Resource Center

Browse our resource center for blog posts, FAQs, and more information about healthcare topics.

Plan benefits related topics

Blog posts- What health insurance benefits are available to refugees and asylees arriving in the United States?

- Can I get dental insurance through the Marketplace?

- What is the ACA's preventive health services coverage mandate?

- Does Marketplace health insurance cover Alzheimer’s disease?

- Does health insurance cover IVF and other fertility treatments?

Choosing coverage related topics

Blog postsCoverage costs related topics

Blog postsEligibility related topics

Blog postsEnrollment related topics

Blog postsHealth reform related topics

Blog postsExplore health insurance options!

Get a free quote from a third-party insurance agency.

View our most recent posts

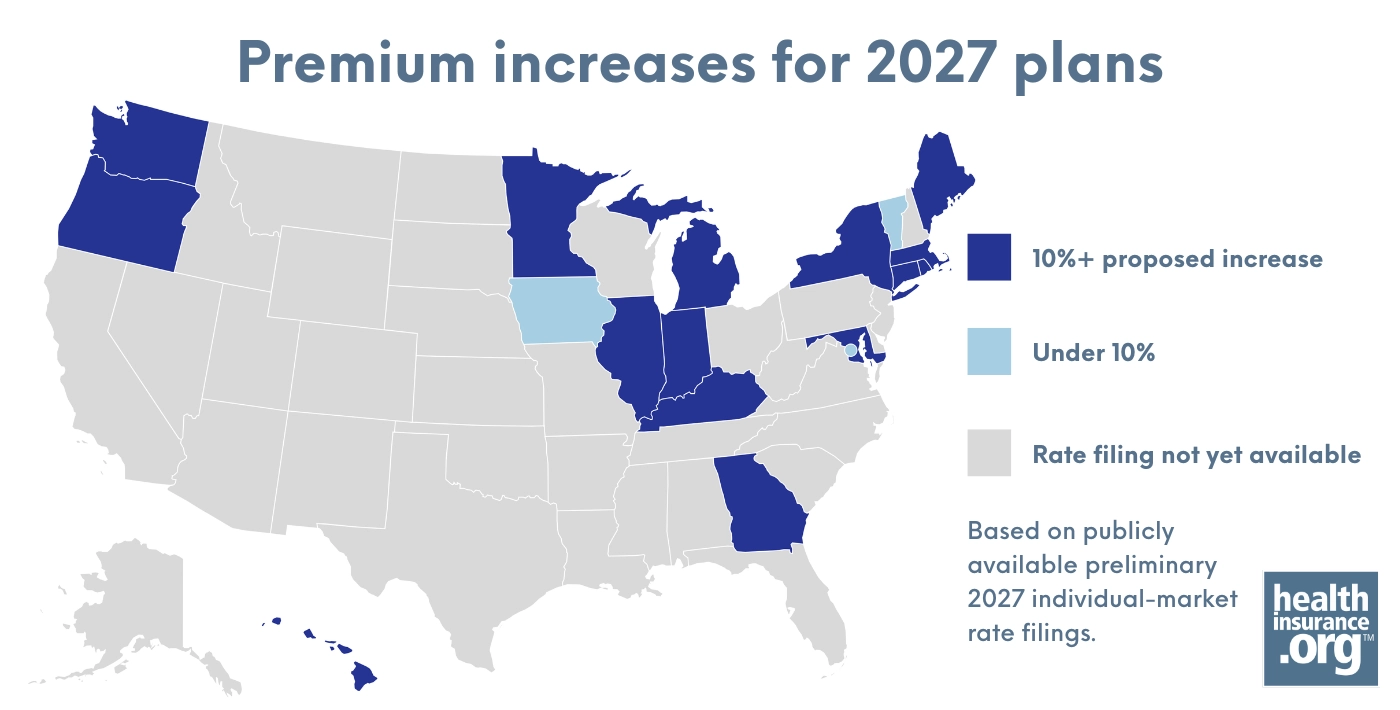

Health insurance premium increases for 2027: Proposed rates by state and what consumers should know

Health insurance premium increases for 2027: Proposed rates by state and what consumers should know

Proposed 2027 health insurance premiums are rising across much of the U.S. See requested rate increases by state and what...

Can AI help you shop for health insurance?

Can AI help you shop for health insurance?

Can AI help you choose health insurance? Learn five ways AI can get Marketplace plans, subsidies, Medicaid eligibility, and state...

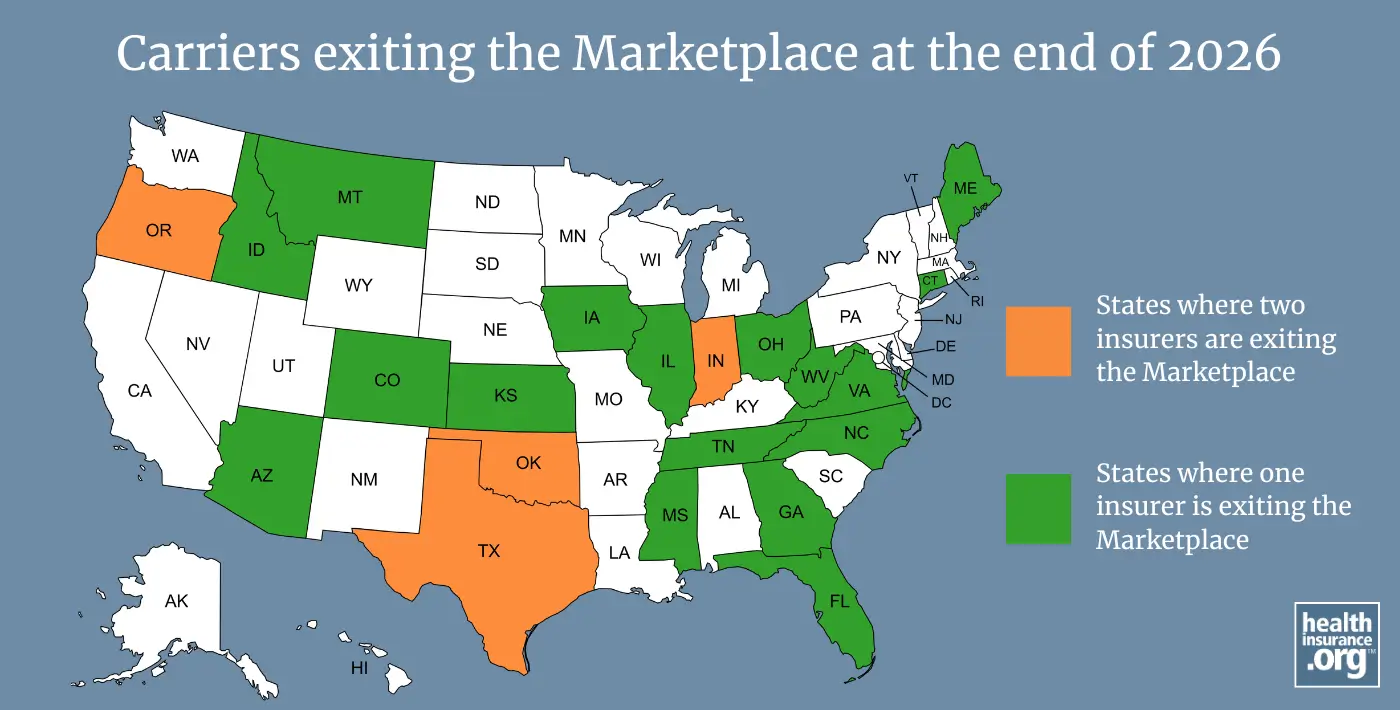

Health insurers are exiting the Marketplace again. Should consumers be worried?

Health insurers are exiting the Marketplace again. Should consumers be worried?

Why are insurers leaving the ACA Marketplace? New exits by Cigna and others highlight growing concerns about enrollment and affordability...

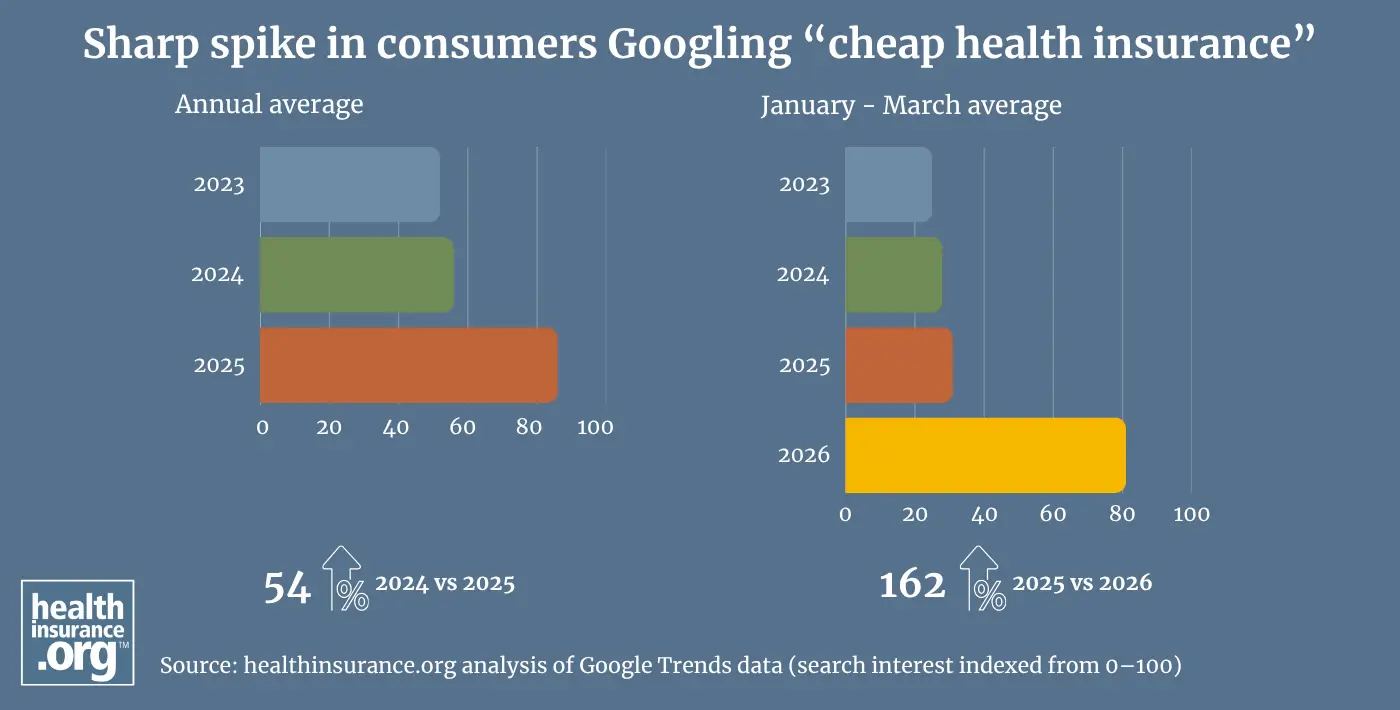

Consumer search trends signal growing cost pressure in health insurance

Consumer search trends signal growing cost pressure in health insurance

Search trends reveal growing concern about health insurance affordability in 2026, as rising premiums and reduced subsidies push consumers to...

Contact a licensed agent to learn more about how to purchase health insurance:

888-389-0372