Find Hawaii Health Insurance Marketplace Coverage for 2026

Compare ACA plans and check subsidy savings from a licensed third-party health insurance agency.

Hawaii Health Insurance Marketplace Guide

Hawaii utilizes a federally-facilitated health insurance Marketplace, which means residents enroll through HealthCare.gov, where two private insurers offer individual/family health plans for Hawaii residents. The Hawaii Insurance Division oversees the plans sold in the exchange.

The approved rates for 2026 amounted to an overall weighted average increase of about 12%, before subsidies are applied. For 2027, the carriers have proposed another round of similar rate increases (details below). Most enrollees get subsidies that offset a significant portion of their premiums, and the subsidy amounts change each year to keep pace with the cost of the benchmark Silver plan.

But starting in 2026, the subsidies cover a smaller share of total premiums and available to fewer people after Congress failed to extend the subsidy enhancements that had been in place since 2021. As a result, net premiums increased significantly in 2026, and enrollment decreased (details below).

For many people, an Affordable Care Act (ACA) Marketplace plan – called Obamacare or an exchange plan – may be a cost-effective choice. This guide, including the FAQs below, is designed to help you understand how Hawaii health insurance options work, including the financial assistance that may be available to you through Hawaii’s health insurance Marketplace.

(In 2014 and 2015, Hawaii ran its own exchange, but transitioned to HealthCare.gov in the fall of 2015 and has continued to use the federally-facilitated platform ever since.)

*Values displayed by this tool are from data generated by CMS and reflect 2026 Marketplace health plans purchased in each state. The values returned are averages based on the plans purchased by consumers of each selected state: subsidy and premium values vary based on factors such as zip code, age, household size, and income.

Hawaii Marketplace quick facts

Frequently asked questions about health insurance in Hawaii

Who can buy Marketplace health insurance in Hawaii?

Virtually all residents of Hawaii are eligible to buy Marketplace health insurance with the following exceptions:3

- People who are not legally in the U.S.

- People already enrolled in Medicare

- People who are incarcerated

But eligibility for financial assistance in the Marketplace is a bit more involved. Eligibility for premium subsidies depends on how the cost of coverage in your area compares with your household income.

And to be eligible for subsidies you must not be eligible for Hawaii Med-QUEST (Medicaid/CHIP), premium-free Medicare Part A,4 or an employer’s plan that’s considered affordable and comprehensive.

Most Marketplace enrollees do qualify for premium subsidies, even after the “subsidy cliff” returned in 2026. During the open enrollment period for 2026 coverage, 71% of Hawaii Marketplace enrollees qualified for premium subsidies.5

When can I enroll in an ACA-compliant plan in Hawaii?

The next open enrollment period for individual and family health coverage in Hawaii starts on November 1, 2026, for coverage effective on January 1, 2027.

A federal rule change called for a shorter open enrollment period starting in the fall of 2026, with an end date of December 15. But a judge vacated this rule change in June 2026.6 The ruling could be appealed, or open enrollment could continue until January 15 as it did in recent years. Enrollees should pay close attention to deadlines communicated by the exchange as open enrollment approaches.

After open enrollment, you can sign up for or make changes to individual market coverage if you qualify for a special enrollment period (SEP). To be eligible for a SEP, you’ll usually need a qualifying life event. But American Indians and Alaska Natives can enroll anytime.

People eligible for Medicaid/CHIP (Med-QUEST in Hawaii) can enroll in that coverage anytime.

How do I enroll in a Marketplace plan in Hawaii?

If you qualify for an ACA Marketplace plan, there are a variety of ways you can sign up, either during open enrollment or during a special enrollment period:

- Enroll online via HealthCare.gov.

- Enroll by phone at (800) 318-2596.

- Enroll in person, over the phone, or online with the help of an agent/broker, Navigator, certified application counselor, or an approved enhanced direct enrollment entity.7

How can I find affordable health insurance in Hawaii?

Hawaii’s uninsured rate has long been lower than the national average, due in large part to the state’s Prepaid Health Care Law, which has been in effect for nearly half a century.8

Under this law, Hawaii’s employers must provide coverage to employees who work at least 20 hours per week, and the employee’s portion of the premiums can’t be more than 1.5% of their gross wages. So employer-sponsored health coverage is more accessible in Hawaii than it is in most of the rest of the country.

(A note about small group health insurance: Hawaii was the first state to receive approval for a 1332 waiver, which allowed Hawaii to no longer have a SHOP exchange.9 Small businesses in Hawaii purchase small group health plans directly from the insurers that sell these plans.)

But for those who aren’t eligible for an employer’s health plan or Medicare, coverage is available through the Marketplace (HealthCare.gov) or Med-QUEST (Medicaid/CHIP).

ACA Marketplace plans (on HealthCare.gov)

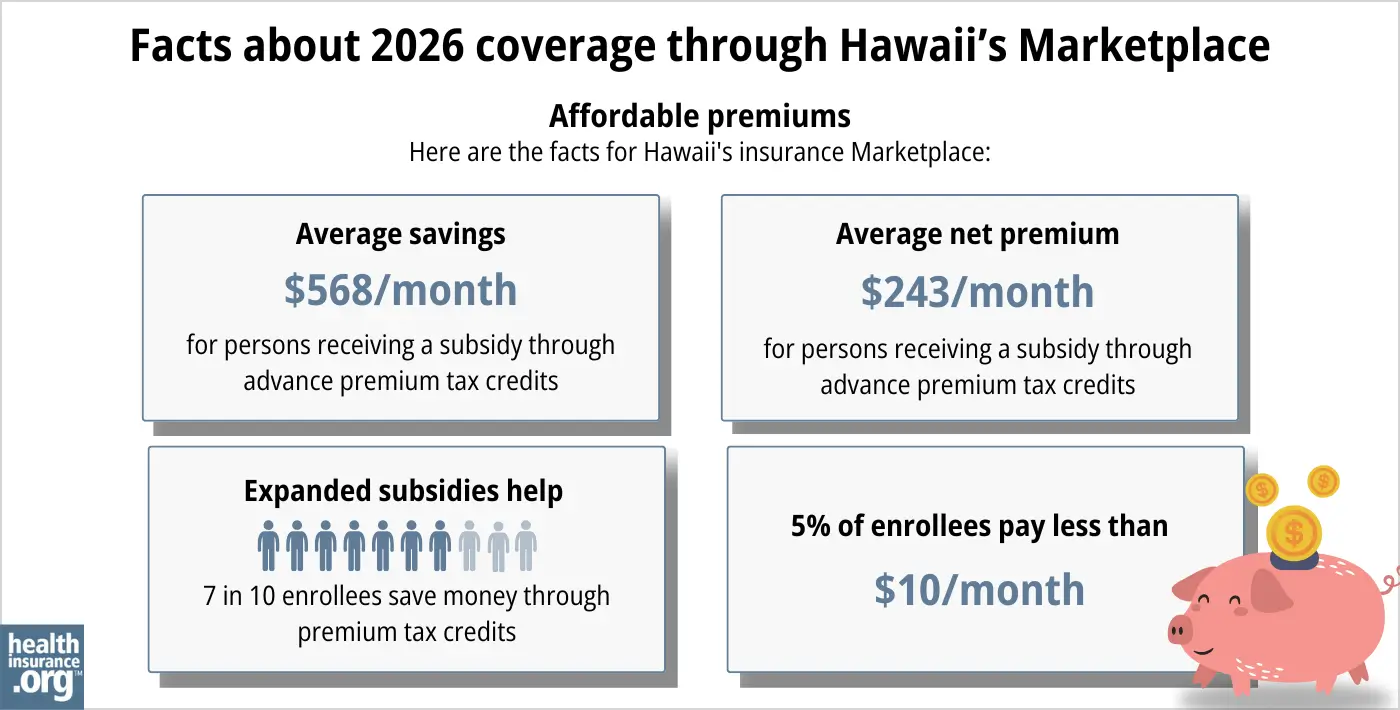

- 71% of the people who enrolled through the Hawaii Marketplace during the open enrollment period for 2026 coverage were eligible for premium subsidies (advance premium tax credits, or APTC). This means they didn’t have to pay the full cost of their coverage.

- For the 2026 enrollees who qualified for premium subsidies, the average subsidy amount was $568/month, bringing their average net premium to $243/month. Even accounting for the enrollees who paid full price, the average net premium paid by all enrollees was $372/month.5

- For 2026, most people are still eligible for premium subsidies, but the subsidies don’t cover as much of enrollees’ total premiums, and are available to fewer people. This is because federal subsidy enhancements were allowed to expire at the end of 2025.

If your income is no more than 250% of the federal poverty level, you may qualify for cost-sharing reductions (CSR) to reduce your deductibles and out-of-pocket expenses, as long as you select a silver plan through the Marketplace.10

- As of 2026, about 22% of Hawaii Marketplace enrollees were receiving CSR benefits.5

Source: CMS.gov5

Medicaid

Hawaiians may find affordable coverage through Medicaid (Med-QUEST) if eligible.

How many insurers offer Marketplace coverage in Hawaii?

Two private insurance companies offer individual/family health coverage through Hawaii’s health insurance Marketplace:11

- Hawaii Medical Service Association (HMSA)

- Kaiser Foundation Health Plan, Inc.

Are Marketplace health insurance premiums increasing in Hawaii?

According to Hawaii SERFF filings, the following average pre-subsidy rate changes have been proposed by Hawaii’s Marketplace insurers for 202712

Hawaii’s ACA Marketplace Plan 2027 PROPOSED Rate Increases by Insurance Company |

|

|---|---|

| Issuer | Percent Increase |

| Hawaii Medical Service Association (HMSA) | 13.3% |

| Kaiser Foundation Health Plan, Inc. | 9% |

Source: Hawaii SERFF12

According to its filings, HMSA has about 19,000 enrollees in 2026, although Kaiser’s filing doesn’t include its enrollment numbers (the year before, Kaiser had 10,439).13

As is always the case, these average proposed premium changes are based on full-price premiums, but the majority of enrollees are eligible for subsidies and thus do not pay full price. However, coverage became less affordable in 2026, due to the expiration of federal subsidy enhancements at the end of 2025.

For perspective, here’s a summary of how average pre-subsidy premiums for ACA-compliant individual/family plans have changed each year in Hawaii:

How many people are insured through Hawaii’s Marketplace?

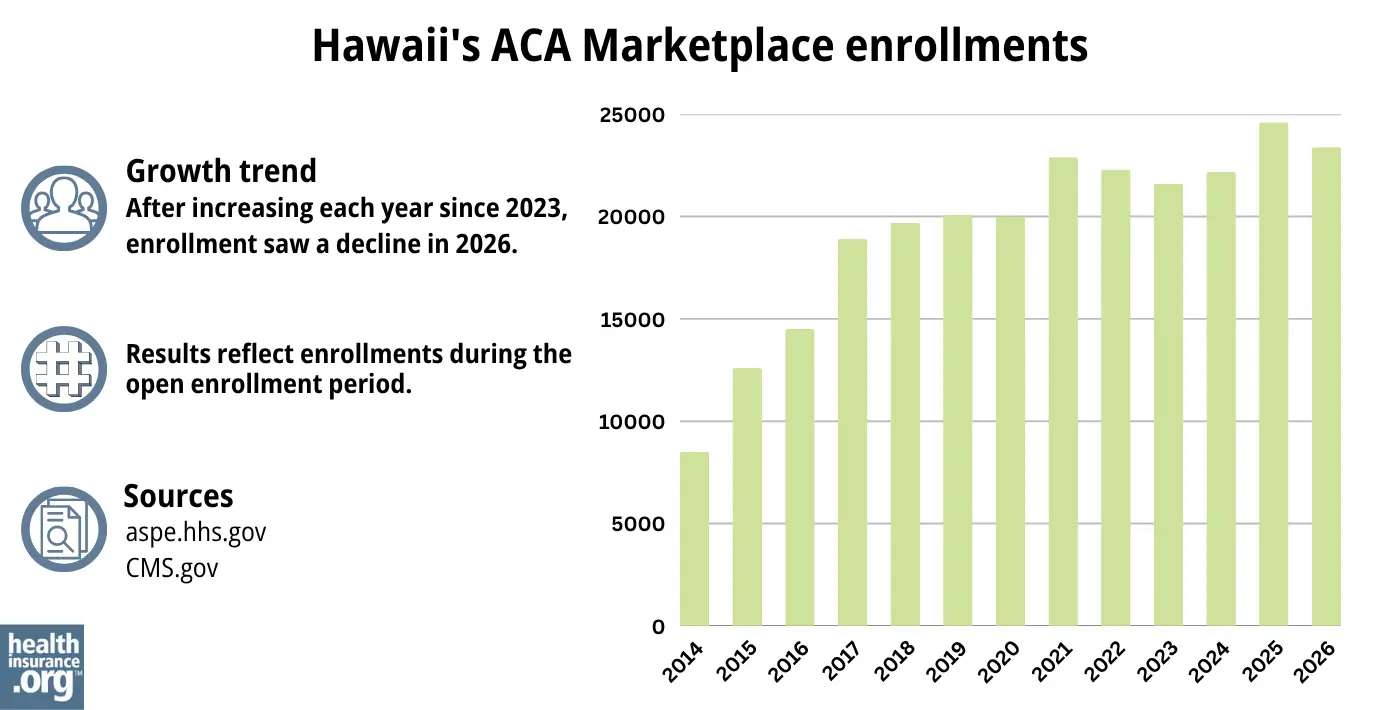

23,380 people selected coverage through the Hawaii exchange during the open enrollment period for 2026 coverage.5

This was down from the record high the year before, when 24,606 people enrolled during the open enrollment period for 2025 coverage.26

Although nationwide Marketplace enrollment had reached new record highs in 2022, 2023, 2024,27 and again in 2025, Hawaii didn’t exceed its 2021 enrollment until 2025.

The drop-off in enrollment in 2026 is not surprising, given the expiration of federal subsidy enhancements at the end of 2025, and the resulting sharp increase in after-subsidy premiums.

Here’s a summary of how enrollment has changed over time in Hawaii’s Marketplace:

Source: 2014,28 2015,29 2016,30 2017,31 2018,32 2019,33 2020,34 2021,35 2022,36 2023,37 2024,38 202539 20265

What health insurance resources are available to Hawaii residents?

HealthCare.gov

This is the ACA Marketplace, where you can enroll in a health insurance plan online. You may also get help by calling (800) 318-2596.

Hawaii’s Insurance Division of the Department of Commerce and Consumer Affairs

Licenses and regulates health insurers, agents, and brokers. They also handle consumer questions and complaints about insurance.

Legal Aid Society of Hawaii

The Navigator organization funded by the federal government in Hawaii.

Hawaii Medicaid (Med-QUEST)

This program provides health coverage for eligible residents.

Hawaii Prepaid Health Care Law information

This law helps ensure that many workers in Hawaii have access to health coverage through their jobs.

Looking for more information about other options in your state?

Need help navigating health insurance options in Hawaii?

Explore more resources for options in HI including short-term health insurance, dental, Medicaid and Medicare.

Speak to a sales agent at a licensed insurance agency.

Footnotes

- ”2026 OEP State-Level Public Use File (ZIP)” Centers for Medicare & Medicaid Services, Accessed July 9, 2026 ⤶ ⤶

- ”Hawaii Rate Review Submissions” HealthCare.gov, Accessed Sep. 16, 2025 *The above is based on the most current data available. ⤶

- ”A quick guide to the Health Insurance Marketplace” HealthCare.gov ⤶

- Medicare and the Marketplace, Master FAQ. Centers for Medicare and Medicaid Services. Accessed Feb. 3, 2025 ⤶

- ”2026 Marketplace Open Enrollment Period Public Use Files” CMS.gov. April 2026 ⤶ ⤶ ⤶ ⤶ ⤶ ⤶

- ”City of Columbus et al. v. Kennedy et al. (Columbus I)” O’Neill Institute Health Care Litigation Tracker. Provision vacated June 12, 2026 ⤶

- “Entities Approved to Use Enhanced Direct Enrollment” CMS.gov, Apr. 7, 2026 ⤶

- ”About Prepaid Health Care” State of Hawaii, Disability Compensation Division. Accessed Sep. 16, 2025 ⤶

- ”Hawaii Section 1332 Waiver Extension” Centers for Medicare and Medicaid Services. December 10, 2021. ⤶

- “Federal Poverty Level (FPL)” HealthCare.gov, 2023 ⤶

- ”Hawaii Rate Review Submissions” HealthCare.gov, Accessed Feb. 3, 2026 ⤶

- ”Hawaii SERFF Filings” (Tracking numbers KAHA-134973969 and HMSA-134976042) Accessed June 29, 2026 ⤶ ⤶

- ”Hawaii SERFF Filings” Accessed Sep. 16, 2025 ⤶

- ”Hawaii: Final 2015 QHP Rate Increase: 7.8%; SHOP Plans *Drop* 3.5%” ACA Signups. November 13, 2024 ⤶

- ”FINAL PROJECTION: 2016 Weighted Avg. Rate Increases: 12-13% Nationally” ACA Signups. October 15, 2015. ⤶

- ”Avg. UNSUBSIDIZED Indy Mkt Rate Hikes: 25% (49 States + DC)” ACA Signups. August 14, 2016. ⤶

- ”2018 Rate Hikes” ACA Signups. ⤶

- ”Hawaii: APPROVED 2019 #ACA rate hikes: 5.3% increase” ACA Signups. October 10, 2018 ⤶

- ”2020 Rate Changes” ACA Signups ⤶

- ”Hawaii SERFF Filings” Accessed September 2023 ⤶

- ”2022 Rate Changes” ACA Signups. ⤶

- ”UPDATED: FINAL Unsubsidized 2023 Premiums: +6.2% Across All 50 States +DC” ACA Signups. ⤶

- ”Hawaii: *Final* avg. unsubsidized 2024 #ACA rate changes: +8.8% (updated)” ACA Signups. Nov. 2, 2023 ⤶

- ”Hawaii: *Final* avg. unsubsidized 2025 #ACA rate changes: +6.7% (updated)” ACA Signups. Sep. 19, 2025 ⤶

- ”Hawaii SERFF Filings” (HMSA had 21,945 enrollees in 2025, and Kaiser had 10,439). Accessed Sep. 16, 2025 ⤶

- ”Marketplace 2025 Open Enrollment Period Report: National Snapshot” Centers for Medicare & Medicaid Services. Jan. 17, 2025 ⤶

- ”Another Year of Record ACA Marketplace Signups, Driven in Part by Medicaid Unwinding and Enhanced Subsidies” KFF.org. Jan. 24, 2024 ⤶

- “ASPE Issue Brief (2014)” ASPE, 2015 ⤶

- “Health Insurance Marketplaces 2015 Open Enrollment Period: March Enrollment Report”, HHS.gov, 2015 ⤶

- “HEALTH INSURANCE MARKETPLACES 2016 OPEN ENROLLMENT PERIOD: FINAL ENROLLMENT REPORT” HHS.gov, 2016 ⤶

- “2017 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2017 ⤶

- “2018 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2018 ⤶

- “2019 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2019 ⤶

- “2020 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2020 ⤶

- “2021 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2021 ⤶

- “2022 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2022 ⤶

- “Health Insurance Marketplaces 2023 Open Enrollment Report” CMS.gov, 2023 ⤶

- ”HEALTH INSURANCE MARKETPLACES 2024 OPEN ENROLLMENT REPORT” CMS.gov, 2024 ⤶

- “2025 Marketplace Open Enrollment Period Public Use Files” CMS.gov, May 2025 ⤶