HMO vs PPO vs POS vs EPO: What’s the difference?

The type of managed care your health plan falls under affects your healthcare costs and plan benefits – including access to medical providers

In this article

Among the many factors to consider when you’re shopping for individual health insurance coverage is the type of managed care plan. HMO vs PPO vs EPO vs POS: To decide which works best for your situation, you need to understand the differences between the options and how they can affect your budget and access to medical providers.

What is managed care? And why do health plans have managed care designations?

Managed care is a medical delivery system that attempts to manage the quality and cost of medical services that individuals receive. Each type of managed care limits, to varying degrees,

- the number of providers from which a patient can choose,

- whether the patient has to use a primary care physician, and

- whether out-of-network care is covered under the plan.

Some managed care systems attempt to improve health quality, by emphasizing the prevention of disease.1

The vast majority of privately insured individuals are in some form of managed care plan. Among those with employer-sponsored insurance, which covers almost half the U.S. population,2 less than 1% of enrollees were in indemnity (non-managed-care) plans.3 And 100% of the plans available nationwide in the health insurance Marketplaces are managed care plans.4

Note: The Trump administration has finalized a rule change for 2028 and future years that will allow "non-network plans" to be sold in the Marketplace if the plans can show "that they ensure a sufficient choice of providers that accept the non-network plan's benefit amount as payment in full, and reasonable and timely access to ECPs (essential community providers) that accept the plan's benefit amount as payment in full."5 This could potentially change the landscape for Marketplace plans, although it remains to be seen whether insurers will be interested in offering non-network plans.

Even in the Medicaid and Medicare systems, managed care plays a significant role: About 85% of the individuals enrolled in Medicaid were covered under private Medicaid managed care plans as of 2024.6 And more than half of Medicare beneficiaries were enrolled in private Medicare Advantage plans as of 20267 – a percentage that has been steadily growing over the past decade.8 (Medicare Advantage plans are managed care plans).9

Four types of managed care

As you’re selecting a health plan, you may notice that the plan is labeled as an HMO, PPO, EPO, or POS. These are categories of managed care, which is how virtually all modern health insurance is organized. Here’s what those acronyms stand for:

- HMO – Health Maintenance Organization

- PPO – Preferred Provider Organization

- EPO – Exclusive Provider Organization

- POS – Point of Service

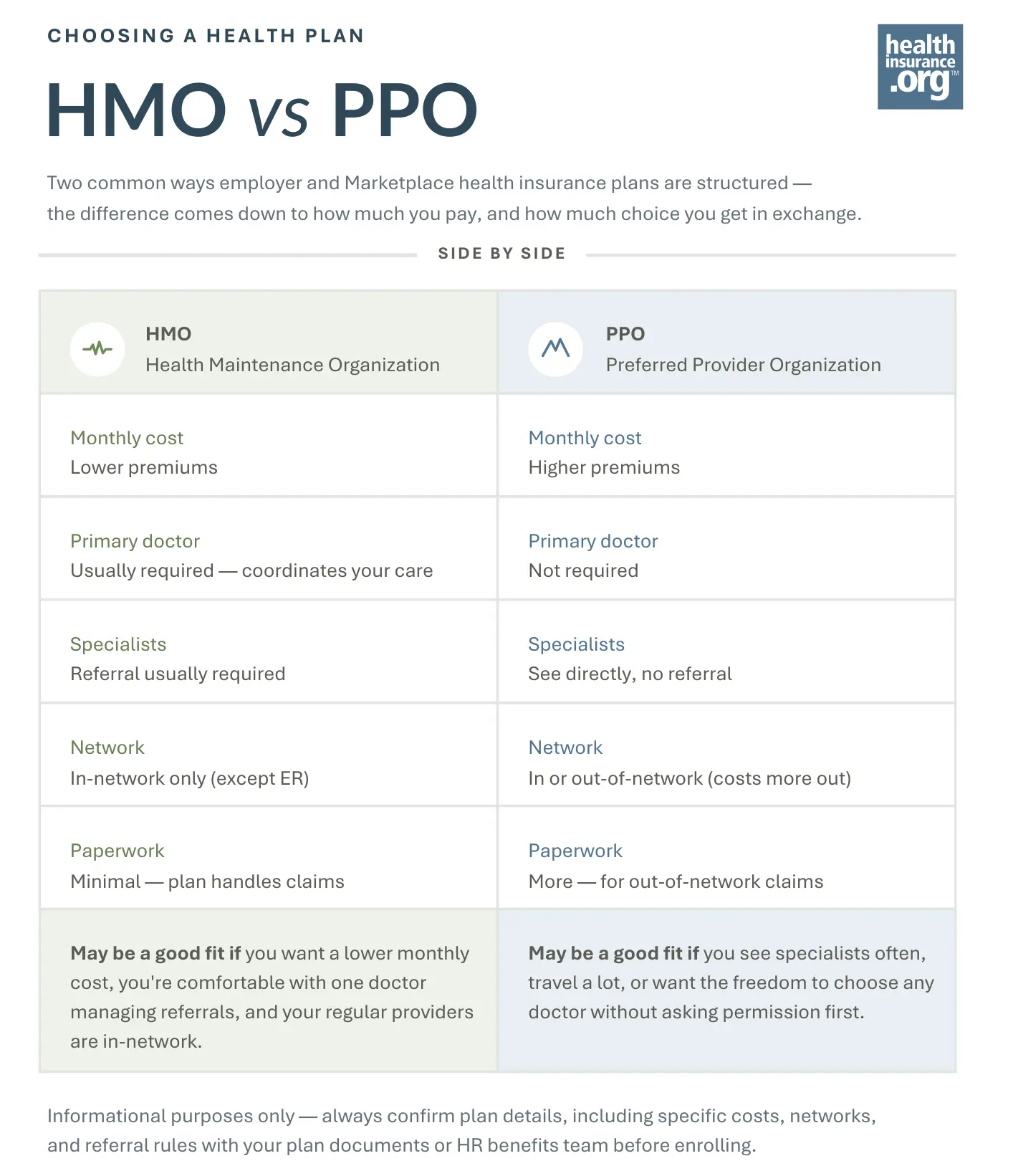

What is an HMO?

If your coverage is a Health Maintenance Organization plan, you’ll generally only have coverage if you use a medical provider who is in-network with the plan, except for emergencies. You'll likely need to choose a primary care physician (PCP) or your insurer will pick one for you. That person will serve as a "gatekeeper," meaning that you'll generally need to see your primary care physician for a referral before your plan will cover care provided by a specialist.

However, some modern HMOs do not require a PCP referral to see a specialist (these are often labeled as "open access" HMOs), so you’ll want to understand the details of the specific plans you’re considering.10

As of 2026, 46% of Marketplace plans are HMOs.11

What is a PPO?

Under a Preferred Provider Organization plan, policyholders receive discounted prices from in-network healthcare providers partnered with the PPO, which means that the provider will write off a portion of their billed amount, under the terms of the network agreement with the health plan. A referral to a specialist is generally not required, which means policyholders can see a specialist without seeing a primary care doctor first.

PPOs will cover out-of-network care, but the deductible and other out-of-pocket expenses are typically higher (often significantly so) for out-of-network care. So policyholders who use a provider outside of the PPO plan’s network typically pay more for the medical care. And they are also subject to balance billing from the out-of-network medical provider, which means that the provider can bill the patient for the full amount of their charges, without having to write off any of the bill (note that the No Surprises Act prohibits balance billing in emergencies and in situations where an out-of-network provider is working at an in-network facility12).

As of 2026, only 15% of Marketplace plans are PPOs.11

What is an EPO?

An Exclusive Provider Organization plan only covers in-network care (except in emergency situations), but policyholders will generally not need to pick a primary care physician, nor will they need to get a referral to see a specialist. So the policyholder can choose to see any specialist in the plan’s network without needing to see a primary care doctor first. Since out-of-network care is not covered, the patient will pay full price for out-of-network services that aren’t subject to the No Surprises Act.

As of 2026, 33% of Marketplace plans are EPOs.11

What is a POS?

A Point of Service plan typically (but not always) requires policyholders to choose a primary care physician and get referrals to see a specialist. These plans do cover out-of-network care after a referral from the PCP, but out-of-pocket costs can be significantly higher for out-of-network care than for in-network care, and the out-of-network provider can balance bill the policyholder unless it’s a situation in which the No Surprises Act protections are applicable. POS plans are not common.

As of 2026, only 7% of Marketplace plans are POS plans.11

Managed care considerations (HMO, EPO, PPO and POS) |

||||

|---|---|---|---|---|

| HMO | EPO | PPO | POS | |

| Does it cover out-of-network services? |

No (In emergencies only) |

No (In emergencies only) |

Yes | Yes |

| Do you need a referral from a primary care doctor to see a specialist? |

Usually | No | No | Usually |

| Availability in the Marketplace11 |

About 46% of Marketplace plans |

About 33% of Marketplace plans |

About 15% of Marketplace plans |

About 7% of Marketplace plans |

What’s the difference between an HMO and a PPO (and other types of managed care)?

When it comes to the differences between the types of managed care, it typically boils down to two factors: access to providers, and out-of-network medical care.

Access to providers

All HMO, PPO, EPO, and POS plans have networks of medical providers (doctors, hospitals, etc.) that have a contract with the health plan in which the carrier agrees to accept a negotiated price for the services they offer. Some plans will only pay for non-emergency care if you receive care from an in-network provider, while other plans may cover some of the bill if you see an out-of-network provider.

You’ll often see simple comparison charts that show the “rules” for the different types of managed care. In a nutshell, these summaries generally say that HMOs and POS plans require a referral from a primary care doctor in order to see a specialist, while PPOs and EPOs do not, and that PPOs and POS plans cover out-of-network care, while HMOs and EPOs do not. They will also often tend to say that HMOs have lower premiums, lower deductibles, and smaller provider networks, while PPOs have higher premiums, higher deductibles, and broader networks.

In reality, these distinctions tend to be blurry, and these types of plan management have evolved over time. For example, some HMO and POS plans do not require a referral to see a specialist (as noted above, you may see these types of coverage described as "open access"). And while it’s often true that employer-sponsored HMOs tend to have lower deductibles and premiums and potentially smaller networks, that does not hold true in the individual/family (self-purchased) market. Read the details of any policy you are considering carefully.

Out-of-network care

It is generally true that EPO and HMO plans will not cover out-of-network care unless it’s an emergency, while PPO and POS plans will provide some out-of-network coverage. But policyholders should always look at the out-of-pocket costs for out-of-network care because they will typically be substantially higher than the out-of-pocket costs for in-network care.13

The ACA requires health plans to cap out-of-pocket costs for essential health benefits obtained from an in-network provider. The upper limit for this cap is $10,600 in 202614 and $12,000 in 2027, although some Bronze plans will be allowed to have even higher limits starting in 2027.15 But there are no limits on how high out-of-network costs can be, even if the plan provides out-of-network coverage.

For perspective, the weighted average in-network deductible for plans purchased in the health insurance Marketplaces in 2026 was just under $3,000, although it was considerably lower for enrollees in plans with built-in cost-sharing reductions16 (for eligible enrollees, cost-sharing reductions lower out-of-pocket costs and increase the actuarial value of a plan, but they don't affect out-of-network cost-sharing, for plans that provide out-of-network coverage).17

So although PPO and POS plans do generally cover out-of-network care, you might find that you only get a benefit from that if your out-of-network costs are particularly high. And some plans with out-of-network coverage do not put any cap on total out-of-pocket costs for out-of-network care, as there is no requirement that they do so.

Availability of managed care options varies by location

It’s important to keep in mind that you may not have access to multiple types of managed care plans. If you get your coverage from an employer, your options will be limited to the plans that your employer offers. And if you buy your own health insurance, your options will depend on what’s offered by insurers in your area.

For example, there are some areas of the country where the only plans available through the Marketplace are HMOs (or HMOs and EPOs). As of 2026, more than eight out of ten Marketplace plans nationwide are either HMOs or EPOs.11

Overall, PPOs are much less common in the individual market than they used to be, while HMOs and EPOs have gained considerable market share over the last several years.18

For 2026 coverage, across the 30 states that used HealthCare.gov, approximately:11

- 46% of plans were HMOs

- 33% of plans were EPOs

- 15% of plans were PPOs

- 7% of plans were POSs

What might you consider when buying an HMO, EPO, PPO or POS plan?

Depending on where you live, you might not have access to multiple types of managed care plans in the Marketplace. But if you do, here are several factors to keep in mind when you’re selecting a plan:

1. Make sure you understand your plan’s coverage of out-of-network care

Although a PPO or POS plan will cover out-of-network care, it’s important to understand how that works. Be aware of the deductible (which is likely to be quite high) and the out-of-pocket exposure (which could be unlimited without a cap).

Also be aware of the fact that an out-of-network provider can and will balance bill you unless it’s an emergency or an out-of-network provider working at an in-network facility. (Here’s how the No Surprises Act protects consumers from surprise balance bills in those situations).

So although your health plan may pay for some of the service (assuming you’ve met the out-of-network cost-sharing requirements), the provider can bill you for the portion of their charges above the amount the health plan paid, unless it's a situation covered by the No Surprises Act. This means your total out-of-pocket costs for the out-of-network care might be significantly higher than just the out-of-network copay/deductible/coinsurance listed in your plan documents.

And there’s a good chance out-of-network care isn’t applicable to your coverage at all, given that the large majority of individual/family health plans are HMOs and EPOs,11 and thus do not provide out-of-network coverage unless it’s an emergency.

2. Narrowness of networks varies

All four types of managed care plans can have broad, narrow, or mid-size provider networks. Don’t assume anything. Instead, you’ll want to actively compare the provider networks of each plan you’re considering, to see whether your specific providers are in-network.

If you don’t currently have any providers, it’s a good idea to see whether each plan you’re considering has in-network hospitals and medical offices that would be convenient if you end up needing medical care. It’s also a good idea to utilize the preventive care benefits that are provided with zero cost-sharing on all ACA-compliant plans.19 This will generally require finding a primary care provider who can help you obtain preventive services.

3. Managed care is different in the individual market

Individual/family plans aren’t the same as employer-sponsored plans, and that includes the provider networks and managed care rules. You may have had an employer-sponsored plan offered or administered by a particular insurer, but don’t assume that individual/family plans from that insurer will have the same provider network or managed care rules. (For example, whether or not a referral is required.)

4. Referral requirements vary

Although you may have heard that HMOs and POS plans require a referral from a primary care physician in order to see a specialist, that’s not necessarily true. Again, you’ll need to check the specifics of the plans you’re considering.

(And there are pros and cons to referral requirements. On one hand, they mean an additional office visit, which adds to your costs. But on the other hand, your PCP can help to ensure that you’re seeing the correct specialist, and can coordinate the care you receive from multiple specialists.)

Referrals are sometimes confused with prior authorizations (pre-authorizations), but those are two different concepts. A referral comes from a primary care physician, whereas prior authorization has to be obtained from the health plan itself. Health plans can set their own rules in terms of which services require prior authorization. All four types of managed care plans – HMOs, PPOs, EPOs, and POS plans – can and do require prior authorization for various services. But there’s a lot of variation from one plan to another in terms of what services need prior authorization.

So it’s important to understand your plan’s rules, and to ensure that your doctor has your health plan information so that they can submit prior authorization requests on your behalf. And if in doubt, it’s best to contact your health plan before any non-emergency service is scheduled, to make sure you know whether prior authorization is necessary, and if so, whether it has been granted.

Confusion over what is and isn’t managed care

If you’ve read this far, you may be wondering why a health savings account (HSA) and a high-deductible health plan (HDHP) aren’t listed here. It’s common to see these acronyms in articles that compare PPO, EPO, HMO, and POS plans – and that leads many consumers to assume that an HSA or HDHP is a form of managed care plan. But they are not.

HSA-qualified high-deductible health plans (HDHPs) allow enrollees to contribute pre-tax money to an HSA. (You cannot contribute to an HSA unless you have active coverage under an HDHP.) And HDHPs must conform to specific IRS rules (or be Bronze or Catastrophic plans obtained in the individual market).20

The IRS sets minimum deductibles and maximum out-of-pocket limits (which are lower than what the Department of Health and Human Services sets for other plans), and limits the services that the plan can pay for before the deductible is met (the regular IRS rules for HDHPs do not apply to Bronze or Catastrophic plans, as those are now HDHPs regardless of plan design).

However, an HDHP will also be either a PPO, an EPO, an HMO, or a POS plan. The HDHP designation means that the plan conforms to the IRS rules for HSA-qualified plans. And the HMO, PPO, EPO, or POS designation describes the plan’s approach to managed care.

Learn more about HSA-qualified high-deductible health plans (HDHPs).

Footnotes

- “Care Management Program: How Your Healthcare System Can Improve Patient Outcomes” WelkinHealth.com, Accessed Jul. 28, 2026 ⤶

- "Health Insurance Coverage of the Total Population" KFF.org. Accessed Mar. 24, 2026 ⤶

- “Employer Health Benefits 2025 Annual Survey” p. 10, KFF.org, October 22, 2025 ⤶

- “The individual health insurance market in 2023” McKinsey.com, Apr. 11, 2023. And "Health insurance plan & network types: HMOs, PPOs, and more" HealthCare.gov. Accessed July 28, 2026 ⤶

- "Patient Protection and Affordable Care Act, HHS Notice of Benefit and Payment Parameters for 2027; and Basic Health Program" Centers for Medicare & Medicaid Services. May 20, 2026 ⤶

- “2024 Medicaid Managed Care Enrollment Summary” Medicaid.gov. Updated Feb. 11, 2026 ⤶

- “Medicare Monthly Enrollment, April 2026” CMS.gov. Accessed July 28, 2026 ⤶

- “Medicare Advantage in 2026: Enrollment Update and Key Trends” KFF.org, June 5, 2026 ⤶

- “Managed Care” Centers for Disease Control and Prevention. National Center for Health Statistics. Accessed Jul. 28, 2026 ⤶

- Examples: “Pathway Essentials – Quick Reference Guide Anthem’s New Network” Anthem. And "Health Maintenance Organization (HMO) Plans" Cigna. Accessed Mar. 24, 2026 ⤶

- "QHP Landscape PY2026 Individual Medical" HHS.gov. Accessed July 28, 2026 ⤶ ⤶ ⤶ ⤶ ⤶ ⤶ ⤶ ⤶

- “Ending Surprise Medical Bills” Centers for Medicare and Medicaid Services. Accessed Mar. 24, 2026 ⤶

- “What happens if I need care from a doctor who isn’t in my plan’s network?” KFF.org, Accessed October 2023 ⤶

- “Out-of-Pocket Maximum/Limit” HealthCare.gov Glossary. Accessed Feb. 17, 2025 ⤶

- "Patient Protection and Affordable Care Act, HHS Notice of Benefit and Payment Parameters for 2027; and Basic Health Program" Centers for Medicare & Medicaid Services. May 20, 2026 ⤶

- "Deductibles in ACA Marketplace Plans, 2014-2026" KFF.org. Nov. 6, 2025 ⤶

- “Patient Protection and Affordable Care Act; Actuarial Value Calculator Methodology” U.S. Department of Health and Human Services. Accessed July 28, 2026 ⤶

- “The individual health insurance market in 2023” McKinsey.com, Apr. 11, 2023 ⤶

- “Health Benefits and Coverage, Preventive Health Services” HealthCare.gov, Accessed Mar. 24, 2026 ⤶

- "Notice 2026-5, Expanded Availability of Health Savings Accounts under the One, Big, Beautiful Bill Act (OBBBA)" Internal Revenue Service. Accessed Mar. 24, 2026 ⤶