Bronze health plan popularity surges in Marketplaces

Higher net premiums have pushed buyers to lower-price Bronze plans for 2026. Here’s what buyers need to know.

In this article

As consumers face decreased access to Marketplace health insurance subsidies for 2026 plans – and higher net premiums for consumers who continue to be subsidy-eligible – one clear buying trend has emerged: a migration of buyers to Bronze-level health plans.

During the open enrollment period for 2026 coverage, nearly 40% of all Marketplace enrollees selected a Bronze plan,1 up from about 30% the year before.2

And while about 43% of enrollees selected Silver plans for 2026,3 that was down from about 56% the year before.4 In other words, a significant number of enrollees have downgraded their coverage for 2026, in addition to the people who simply dropped their coverage altogether.

What’s happening with Marketplace health plan enrollments?

Enrollment in Marketplace health plans declined in 202656 after four consecutive years of record-high enrollment.7 This was not surprising, given the sharp increase in net premiums for 2026 due to the expiration of federal subsidy enhancements at the end of 2025.

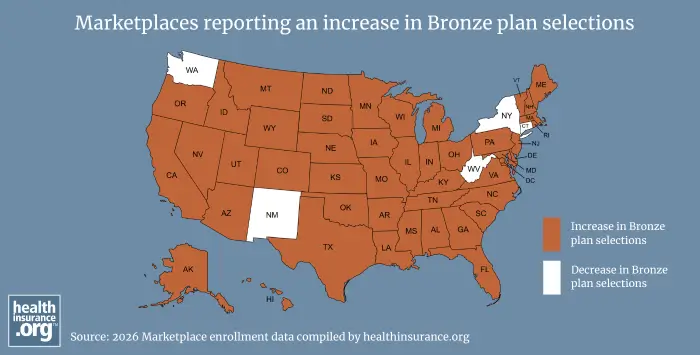

And among the people who did enroll in Marketplace coverage for 2026, there was a significant uptick in the percentage of people selecting Bronze plans. In fact, there were only five states (Connecticut, New Mexico, New York, Washington, and West Virginia) where the percentage of enrollees selecting Bronze plans didn’t increase.8

Why might consumers be downgrading to Bronze plans?

Lower premiums

Although all Marketplace plans cover the ACA’s essential health benefits, Bronze plans have higher deductibles and out-of-pocket limits than Silver or Gold plans.9 As a result, Bronze plans have lower monthly premiums.

So when consumers were faced with average net premiums that more than doubled for 2026 (if they had kept the same plan they had in 2025),10 it’s understandable that people may have selected a different plan with a lower premium, in an effort to keep their monthly premium costs affordable.

Ultimately, once people made their plan selections for 2026, the national average after-subsidy premium ended up being $178/month. This was roughly a 58% increase from 2025, when the average was $113/month.11

To be clear, a large part of the reason that average net premiums increased by “only” 58%, instead of more than doubling, was due to people downgrading to lower-premium Bronze plans.

Access to HSA contributions

The fact that Bronze plans are newly HSA-eligible may also have been a factor in some enrollees’ decisions to downgrade to a Bronze plan. As of 2026, all Bronze (and Catastrophic) Marketplace plans are HSA-eligible, meaning that people who enroll in these plans have the option to contribute pre-tax money to a health savings account (HSA).

Learn more about health savings accounts and the tax advantages they offer.

Contributions to an HSA will reduce the ACA-specific modified adjusted gross income (MAGI) that’s used to determine Marketplace subsidy eligibility. So selecting an HSA-eligible plan and making HSA contributions is a way for people to increase their subsidy amount (due to their reduced MAGI) or potentially qualify for subsidies if the HSA contribution brings their MAGI down below 400% of the federal poverty level (FPL).

This became more important in 2026, due to the return of the “subsidy cliff.” Enrollees with household income above 400% of FPL have to pay full-price for their coverage in 2026, so opting for a Bronze plan and contributing to an HSA may have been a choice that allowed some enrollees to continue to qualify for a subsidy.

Which states saw a decrease in Bronze plan selections?

In 45 states and Washington, D.C., there was an increase in the percentage of enrollees who selected Bronze plans for 2026.

There were only five states where the percentage of enrollees selecting Bronze plans decreased: Connecticut, New Mexico, New York, Washington, and West Virginia. (Four of these five – all but West Virginia – offer state-funded subsidies for their Marketplace enrollees, in addition to federal ACA subsidies.)

In Connecticut, New Mexico, and New York, the reduction in Bronze plan enrollment was very slight, at less than three tenths of a percentage point, and in West Virginia, the decrease was less than one percentage point.

In Washington, the decrease in Bronze plan enrollment was a little more significant than the other states, at nearly three-and-a-half percentage points. Bronze plans accounted for about 30% of plan selections in 2026, down from about 33.4% in 2025.8

In addition, Washington experienced a very significant increase in the percentage of enrollees who selected Gold plans: In 2025, about 19% of Washington Marketplace enrollees selected Gold plans,12 and this grew to 53% in 2026.13 Because Silver plans became more expensive, premium subsidies also increased, as subsidy amounts are based on the cost of a Silver plan. These larger subsidies made Gold plans more affordable, leading to a substantial increase in Gold plan selections for 2026.14

Although Bronze plan selections dropped only slightly in New Mexico, it’s noteworthy that very few Marketplace enrollees choose Bronze plans in New Mexico. Bronze plans accounted for 3.4% of plan selections in New Mexico’s Marketplace in 2025,15 and dropped to 3.1% in 2026,16 versus about 40% of Marketplace plan selections nationwide.17

This is because New Mexico offers additional state-funded subsidies that result in robust “Turquoise” plans being available to enrollees with household incomes up to 400% of the federal poverty level.18 These are by far the most popular plans in the New Mexico Marketplace, selected by nearly eight out of ten enrollees buying 2026 plans.16

New Mexico is also the only state that used state funding to fully backfill the reduction in federal premium subsidies for 2026.19 So while consumers in many states responded to higher net premiums (stemming from the expiration of the federal subsidy enhancements) by downgrading their coverage to a plan with a lower premium,20 there was no need for New Mexico residents to do that.

What does a shift to Bronze plans mean for consumers?

Bronze plans have average deductibles of nearly $7,500 in 2026, which is more than double the overall weighted average deductible across all Marketplace plans.9 Plan designs vary considerably, but some Bronze plans count all non-preventive care toward the deductible (and deductibles can be as high as $10,600 in 2026, depending on how the plan is designed).21

So consumers who select Bronze plans will generally have deductibles that are quite a bit higher than the average Marketplace plan deductible. Their total out-of-pocket exposure is often as high as the allowable maximum, which is $10,600 for a single individual in 2026.22 And depending on how the plan is designed, it might pay very little until the enrollee has met the deductible.

This means Bronze plan enrollees should be prepared for the possibility of having to pay several thousand dollars in out-of-pocket costs if they end up needing medical care during the year.

Unfortunately, a person who downgraded to a Bronze plan because of premium affordability might struggle to come up with the money to pay their deductible. Or they might avoid getting necessary medical care because of the cost.20

Options for Bronze plan buyers facing higher out-of-pocket costs

If you’re enrolled in a Bronze plan and worried about higher out-of-pocket costs, there are several tips to keep in mind:

- Comparison shop for your care whenever possible. Although your health plan might have a wide range of in-network hospitals, medical offices, and pharmacies, that doesn’t mean your out-of-pocket costs will be the same at all of them. If you need a prescription, you can check with various in-network pharmacies (including mail-order options) to see if there are price differences. The same is true for other medical care, and there are transparency tools that can help you determine what your costs will be.23

- Discuss your financial situation with your medical providers. You may find that they can offer a payment plan that fits within your budget.

- If at all possible, consider opening and funding an HSA. All Bronze plans are HSA-eligible as of 2026. The money you contribute to an HSA is pre-tax. And if you need to use it to pay your deductible or other medical expenses, it will continue to be tax-free when you make the withdrawal. If you don’t end up needing to use the money in your HSA, it will remain in the account in future years until if and when you need it.

- If your income isn’t more than 200% of the federal poverty level, you might be eligible for reduced out-of-pocket costs if you use a federally qualified health center (FQHC) that’s in your plan’s provider network. Depending on your income, these clinics can reduce the amount that you’d otherwise have to pay out-of-pocket under the terms of your health plan.24

- Consider supplemental coverage, such as a critical illness policy or an accident insurance policy, that could reimburse some of your out-of-pocket costs if you were to face unexpected medical costs for a covered illness or injury.

- Some people with high-deductible health insurance choose to enroll in a local doctor’s direct primary care (DPC) membership program, to have unlimited access to various primary care services. And as of 2026, having a DPC membership no longer prohibits a person from making HSA contributions if they also have an HSA-eligible health plan, as long as the DPC membership meets certain parameters.25

Footnotes

- “2026 Marketplace Open Enrollment Period Public Use Files” (state-level public use files, Column BW divided by Column H). Centers for Medicare & Medicaid Services. Mar. 27, 2026 ⤶

- “2025 Marketplace Open Enrollment Period Public Use Files” (state-level public use files, Column BR divided by Column H). Centers for Medicare & Medicaid Services. May 12, 2025 ⤶

- “2026 Marketplace Open Enrollment Period Public Use Files” (state-level public use files, Column BX divided by Column H). Centers for Medicare & Medicaid Services. Mar. 27, 2026 ⤶

- “2025 Marketplace Open Enrollment Period Public Use Files” (state-level public use files, Column BS divided by Column H). Centers for Medicare & Medicaid Services. May 12, 2025 ⤶

- “ACA Sign-Ups Are Down by Over a Million People, But It’s Still an Incomplete Picture” KFF.org. Jan. 29, 2026 ⤶

- “2026 Marketplace Open Enrollment Period Public Use Files” (state-level public use files, Column H). Centers for Medicare & Medicaid Services. Mar. 27, 2026 ⤶

- “Marketplace Enrollment, 2014-2025” KFF.org. Accessed Mar. 3, 2026 ⤶

- “2026 Marketplace Open Enrollment Period Public Use Files” (state-level public use files, Column BW divided by Column H). Centers for Medicare & Medicaid Services. Mar. 27, 2026. And ”2025 Marketplace Open Enrollment Period Public Use Files” (state-level public use files, Column BR divided by Column H). Centers for Medicare & Medicaid Services. May 12, 2025 ⤶ ⤶

- “Deductibles in ACA Marketplace Plans, 2014-2026” KFF.org. Nov. 6, 2025 ⤶ ⤶

- “ACA Marketplace Premium Payments Would More than Double on Average Next Year if Enhanced Premium Tax Credits Expire” KFF.org. Sep. 30, 2025 ⤶

- “2026 Marketplace Open Enrollment Period Public Use Files” (state-level public use files, Column AG). Centers for Medicare & Medicaid Services. Mar. 27, 2026. And ”2025 Marketplace Open Enrollment Period Public Use Files” (state-level public use files, Column AB). Centers for Medicare & Medicaid Services. May 12, 2025 ⤶

- “2025 Marketplace Open Enrollment Period Public Use Files” (state-level public use files, Column BT divided by Column H). Centers for Medicare & Medicaid Services. May 12, 2025 ⤶

- “2026 Marketplace Open Enrollment Period Public Use Files” (state-level public use files, Column BY divided by Column H). Centers for Medicare & Medicaid Services. Mar. 27, 2026.

This migration to Gold plans (and reduction in Silver and Bronze plan selections) happened because Washington adopted premium alignment for 2026, requiring insurers to add a 43% load to the premiums for Silver plans. This is because most Silver plans actually have benefits that are similar to those of Platinum plans, as a result of cost-sharing reductions (CSR).[efn_note]“Final Cascade Care Savings amounts for plan year 2026” Washington Health Benefit Exchange. Sept. 30, 2025 ⤶

- “2026 Open enrollment Preview Report” Washington Health Benefit Exchange. Jan. 16, 2026 ⤶

- “New Mexico Open Enrollment 2025 Level of Coverage Summary” BeWellnm. Accessed Mar. 3, 2026 ⤶

- “New Mexico Open Enrollment 2026 Level of Coverage Summary” BeWellnm. Accessed Mar. 3, 2026 ⤶ ⤶

- “2026 Marketplace Open Enrollment Period Public Use Files” (state-level public use files, Column BW divided by Column H). Centers for Medicare & Medicaid Services. Mar. 27, 2026. ⤶

- “Health Insurance Marketplace Affordability Program” New Mexico Health Care Authority. Accessed Mar. 3, 2026 ⤶

- “New Mexico HB4, Fiscal Impact Report” New Mexico Legislature. Feb. 5, 2026 ⤶

- “More Americans are picking higher-deductible Obamacare plans, possibly risking their health” Politico. Feb. 4, 2026 ⤶ ⤶

- “Patient Protection and Affordable Care Act; Marketplace Integrity and Affordability” Centers for Medicare & Medicaid Services; Department of Health and Human Services. June 25, 2025 ⤶

- “Out-of-pocket maximum/limit” HealthCare.gov. Accessed Mar. 6, 2026 ⤶

- “Hospital Price Transparency” and “Health Plan Price Transparency” Centers for Medicare & Medicaid Services. Accessed Mar. 3, 2026 ⤶

- “Chapter 9: Sliding Fee Discount Program” HRSA Health Center Program. Accessed Mar. 3, 2026 ⤶

- “H.R.1” (Section 71308(a)) Congress.gov. Enacted July 4, 2025 ⤶