Medicare in Montana

Original Medicare, Medicare Advantage, Part D prescription drug, and Medigap coverage in Montana

Medicare enrollment in Montana

As of February 2026, there were 270,312 Montana residents with Medicare coverage.1

In most cases, Medicare eligibility starts when a person turns 65. But Medicare also provides coverage for disabled Americans under age 65, once they have been receiving disability benefits for 24 months or have end-stage renal disease (ESRD) or amyotrophic lateral sclerosis (ALS). Nationwide, about 9% of Medicare beneficiaries are under age 65;2 in Montana, it’s about 8%.1

- Read about Medicare’s open enrollment period and other important enrollment deadlines.

- Learn how Montana’s Medicaid program can provide assistance to Medicare beneficiaries with limited income and assets.

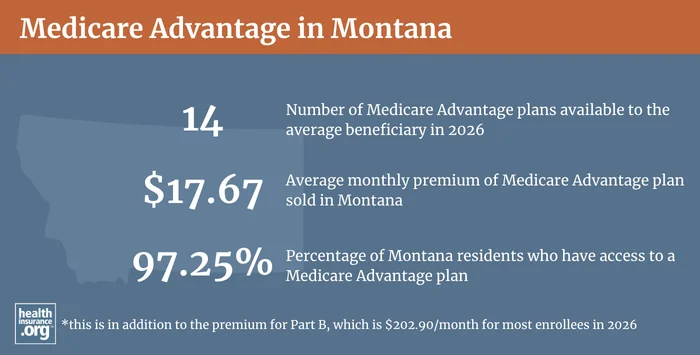

Medicare Advantage plan availability and enrollment in Montana

Most areas in Montana have Medicare Advantage plans available in 2026, but there are six counties that do not. However, the average Medicare beneficiary in Montana can choose from among 14 Medicare Advantage plans in 2026.3

As of February 2026, there were 80,720 beneficiaries of Medicare in Montana who had Medicare Advantage coverage enrollment.1

About 70% (189,592) of the state’s Medicare beneficiaries have coverage under Original Medicare.1 Nationwide, 51% of Medicare beneficiaries were enrolled in private Medicare Advantage plans as of February 2026,2 but this percentage was much lower in Montana.

Learn more about Medicare Advantage, Medicare’s annual open enrollment period, and the Medicare Advantage open enrollment period.

Sources: Medicare Advantage 2026 Spotlight: A First Look at Plan Offerings, KFF.org, Dec. 9, 2025; Fact Sheet: Medicare Open Enrollment for 2026, Centers for Medicare & Medicaid Services. Sep. 26, 2025

Learn about Medicare plan options in Montana by contacting a licensed agent.

Medicare supplement (Medigap) plan availability in Montana

According to an AHIP analysis, there were 100,634 Montana Medicare beneficiaries with Medigap coverage as of 2024.4

As of 2026, there were 24 insurers offering Medigap plans in Montana.5

Federal rules do not require Medigap insurers to offer plans to Medicare beneficiaries under age 65 who are eligible for Medicare due to a disability. Montana began requiring Medigap insurers to offer coverage to disabled Medicare beneficiaries starting in late 2013, although they’re allowed to charge significantly higher premiums for under-65 enrollees.5

For example, the 2026 premium for Medigap Plan A (which must be offered by all Medigap insurers) ranges from $109/month to $344/month for a 65-year-old female in Montana.5 But if she’s 55 instead, the Plan A options range in price from $157/month to $1,146/month.5

Disabled Medicare beneficiaries also have access to the normal Medigap open enrollment period when they turn 65. At that point, they can select from among any of the available Medigap plans, with lower premiums that apply to people who are aging onto Medicare when they turn 65.

Learn what Medigap covers, who’s eligible for Medigap and when you can enroll.

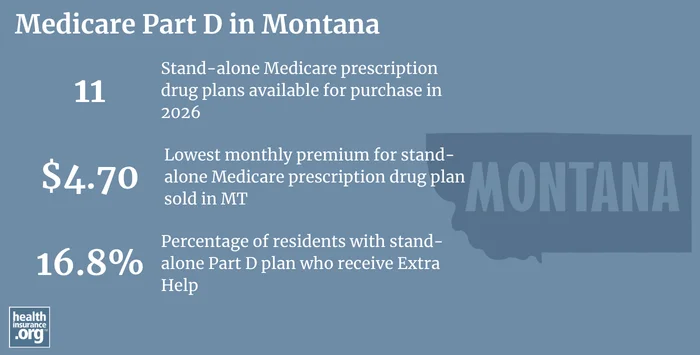

Medicare Part D plan availability and enrollment in Montana

There were 11 stand-alone Medicare Part D prescription drug plans for sale in Montana in 2026, with premiums that started at $4.70 per month.6

As of February 2026, there were 134,253 Montana Medicare beneficiaries (nearly half of the state’s total Medicare population) with stand-alone Part D plans.1 Another 72,904 Montana residents had Medicare Advantage plans that included integrated Medicare Part D prescription drug coverage.1

Learn how Medicare Part D prescription drug coverage works, what it pays for, how and when to enroll.

Source: Fact Sheet: Medicare Open Enrollment for 2026, Centers for Medicare & Medicaid Services. Sep. 26, 2025

Resources for Medicare beneficiaries in Montana

Need help filing for Medicare benefits? Got questions about Medicare eligibility in Montana?

- You can contact the Montana State Health and Insurance Information Program with questions related to Medicare in Montana.

- The Montana Commissioner of Securities and Insurance maintains a Medicare page with FAQs and a link to the federal Medigap plan comparison tool.

- The American Council on Aging has a useful guide to Medicaid eligibility in Montana for seniors in need of long-term care (which is not covered by Medicare).

- The Medicare Rights Center maintains a comprehensive national website and staffs a call center with helpful people who can provide a variety of assistance with Medicare-related questions.

Looking for more information about other options in your state?

Need help navigating health insurance options in Montana?

Explore more resources for options in MT including ACA coverage, short-term health insurance, dental and Medicaid.

Speak to a sales agent at a licensed insurance agency.

Footnotes

- “Medicare Monthly Enrollment – Montana” Centers for Medicare & Medicaid Services Data. Accessed June 2026. ⤶ ⤶ ⤶ ⤶ ⤶ ⤶

- “Medicare Monthly Enrollment – US” Centers for Medicare & Medicaid Services Data. Accessed June 2026. ⤶ ⤶

- “Medicare Advantage 2026 Spotlight: First Look” KFF.org. Dec. 9, 2025 ⤶

- “The State of Medicare Supplement Coverage” AHIP. Apr. 2026 ⤶

- “Supplement Insurance (Medigap) plans in Montana” Medicare.gov. Accessed June 4, 2026 ⤶ ⤶ ⤶ ⤶

- “Fact Sheet: Medicare Open Enrollment for 2026” Centers for Medicare & Medicaid Services. Sep. 26, 2025 ⤶