Texas Marketplace health insurance in 2026

Compare ACA plans and check subsidy savings from a third-party insurance agency.

Texas ACA Marketplace quick facts

Texas health insurance Marketplace guide

This guide, including the FAQs below, was developed to assist you in choosing the right health insurance in Texas for you and your family. The coverage options found in Texas’s ACA Marketplace may be a good choice for many consumers. Texas uses the federally-facilitated health insurance exchange (Marketplace), HealthCare.gov, for residents to purchase its ACA Marketplace plans.

The Marketplace provides access to health insurance products from numerous private insurers (coverage areas vary from one insurer to another; most areas of the state have plans available from multiple insurers, but there are some counties in north-central Texas where only a single insurer offers 2025 Marketplace coverage).3

For 2026, one new insurer is joining the Texas Marketplace, and one existing insurer is leaving the market (details below), so there will continue to be 16 participating insurers.

Depending on your income and other circumstances, you may qualify for financial assistance through the Marketplace, which can reduce your monthly insurance premium (the amount you pay to enroll in the coverage) and possibly your out-of-pocket expenses.

Texas implemented a new rule — for coverage effective in 2023 and future years — requiring health insurers to add a 35% load to the cost of silver plans to account for the cost of cost-sharing reductions (CSR).4 This effectively makes silver plan prices higher than most gold plan prices, resulting in larger subsidies and even more affordable premiums for bronze and gold plans.5

Frequently asked questions about health insurance in Texas

Who can buy Marketplace health insurance in Texas?

To qualify for health coverage through the Texas Marketplace, you must:

- Live in Texas

- Be lawfully present in the United States

- Not be incarcerated

- Not be enrolled in Medicare

Eligibility for financial assistance (premium subsidies and cost-sharing reductions) depends on your income. In addition, to qualify for financial assistance with the cost of your Marketplace plan you must:

- Not have access to affordable health coverage offered by an employer. If your employer offers coverage but you feel it’s too expensive, you can use our Employer Health Plan Affordability Calculator to see if you might qualify for premium subsidies in the Marketplace.

- Not be eligible for Medicaid or CHIP.

- Not be eligible for premium-free Medicare Part A.6

- If married, file a joint tax return.7

- Not be able to be claimed by someone else as a tax dependent.7

When can I enroll in an ACA-compliant plan in Texas?

In Texas, you can sign up for an ACA-compliant individual or family health plan from November 1 to January 15 during open enrollment.8

If you need your coverage to start on January 1, you must apply by December 15. If you apply between December 16 and January 15, your coverage will begin on February 1.9

Starting in the fall of 2026, for coverage effective in 2027 and future years, open enrollment will be shorter, ending on December 15, and all plans selected during open enrollment will take effect on January 1.

Outside of open enrollment, a special enrollment period (typically linked to a specific qualifying life event) is necessary to enroll or make changes to your coverage.

If you have questions about open enrollment, you can learn more in our comprehensive guide to open enrollment. We also have a comprehensive guide to special enrollment periods.

How do I enroll in Texas ACA Marketplace health insurance?

To enroll in an ACA Marketplace plan in Texas, you can:

- Visit HealthCare.gov, the Texas health insurance marketplace.

- Purchase individual and family health coverage with the help of an insurance agent or broker, a Navigator or certified application counselor, or an approved enhanced direct enrollment entity.10

- Get a quote from a licensed third-party agency using the quoting feature below.

- Talk directly with a licensed third-party agent or broker at 866-553-3223

You can also call HealthCare.gov’s contact center by dialing 1-800-318-2596 (TTY: 1-855-889-4325). The call center is available 24 hours a day, seven days a week, but it’s closed on holidays.

How can I find affordable health insurance in Texas?

Texas uses the federally-facilitated exchange for individual market plans, so residents who buy their own health insurance enroll through HealthCare.gov.

Across the nearly 4 million Texas residents who enrolled in Marketplace coverage during the open enrollment period for 2025 coverage, 95% were receiving advance premium tax credits (premium subsidies) that paid an average of $541/month toward their premium costs. Across all enrollees, including the 5% who paid full price, this reduced the average net premium to about $57/month.11

Source: CMS.gov11

In addition to premium subsidies, the Affordable Care Act also includes cost-sharing reductions (CSR), which help to reduce out-of-pocket costs on Silver-level plans for people with household income up to 250% of the poverty level.12

Between the premium subsidies and cost-sharing reductions, you may find that an ACA plan is the cheapest health insurance option for you.

And as noted above, Texas requires health plans to charge higher premiums for Silver-level plans4 (to account for the loss of federal CSR funding, but in a uniform manner).

The result is that it’s common to see Gold plans priced lower than Silver plans. If you’re not eligible for CSR, this can make a Gold plan a particularly good value in Texas.5 (If you are eligible for CSR, you’ll want to carefully consider Silver plans, as you’ll forfeit your CSR benefit if you don’t select a Silver plan.)

Texas has not expanded Medicaid under the ACA, so there is still a coverage gap in the state. An estimated 570,000 people are in the coverage gap in Texas, which means they earn less than the poverty level, are not eligible for Medicaid (due to lack of Medicaid expansion in Texas), and are also not eligible for subsidies in the Marketplace because their income is under the poverty level.13

As a result of the Affordable Care Act, federal law only allows a self-employed married couple to purchase small group health insurance if there is at least one additional employee. Even if both spouses work for their business, they aren’t considered two separate employees (and thus eligible for group health coverage, which requires at least two employees) under federal law. But Texas law is different, and takes precedence in this case. In Texas, a small group insurer must issue coverage to any group of two or more employees, even if the group only has two employees who are married to each other.14

So if you and your spouse are self-employed together, you can consider Texas small group plans as well as individual market plans. Marketplace subsidies are not available for small group plans, but you might find that there are factors that make the small group plans preferable (such as the provider network or the option to purchase a PPO plan), especially if you’re not eligible for Marketplace subsidies due to your income.

How many insurers offer Marketplace coverage in Texas?

The Texas individual/family Marketplace will have 16 participating insurers offering coverage for 2026 (coverage areas differ from one insurer to another). This is the same as 2025, but with some changes: Aetna is leaving the market at the end of 2025 (as is the case in all states where Aetna offers Marketplace coverage in 2025), and Harbor Health is joining the Texas Marketplace for 2026.15

Enrollees with Aetna coverage in 2025 will need to select a new plan during the open enrollment period that begins November 1, 2025.

There was a similar change for 2025, when the number of participating insurers stayed at 16,16 but there was one newcomer (Wellpoint)17 and one carrier that exited at the end of 2024 (Ascension/U.S. Health & Life).18

In most Texas counties, at least three insurers are offering health plans on the exchange in 2025, although some counties in the north-central part of the state only have plans available from one insurer. But there are also numerous counties where five or more insurers offer Marketplace plans.19

Are Marketplace premiums increasing in Texas?

In the Texas individual/family health insurance market, the following average premium changes have been proposed for 2026 ,20 amounting to a weighted average proposed rate increase of 32.5%21 before any subsidies are applied:

Texas’ ACA Marketplace Plan Year 2026 PROPOSED Rate Increases by Insurance Company |

|

|---|---|

| Issuer | Percent Increase |

| Aetna/CVS* | Exiting market |

| Celtic/Ambetter | 41.48% |

| Superior Health Plan/Ambetter | 35.95% |

| Blue Cross Blue Shield of Texas | 39.28% |

| CHRISTUS | 22.66% |

| Community First Insurance Plans | 17.58% |

| Community Health Choice | 17.07% |

| Moda | 14.74% |

| Molina | 29.3% |

| Oscar | 31% |

| Sendero | 16.22% |

| Baylor Scott & White Health Plan | 23.71% |

| UnitedHealthcare | 23.02% |

| Cigna | 42.3% |

| Imperial Insurance Companies | 8.15% |

| Wellpoint | 31.22% |

| Harbor Health | New for 2026 |

Source: RateReview.HealthCare.gov and Texas SERFF16

* Aetna/CVS notified policyholders in mid-2025 that the carrier would no longer offer coverage in the individual market after the end of 2025.22 Policyholders can select new 2026 coverage during open enrollment, and have until Dec. 31, 2025 to pick a new plan that will take effect Jan. 1, 2026 (the regular deadline to apply for Jan. 1 coverage is Dec. 15, but that’s not applicable if a person’s plan is ending altogether and not available for renewal).

Prior to the 2023 plan year, Texas did not have an effective rate review program, so the federal government reviewed insurers’ rate proposals in Texas. But that changed as of the 2023 plan year, and the Texas Department of Insurance now handles rate review for individual/family health plans.23

For perspective, here’s an overview of how full-price (pre-subsidy) premiums have changed in the Texas individual/family market over the years:

- 2015: Average increase of 5%24

- 2016: Average increase of 15.8%25

- 2017: Average increase of 34%26

- 2018: Average increase of 32.5%27

- 2019: Average increase of 2.3%28

- 2020: Average decrease of 1.4%29

- 2021: Average increase of 7.4%30

- 2022: Average rate increase of 3%31

- 2023: Average increase of 4.9%32

- 2024: Average increase of 5.3%33

- 2025: Average increase of 5.8%34

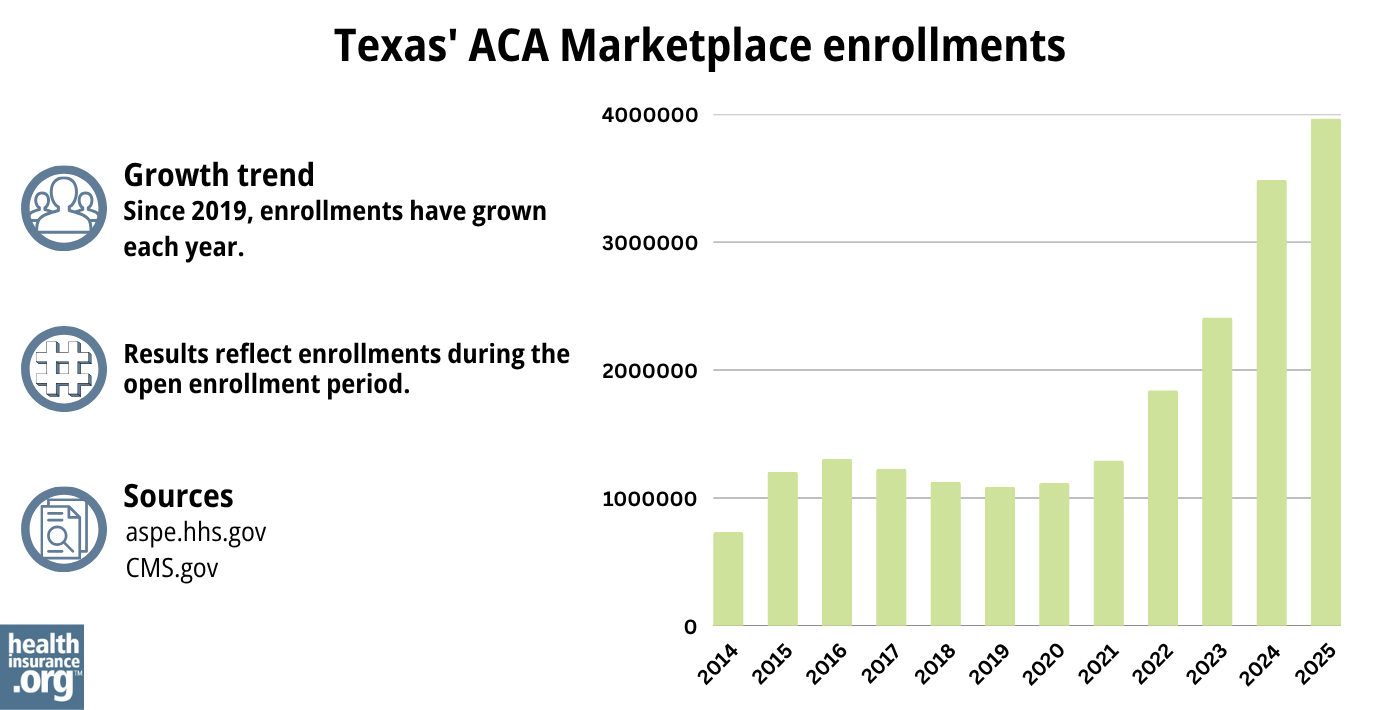

How many people are insured through Texas’s Marketplace?

Enrollment spiked again in 2025 in the Texas Marketplace, for the fourth year in a row (see chart below). Nearly 4 million Texas residents enrolled during the open enrollment period for 2025 coverage.35

The surge in enrollment during these years is likely due to the American Rescue Plan (ARP). Under the ARP, ACA’s premium subsidies are more significant and widely available.36 The ARP’s subsidy enhancements were extended through 2025 by the Inflation Reduction Act. But these subsidy enhancements will expire at the end of 2025 unless Congress takes action to extend them again. If that happens, subsidies will be smaller in 2026, and some people will lose their subsidies altogether.

The 2024 enrollment spike was also likely driven by the “unwinding” of the COVID-related Medicaid continuous coverage rule that had been in place from 2020-2023. By April 2024, CMS reported that nearly 650,000 Texas residents transitioned from Medicaid to a Marketplace plan during the unwinding process. 37

Source: 2014,38 2015,39 2016,40 2017,41 2018,42 2019,43 2020,44 2021,45 2022,46 2023,47 2024,48 202535

What health insurance resources are available to Texas residents?

HealthCare.gov

800-318-2596

Texas Health Plan Compare (a service of the Texas Department of Insurance)

State Exchange Profile: Texas

The Henry J. Kaiser Family Foundation overview of Texas’ progress toward creating a state health insurance exchange.

Looking for more information about other options in your state?

Need help navigating health insurance options in Texas?

Explore more resources for options in TX including short-term health insurance, dental, Medicaid and Medicare.

Speak to a sales agent at a licensed insurance agency.

Footnotes

- ”2025 OEP State-Level Public Use File (ZIP)” Centers for Medicare & Medicaid Services, Accessed May 13, 2025 ⤶ ⤶

- ”Texas Rate Review Submissions” RateReview.HealthCare.gov. And “SERFF Filing number HHIC-134520793” Texas SERFF. Accessed Aug. 30, 2025 *The above is based on the most current data available. ⤶

- ”Plan Year 2025 Qualified Health Plan Choice and Premiums in HealthCare.gov Marketplaces” Centers for Medicare and Medicaid Services. Oct. 25, 2024 ⤶

- ACA Rating Rule. Texas Department of Insurance. April 2022. ⤶ ⤶

- How the Texas Legislature Learned to Stop Worrying and Love the ACA Marketplace. Sprung, Andrew. The American Prospect. April 2022. ⤶ ⤶

- Medicare and the Marketplace, Master FAQ. Centers for Medicare and Medicaid Services. Accessed November 2023. ⤶

- Premium Tax Credit — The Basics. Internal Revenue Service. Accessed May 10, 2024 ⤶ ⤶

- “When can you get health insurance?” HealthCare.gov. Accessed Aug. 5, 2024 ⤶

- “A quick guide to the Health Insurance Marketplace®” HealthCare.gov, Accessed Aug. 9, 2024 ⤶

- “Entities Approved to Use Enhanced Direct Enrollment” CMS.gov, Aug. 9, 2024 ⤶

- “2025 Marketplace Open Enrollment Period Public Use Files” CMS.gov, May 2025 ⤶ ⤶

- APTC and CSR Basics. Centers for Medicare and Medicaid Services. June 2023. ⤶

- How Many Uninsured Are in the Coverage Gap and How Many Could be Eligible if All States Adopted the Medicaid Expansion? KFF. Feb. 25, 2025 ⤶

- ”Treatment of Very Small Groups in the TX Group Health Market” Kilpatrick Companies. Dec. 23, 2016 ⤶

- ”Texas Rate Review Submissions” RateReview.HealthCare.gov. And “SERFF Filing number HHIC-134520793” Texas SERFF. Accessed Aug. 30, 2025 ⤶

- ”Texas Rate Review Submissions” RateReview.HealthCare.gov. Accessed Dec. 4, 2024 ⤶ ⤶

- ”Wellpoint expanding healthcare coverage in your market for 2025 plan year” Wellpoint Provider News. Sep. 17, 2024 ⤶

- ”Ascension will stop offering health insurance plans in Texas” Kut News. June 27, 2024 ⤶

- Plan Year 2025 Qualified Health Plan Choice and Premiums in HealthCare.gov Marketplaces. Centers for Medicare and Medicaid Services. Oct. 25, 2024 ⤶

- ”Texas Rate Review Submissions” RateReview.HealthCare.gov. Accessed Aug. 30, 2025 ⤶

- ”2026 Gross Rate Changes – Texas: +32.5% (updated; CHRISTUS not dropping out after all)” ACA Signups. Aug. 29, 2025 ⤶

- ”Aetna to exit the ACA exchanges in 2026” Fierce Healthcare. May 1, 2025 ⤶

- Texas Rate Review Requirements for Health Benefit Plans. Texas Department of Insurance. Accessed December 2023. ⤶

- Analysis Finds No Nationwide Increase in Health Insurance Marketplace Premiums. The Commonwealth Fund. December 2014. ⤶

- FINAL PROJECTION: 2016 Weighted Avg. Rate Increases: 12-13% Nationally* ACA Signups. October 2015. ⤶

- Avg. UNSUBSIDIZED Indy Mkt Rate Hikes: 25% (49 States + DC). ACA Signups. October 2016. ⤶

- 2018 Rate Hikes. ACA Signups. October 2017. ⤶

- Texas: FINAL/APPROVED 2019 #ACA Rate Hikes: 2.3%, But WOULD Likely Have DROPPED 8% W/Out #ACASabotage. ACA Signups. November 2018. ⤶

- Texas: *Final* Avg. 2020 #ACA Premiums: 1.4% Decrease. ACA Signups. October 2019. ⤶

- 2021 Rate Changes. ACA Signups. October 2020. ⤶

- *APPROVED* Avg. 2022 #ACA Rate Changeapalooza! AK, CA, GA, HI, IL, KS, LA, MA, MS, MO, NE, NH, TX, WY. ACA Signups. November 2021. ⤶

- Texas: Average Unsubsidized 2023 #ACA Rate Increases Drop From 8.8% To 4.9% “Thanks” To Bright & Friday Leaving… ACA Signups. October 2022. ⤶

- So How’d I Do On My 2024 Avg. Rate Change Project? Not Bad At All! ACA Signups. December 2023. ⤶

- ”Texas: Preliminary avg. unsubsidized 2025 #ACA rate changes: +5.8% (semi-weighted); US Health & Life dropping out?” ACA Signups. Sep. 13, 2025 ⤶

- “2025 Marketplace Open Enrollment Period Public Use Files” CMS.gov, May 2025 ⤶ ⤶

- “Health Insurance Marketplaces 2023 Open Enrollment Report” CMS.gov, Accessed August 2023 ⤶

- ”HealthCare.gov Marketplace Medicaid Unwinding Report” Centers for Medicare & Medicaid Services. Data through April 2024; Accessed Aug. 5, 2024 ⤶

- “ASPE Issue Brief (2014) ASPE, 2015 ⤶

- Health Insurance Marketplaces 2015 Open Enrollment Period: March Enrollment Report, HHS.gov, 2015 ⤶

- “HEALTH INSURANCE MARKETPLACES 2016 OPEN ENROLLMENT PERIOD: FINAL ENROLLMENT REPORT” HHS.gov, 2016 ⤶

- “2017 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2017 ⤶

- “2018 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2018 ⤶

- “2019 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2019 ⤶

- “2020 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2020 ⤶

- “2021 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2021 ⤶

- “2022 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2022 ⤶

- “2023 Marketplace Open Enrollment Period Public Use Files” CMS.gov, 2023 ⤶

- ”HEALTH INSURANCE MARKETPLACES 2024 OPEN ENROLLMENT REPORT” CMS.gov, 2024 ⤶