average decrease of 0.25%22

- 2020: Average increase of 1.6%23

- 2021: Average decrease of 10%24 (second insurer joined the exchange)

- 2022: Average decrease of 4%25

- 2023: Average increase of 18.5%26

- 2024: Average increase of 0.3%27

- 2025: Average increase of 10%28

How many people in Wyoming are insured through the Marketplace?

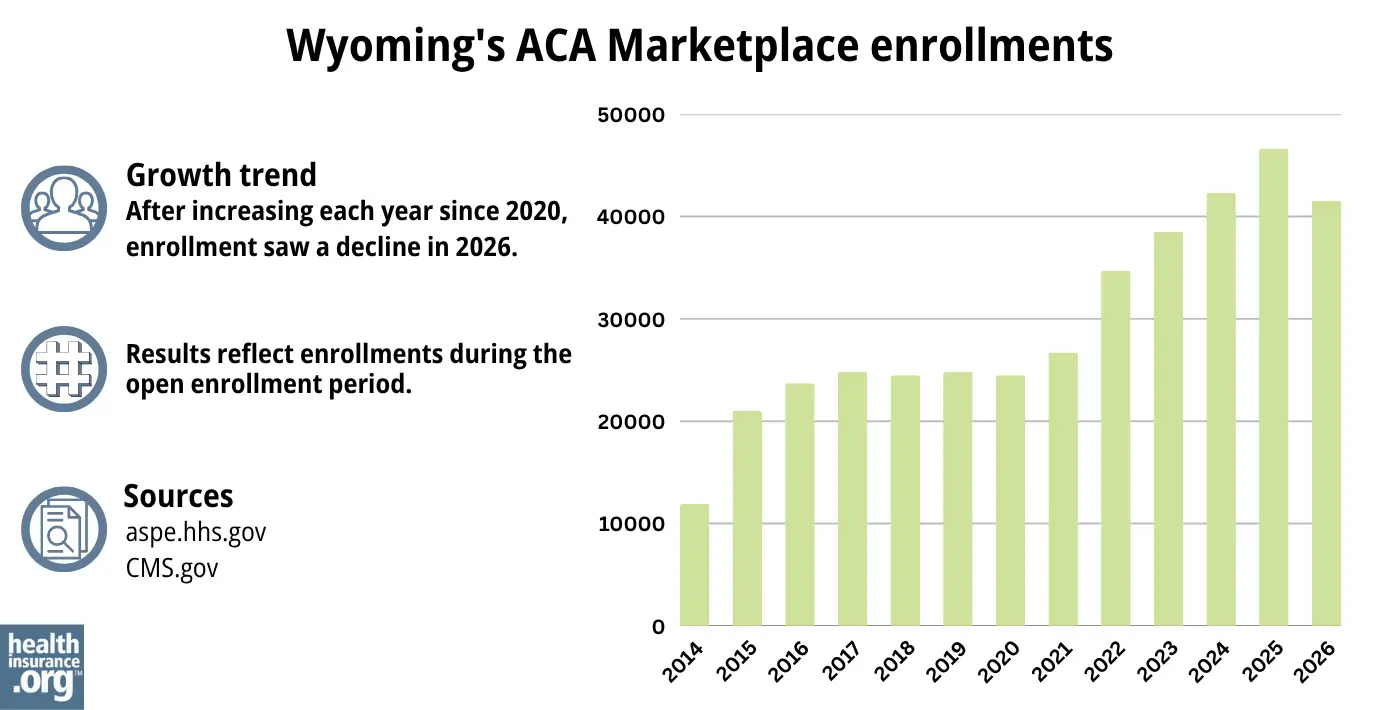

During the open enrollment period for 2026 coverage, 41,545 people enrolled in private plans through the Wyoming ACA Marketplace.29 This was lower than enrollment had been in 2024 or 2025 (see chart below).

The surge in enrollment from 2021 through 2025 was due in part to the American Rescue Plan (ARP), which made ACA’s premium subsidies more substantial. Under the ARP’s rules – extended through 2025 by the Inflation Reduction Act – subsidies were larger and more widely available than they used to be.30 But as noted above, those subsidy enhancements expired at the end of 2025, resulting in lower Marketplace enrollment for 2026.

The enrollment increase in 2024 and 2025 was also driven partly by the “unwinding” of the pandemic-era Medicaid continuous coverage rule. CMS reported that 5,864 Wyoming residents transitioned from Medicaid to a Marketplace plan during the year-long unwinding period.31

Source: 2014,32 2015,33 2016,34 2017,35 2018,36 2019,37 2020,38 2021,39 2022,40 2023,41 2024,42 202543 202644

What health insurance resources are available to Wyoming residents?

HealthCare.gov

800-318-2596

Wyoming Insurance Department

Provides consumer protection and support to Wyoming residents by investigating consumer complaints and resolving issues on insurance matters.

(307) 777-7401 / Toll Free: 1-800-438-5768 / [email protected]

State Exchange Profile: Wyoming

The Henry J. Kaiser Family Foundation overview of Wyoming’s progress toward creating a state health insurance exchange.

Looking for more information about other options in your state?

Need help navigating health insurance options in Wyoming?

Explore more resources for options in WY including short-term health insurance, dental, Medicaid and Medicare.

Speak to a sales agent at a licensed insurance agency.

Footnotes

- ”2026 Marketplace Open Enrollment Period Public Use Files” Centers for Medicare & Medicaid Services. Mar. 27, 2026 ⤶

- ”2026 OEP State-Level Public Use File (ZIP)” Centers for Medicare & Medicaid Services, Accessed July 9, 2026 ⤶ ⤶

- ”Your Health Coverage with us in Wyoming is ending on December 31, 2025” Mountain Health CO-OP. Accessed Aug. 18, 2025 *The above is based on the most current data available. ⤶

- “A quick guide to the Health Insurance Marketplace®” HealthCare.gov, Accessed Apr. 14, 2026 ⤶

- Medicare and the Marketplace, Master FAQ. Centers for Medicare and Medicaid Services. Accessed Apr. 14, 2026 ⤶

- Premium Tax Credit — The Basics. Internal Revenue Service. Accessed Apr. 14, 2026 ⤶ ⤶

- “When can you get health insurance?” HealthCare.gov. Accessed Apr. 14, 2026 ⤶

- “Entities Approved to Use Enhanced Direct Enrollment” CMS.gov, Dec. 8, 2025 ⤶

- “2026 Marketplace Open Enrollment Period Public Use Files” CMS.gov, March 2026 ⤶ ⤶ ⤶ ⤶

- ”APTC and CSR Basics” Centers for Medicare & Medicaid Services. Oct. 2025 ⤶

- ”Your Health Coverage with us in Wyoming is ending on December 31, 2025” Mountain Health CO-OP. Accessed Aug. 18, 2025 ⤶

- ”Mountain Health Co-Op insurance provider to cease coverage for Wyoming residents” Insurance News Net. Aug. 15, 2025 ⤶

- ”Wyoming: Mountain Health Co-Op pulling the plug for 2026 just weeks after filings go live” ACA Signups. Aug. 14, 2025 ⤶

- ”New 2025 Individual Exchange plans and prior authorization information” UnitedHealthcare. Oct. 1, 2024 ⤶

- ”Wyoming Rate Review Submissions” RateReview.HealthCare.gov, Accessed Dec. 5, 2025 ⤶ ⤶

- ”State Effective Rate Review Programs” CMS.gov. Accessed Dec. 5, 2025 ⤶

- ”2026 Final Gross Rate Changes – Wyoming: +25.9% (updated)” ACA Signups. Nov. 2, 2025 ⤶

- ”Analysis Finds No Nationwide Increase in Health Insurance Marketplace Premiums” The Commonwealth Fund. December 2014. ⤶

- ”UPDATE: Wyoming: Requested 2016 Avg. Rate Hikes: 10.2%” ACA Signups. Sept. 15, 2015; However, WINhealth and Time Insurance exited the market at the end of 2015 and only BCBSWY plans continued into 2015 ⤶

- ”Avg. UNSUBSIDIZED Indy Mkt Rate Hikes: 25% (49 States + DC)” ACA Signups. October 2016. ⤶

- ”Alabama, Hawaii, Missouri, Wyoming: Wrapping Up The 2018 Rate Hike Project W/An Assist From Avalere” ACA Signups. Oct 27, 2017 ⤶

- ”2019 Rate Hikes” ACA Signups. October 2018. ⤶

- ”2020 Rate Changes” ACA Signups. October 2019. ⤶

- ”Wyoming: Preliminary Avg. 2021 #ACA Rates: 10.0% *Decrease*” ACA Signups. Oct. 14, 2020 ⤶

- ”Wyoming: Preliminary Avg. 2022 #ACA Rate Changes (Unweighted): -4.1% Indy Market; +1.0% Sm. Group” ACA Signups. Oct. 13, 2021 ⤶

- ”Wyoming: (Preliminary) Avg. Unsubsidized 2023 #ACA Rate Changes: +18.5%” ACA Signups. Aug. 3, 2022 ⤶

- ”Wyoming: *Final* Avg. Unsubsidized 2024 #ACA Rate Changes: +0.3% (Unweighted; Updated)” ACA Signups. Nov. 8, 2023 ⤶

- ”Wyoming: Preliminary avg. unsubsidized 2025 #ACA rate changes: +10.0% (unweighted)” ACA Signups. Sep. 19, 2024 ⤶

- ”Marketplace 2026 Open Enrollment Period Report: National Snapshot” CMS.gov, March 2026 ⤶

- “Health Insurance Marketplaces 2023 Open Enrollment Report” CMS.gov, Accessed August 2023 ⤶

- ”HealthCare.gov Marketplace Medicaid Unwinding Report” CMS.gov. Data through April 2024. Accessed Jan. 31, 2025 ⤶

- “ASPE Issue Brief (2014)” ASPE, 2015 ⤶

- “Health Insurance Marketplaces 2015 Open Enrollment Period: March Enrollment Report”, HHS.gov, 2015 ⤶

- “HEALTH INSURANCE MARKETPLACES 2016 OPEN ENROLLMENT PERIOD: FINAL ENROLLMENT REPORT” HHS.gov, 2016 ⤶

- “2017 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2017 ⤶

- “2018 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2018 ⤶

- “2019 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2019 ⤶

- “2020 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2020 ⤶

- “2021 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2021 ⤶

- “2022 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2022 ⤶

- “2023 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2023 ⤶

- ”HEALTH INSURANCE MARKETPLACES 2024 OPEN ENROLLMENT REPORT” CMS.gov, 2024 ⤶

- “2025 Marketplace Open Enrollment Period Public Use Files” CMS.gov, May 2025 ⤶

- ”2026 Marketplace Open Enrollment Period Public Use Files” CMS.gov. March 2026 ⤶